Bernstein Quants See Historic Divergence Favoring Value Stocks

Bernstein Quants See Historic Divergence Favoring Value Stocks

(Bloomberg) -- The most-hated shares on Wall Street are flashing buy signals for quantitative whizzes at Sanford C. Bernstein.

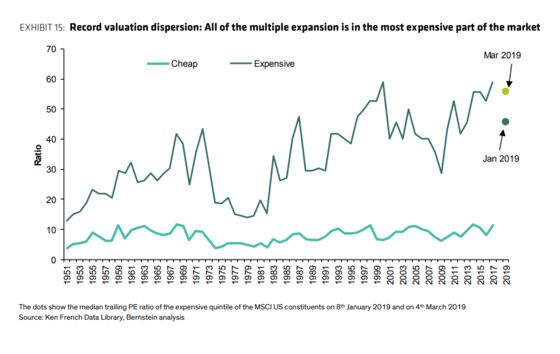

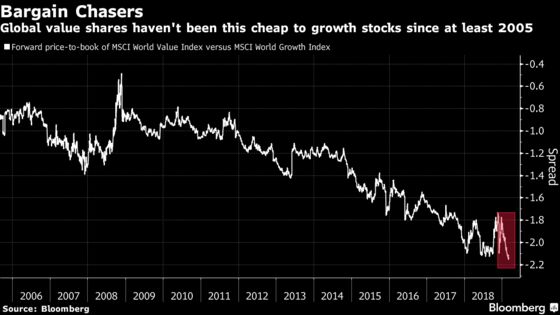

The valuation gulf between the cheapest and priciest companies around the world has reached levels rarely seen in decades of history -- a bullish omen for contrarians fading the extreme divergence with bets on beaten-up value stocks.

Add easier financial conditions with stronger economic sentiment in Europe and Asia, and the stage is set for a tentative rebound in the investing strategy over the next six to 12 months, according to the U.S. firm.

The call is at odds with value bears at Credit Suisse Group AG -- and belies the relentless pursuit for safe equities that offer solid corporate earnings late in the business cycle.

“Valuation spreads in the U.S. are close to all-time wide levels compared to the past 70 years,” strategists led by Inigo Fraser-Jenkins wrote in a note. “They are also wide in other regions. This provides a support for value within the market contrasted with traditional asset classes which are mostly fully valued.”

While value stocks have lagged the $8 trillion new-year rally, companies that boast low volatility and strong balance sheets are on a tear -- pushing up relative premiums across the board.

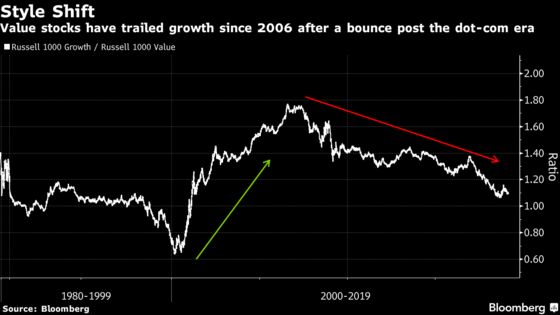

It’s part of a deeper trend, of course. Since 2006, value has lagged as investors rushed to growth- or low-volatility stocks citing the mantra that cheap stocks are cheap for a good reason.

But you can forgive chartists for eying an inflexion point. When the valuation gap notched current highs, stocks were mired in a growth frenzy during the dot-com era -- paving the way for a huge value comeback as the bubble burst.

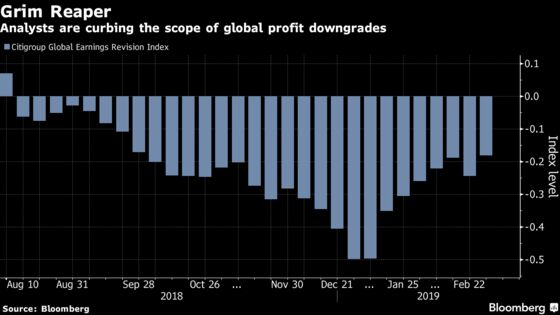

Another bull case: the investing style tends to outperform after sell-side profit projections have bottomed out -- as is the case now, according to Bernstein.

“Value as a style tends to perform better than average when there have been extreme troughs in the earnings revisions balance series particularly 6-12 months following the point of most aggressive downgrades,” the strategists wrote.

The gap between the cheapest and priciest firms is especially apparent among European automakers, where Ferrari NV trades at 12 times forward price-to-book and Renault SA trades at 0.4 times.

But the counter-case is forceful. Bargain hunting has largely been a losers’ game post crisis as low-priced equities trailed higher-rated peers with earnings potential, known as growth shares.

Credit Suisse analysts including Andrew Garthwaite summed up the bearish view Tuesday, saying low-priced equities might end up as a “value trap”. The reason? Many undervalued industries like automakers and utilities are in the grip of unusually strong disruption trends.

Still, Bernstein strategists are unbowed.

“Make no mistake -- this is a tactical call,” they said. “We still think that earnings growth is slowing compared to recent years and at some point the poor quality of corporate debt will weigh on buybacks and earnings. But at the same time valuation spreads are incredibly wide and sentiment may have found a floor.”

To contact the reporter on this story: Ksenia Galouchko in London at kgalouchko1@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Sid Verma, Lu Wang

©2019 Bloomberg L.P.