Beloved Hedge-Fund Trade Delivers Best FX Returns Since 2012

Beloved Hedge-Fund Trade Delivers Best FX Returns Since 2012

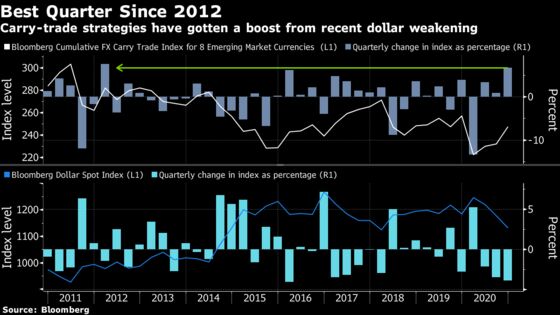

(Bloomberg) -- A foreign-exchange strategy popular with hedge funds is having its best quarter in eight years, with investors betting that there are more gains to come in 2021.

Carry trades -- which use funds borrowed in a currency with low interest rates to invest in one with a higher yield, such as those of developing nations -- have returned 6.7% since Sept. 30, according to a Bloomberg index that tracks speculation on eight emerging-market currencies. That’s on track for the best quarter since the first three months of 2012. Those who used dollars to buy the South African rand have reaped a 16% windfall since the end of September, while wagers on the Colombian peso have gained 11%, data compiled by Bloomberg show.

The success of this playbook is largely thanks to the weakening dollar and lower U.S. borrowing costs. The greenback, helped by the Federal Reserve’s decision to fight the economic fallout from the pandemic with interest-rate reductions and asset purchases, has dropped about 13% from its March peak and become a favored currency to fund carry trades. While this extended decline has kindled concern that bets against the greenback are overdone, Wall Street is almost unanimously forecasting a further slide in 2021 and money managers still expect these trades to deliver.

“The outperformance of currencies and equities in emerging markets should be apparent” next year, said Alessio de Longis, Invesco Ltd.’s head of tactical asset allocation solutions, who has bought the Indian rupee and Colombian peso. “These are some emerging-market currencies that have a good combination of yield and better valuations.”

Invesco was neutral on the dollar until May, when it started to increase its exposure to other currencies. Now, de Longis is betting on gains from emerging markets, and sees his bets providing mid-to-high single-digit returns in 2021.

Using the greenback to finance carry trades is a relatively recent phenomenon, reflecting the depreciating pressure of the Fed’s easing measures after years of dollar strength. But with speculative and real money accounts betting against the currency, any bounce higher by the greenback could lead to short covering and a potentially painful squeeze.

It’s a far from academic question, given the dollar stands to benefit from either a renewed bout of market volatility and risk aversion, or signs that the U.S. is recovering faster than the rest of the world. A Covid-19 vaccine that doesn’t produce herd immunity, or one that works well enough to cause the Fed to tap the brakes on easing, could lead to a bout of dollar strength, Deutsche Bank’s Alan Ruskin wrote in a note last Friday.

“We do think that a weaker dollar is a good basis as we go into next year,” said Marvin Loh, senior global macro strategist at State Street Corp. “But the caveat is that the dollar performs well when there’s global volatility, as we saw earlier this year.”

©2020 Bloomberg L.P.