All-or-Nothing Stock Market Lurches All Around and Goes Nowhere

Naturally, despite all the tumult, shares completed the month with one of their smallest wire-to-wire moves of the year.

(Bloomberg) -- If you’re an investor convinced the trade war is going to cause a recession sometime soon, the market saw it your way in August, delivering three separate plunges of 2.6% or more in the S&P 500.

On the other hand, if you’re sure everything’s under control, that President Donald Trump will steer the economy out of trouble, the same index served up seven different 1% rallies affirming your view.

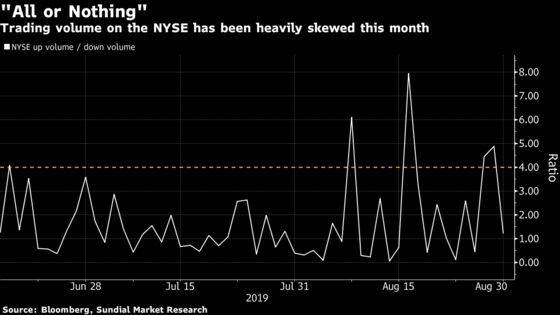

In August equities, bone-rattling reversals were the norm. Going by one metric, “all-or-nothing days” in which up or down share volume got to historical extremes on the New York Stock Exchange, the month saw as much back-and-forth volatility as any in four years.

Naturally, despite all the tumult, shares completed the month with one of their smallest wire-to-wire moves of the year -- down 1.8% on the S&P 500. It was another lesson in humility for anyone trying to make sense of market swings. However important day-to-day moves feel emotionally, they carry all the meaning of soda fizz.

“It was like the last nine months on steroids,” said Peter Mallouk, president of Creative Planning, a wealth-management firm with about $43 billion in assets. “All of it smashed into a few weeks,” he said. “The swings with the Fed and tariffs were just much more significant and the stakes get higher as time goes on.”

Odds are, it’s a world U.S. investors will need to get comfortable with as questions about trade and global growth linger into an election year. However quickly sell-offs get unwound these days, markets are showing themselves vulnerable to moves that two years ago were all but unheard of.

Stitching together a narrative for August got particularly futile as the month wore on. Big down days were framed as a rebuke of the president’s policies, signs a recession is at hand or evidence the Federal Reserve went too far. Big up sessions came a day later and were said to show the strength of earnings, the power of stimulus and the benefits of an expanding economy. Thesis got drubbed today? It should be fine tomorrow.

In the end, the bull-bear symmetry was near-perfect. Twenty-two August trading days, 10 down, 12 up. Volatility indexes that spent parts of the month 50% higher than where they started settled back to where they began. Prices were chaotic, but locked in a range. Three times the S&P 500 plunged 2% or more, and three times it bounced from almost the exact same floor.

Anytime markets get moving this jarringly, scrutiny, informed and otherwise, is trained on traders using computers, entities that get lumped under labels like “the algos” but who in truth at this point are everyone. Only a machine could be suckered into reacting to Trump’s bloviation so credulously, the theories go, and it’s making markets unsafe for human habitation.

Two views on that:

Chris Zaccarelli, chief investment officer for Independent Advisor Alliance: “I think algos are responsible for quick, knee-jerk moves, but it’s harder to blame them for full-day losses. Using it as an excuse is as much a crutch as a retailer blaming bad sales on the weather. It’s somewhat true, but it’s an exaggeration and it’s lame.”

Nancy Tengler, chief investment strategist, Tengler Wealth Management: “It’s been driven by the fact that the algos own the court in the short term on any day. They can have outsize influence in the near term because the programs start selling or buying. And then when you add the fact that half of Wall Street is on vacation, the market appears directionless.”

For people who blame the algos, a follow-up question could be: so what? The market’s digital infrastructure is unlikely to be dismantled anytime soon, things generally get faster, and overall levels of volatility aren’t any different from 50 or 70 years ago.

A more tangible cause for the gyrations may be related to the economy’s health, something that -- unlike Trump’s tirades -- doesn’t announce itself on Twitter all morning.

While it’s always possible to frame macro trends as teetering, S&P 500 earnings do sit 25% above their levels of 18 months ago, unemployment is near a generational low and consumer spending keeps rising -- all as the Fed is cutting rates. In this narrative, Trump tweets pin stocks down at a time when their natural inertia is upward. It’s not machines causing the volatility, but a particularly pitched battle between forward and backward economic forces.

“If you paid attention to short-term news, tweets and all of that market noise, you could’ve easily missed out on the longest bull market in history,” said Randy Frederick, vice president of trading and derivatives at Charles Schwab. “Trump’s tweets move the market around, but if you’re a long-term investor, this shouldn’t matter.”

Algos or not, this month has featured an exhausting list of extreme readings. The tally of days when stocks moved up or down by 1% reached the highest since February 2018. Realized correlations among the S&P 500’s top members soared, pushing stocks into nearly unanimous swings at least 11 times. The Cboe Volatility Index closed below 18 then opened above 21 three times this month. That’s only happened in 11 instances in the history of the index.

There’s more. Small-cap stocks at one point lagged their larger counterparts by the most in two months. The gap needed all of three days to close. Semiconductor stocks looked placid wire-to-wire, ending the month down less than 3%. But the Philadelphia Semiconductor Index dropped more than 3% on three separate occasions.

There was also Invesco’s exchange-traded fund that tracks the 100 companies in the S&P 500 with the highest sensitivity to market moves, otherwise known as beta. The fund was down more than 10% at one point in August. Meanwhile, an ETF tracking low-volatility stocks reached an all-time high, with investors piling in a record amount of cash during the month.

Traders hoping September will be less volatile have to contend with that fact that the next escalation on the trade front is set to take place on Sunday, when tariffs on more than 3,000 categories of Chinese goods go into effect. Barring any delays or cancellations, that is.

“If you think about the three-day weekend, there’s a lot that can happen,” said Shawn Cruz, manager of trader strategy at TD Ameritrade. “That’s 72 hours. You can get a lot of tweets in 72 hours.”

--With assistance from Luke Kawa.

To contact the reporters on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net;Vildana Hajric in New York at vhajric1@bloomberg.net;Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi, Dave Liedtka

©2019 Bloomberg L.P.