Hard-to-Get Bonds Hand Quick 20% Returns to China Insiders

In China’s convertible bond market, big investors use privileged access to flip newly issued securities for gains of 20% or more.

(Bloomberg) -- In China’s red-hot convertible bond market, big investors are using their privileged access to deals to flip newly issued securities for gains of 20% or more.

The bonds have been so coveted in recent months that demand for new issuance routinely exceeds supply by hundreds or even thousands of times. Shareholders of companies that issue the securities are guaranteed an allocation if they want one, and many are offloading their holdings almost immediately to lock in gains that averaged 20% on trading debuts this year.

Major shareholders have been particularly notable sellers, cutting positions in more than two-thirds of the 37 convertibles that started trading in 2020 within two weeks, according to data compiled by Bloomberg. A new law that took effect in March stipulates that insiders must hand over to the company any profits made from selling equities or equity-like securities within six months. It’s unclear whether the rule applies to convertible bonds.

Some worry that selling pressure from insiders will expose latecomers to losses. It’s one of several risks hanging over a market that has so far brushed off concerns about China’s coronavirus outbreak, plunging economic growth and frothy valuations.

“Their quick and massive sales will weigh on prices and are definitely negative for other investors,” said Jiang Liangqing, a fund manager at Ruisen Capital Management in Beijing.

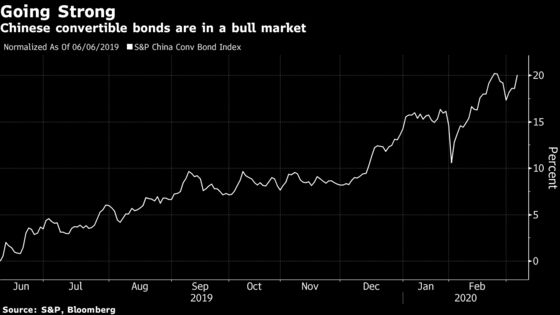

China’s convertible bond market has been booming since the middle of last year as investors flocked to hybrid securities that offer the prospect of equity-like returns with less downside risk.

When a company sells a convertible, existing shareholders have the right to participate in the deal to avoid dilution. And unlike most equity offerings, the bonds don’t have lock-up requirements. That means insiders can sell as soon as the first day of trading.

This year’s biggest issuance came in January, a 7.3 billion yuan ($1.1 billion) deal from financial services provider East Money Information Co. Nearly two thirds of the notes were allocated to existing shareholders; the public tranche was about 760 times oversubscribed.

Qi Shi, East Money’s controlling shareholder, sold 10% of the issued notes in their first two days of trading, according to a filing to the Shenzhen stock exchange. Based on closing prices, Qi could have netted a 30% gain worth about 220 million yuan.

Shanghai Putailai New Energy Technology Co.’s controlling shareholder and related parties bought 55% of a convertible bond issued by the company in early January, only to offload about 10% of the stake on its trading debut. If they sold when prices peaked that day, the return would have been about 50%.

Some investors are optimistic the market will stay strong despite insider selling. China’s CSI 300 Index of large-cap shares climbed to a two-year high on Thursday, fueling speculation that the equity component of convertible bonds will continue to increase in value.

“The enthusiasm to subscribe for convertible bond offerings will not be dampened by sales from big shareholders given the market environment at the moment,” said Manran Ma, general Manager of Beijing Mamanran Asset Management Ltd.

Others are less sanguine, saying stretched valuations pose a risk. A Standard & Poor’s index of Chinese convertible bonds is trading near a more than four-year high, and market volatility has increased in recent weeks as investors digest the economic implications of the coronavirus outbreak.

If enthusiasm for convertibles fades, big sales by insiders could have a more dramatic effect on prices, according to Jingwei Yu, an analyst at Citic Securities Co.

“Negative impacts may emerge when the secondary market becomes less robust,” Yu said.

To contact Bloomberg News staff for this story: Ken Wang in Beijing at ywang1690@bloomberg.net;Qingqi She in Shanghai at qshe@bloomberg.net

To contact the editors responsible for this story: Sofia Horta e Costa at shortaecosta@bloomberg.net, Fran Wang, Michael Patterson

©2020 Bloomberg L.P.

With assistance from Bloomberg