Big Bets in Asia on Fed Have Traders Guessing Who’s Paying

Big Bets in Asia on Fed Cuts Have Traders Guessing Who’s Paying

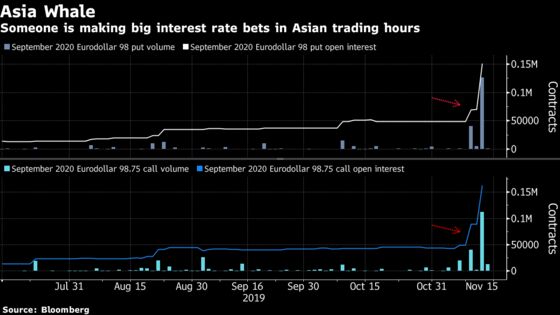

(Bloomberg) -- The eurodollar options market, where investors bet on U.S. interest rates, is typically quiet during Asian trading hours. The lack of liquidity hasn’t stopped the building of huge positions in recent weeks.

A series of block trades, similar in size and structure, has led to speculation that at least one investor is betting big that the Federal Reserve will cut rates only once more, at most, in this cycle. The hedge for just one transaction last week was equivalent to more than four times the average daily volume for September contracts in the region.

With Fed Chairman Jerome Powell sticking to his view Wednesday that rates are probably on hold after three straight reductions, investors have dialed back expectations. Futures show close to zero easing priced in for the remainder of this year, and a quarter-point cut in 2020.

“The Fed shows no signs of hurrying to cut rates,” said Jun Kato, chief market analyst at Shinkin Asset Management in Tokyo. “With Powell repeating that the U.S. economy is in a good shape, speculation that there won’t be any more cuts is gaining momentum.”

That view appears to underlie the eurodollar positions constructed during Asian hours over a period of three weeks, based on an analysis of the options purchased and sold and open interest changes.

The trades started drawing attention from Oct. 24 after a series of large block transactions. From then, they have proceeded like clockwork every few days, with the latest showing a build up of 98.00 puts and 98.75 calls.

Read this to see how the position unfolded

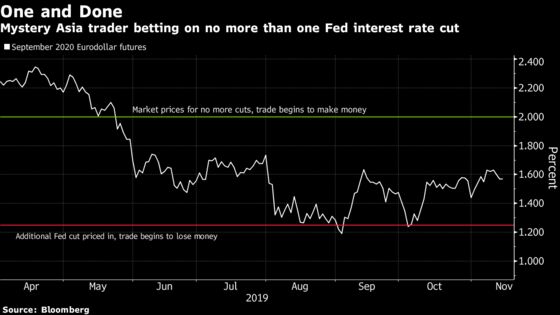

For an illustration of how the trades work, take a look at a risk-reversal bet placed on Nov. 12 on the level of 3-month Libor in September 2020. The investor bought one put option with a target of 2%, and sold a call at 1.25%, a strategy that will make money if markets price out more than one Fed cut and incur losses if expectations for more easing increase.

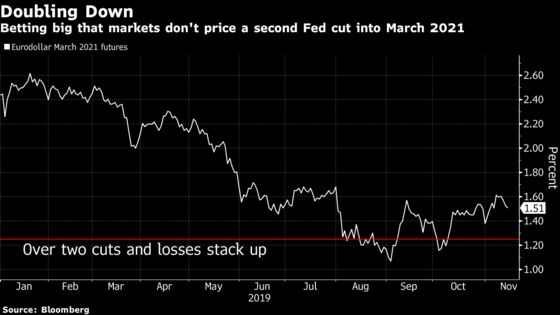

In total, there are are around 280,000 short positions in calls targeting a strike equivalent to 1.25% for the September 2020 and March 2021 eurodollars contracts. That means if markets start to price more than two Fed rate cuts by this time, someone holding that position would stand to suffer heavy losses.

On the flip side, not all economists agree that the Fed will cut rates even once. Morgan Stanley predicts the central bank will remain on hold through 2020 in its global strategy outlook.

The trades stand out not only for their size, but also their timing, during less liquid Asian hours.

Less Liquid

“Simply believing a Fed on hold in 2020 brings us closer” to the 98 strike, at least through the end of this year, said Albert Marquez, who covers interest rates at Chicago Capital Markets.

Alternatively, the trade might be to take advantage of elevated call skew, he said. Executing during Asian hours is strange, though, as “the amount of edge given up at that time is exaggerated,” he said.

Pricing has probably been expensive as dealers who take the other side of the bet need extra compensation for the risks of hedging positions in thin markets, according to traders in London and Chicago who asked not to be named as they aren’t authorized to speak publicly.

For example, the risk-reversal trade on Nov. 12 was for 80,000 options. Market pricing at that time meant a dealer accepting it would have to sell around 32,000 equivalent Eurodollar futures to hedge it. So far this month, the average daily trading volume during Asia hours for September 2020 contracts is just a little over 7,000, according to data compiled by Bloomberg.

A similar structure counting on minimal deviation in expectations for Fed policy was bought during the U.S. session Friday, and open-interest changes subsequently indicated it was for new risk.

Eurodollar futures are the most-traded interest-rate derivatives. They are standardized, exchange-traded instruments that allow traders to bet on the direction of short-term interest rates and are priced off three-month Libor fixing at expiry.

--With assistance from Chikako Mogi, Elizabeth Stanton and Edward Bolingbroke.

To contact the reporter on this story: Stephen Spratt in Hong Kong at sspratt3@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, ;Benjamin Purvis at bpurvis@bloomberg.net, Cormac Mullen

©2019 Bloomberg L.P.