Relax. China Only Wants a Bull Market, Not a Mad Cow

Make no mistake: Beijing needs a bull market in stocks, and is willing to stomach the volatility and leverage that comes with it.

(Bloomberg Opinion) -- Make no mistake: Beijing needs a bull market in stocks, and is willing to stomach the volatility and leverage that comes with it.

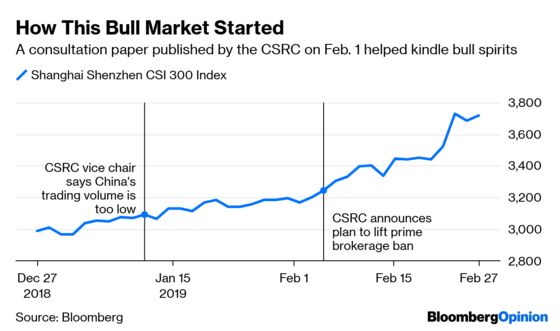

China’s stock market is roaring back, reentering bull territory this week after staging one of the world’s worst routs in 2018. Turnover surpassed 1 trillion yuan ($149 billion) both on Monday and Tuesday.

Leverage is also making a comeback in China’s $6.4 trillion stock market. Firms that offer gray-area margin finance – effectively, those beyond traditional brokers – are coming alive again. Leverage ratios in this sector are as high as 10-to-1, compared with 1-to-1 for regulated channels. On Monday night, China’s securities officials warned of an increase in shadow margin debt and asked brokerages to monitor abnormal trades.

Here’s where your alarm bells may start to go off. Will the China Securities Regulatory Commission kill this young bull?

To answer that, it’s important to put the regulator’s notice in its proper context.

On Feb. 1, just days after Beijing appointed Yi Huiman as the CSRC’s new chairman, the regulator posted a consultation paper on its website. It now aims to reopen prime brokers’ electronic-trading systems to funds, after barring the practice in June 2015. Currently, quant funds have to send their orders to each broker manually. The change would allow hedge funds to execute their strategies faster, bringing more than 1 trillion yuan of extra trading volume a year to mainland stock markets, Goldman Sachs Group Inc. estimates.

The move was daring: Many blamed the 2015 stock rout on brokers offering funds direct access to their electronic trading systems. At the time, margin-financing firms would pool retail investors’ money to open brokerage accounts. Then they’d use computer software programs – such as HOMS, developed by Jack Ma-controlled Hundsun Technologies Inc. – to divide the account into sub-accounts, which allowed mom-and-pops to trade on their own using these systems.

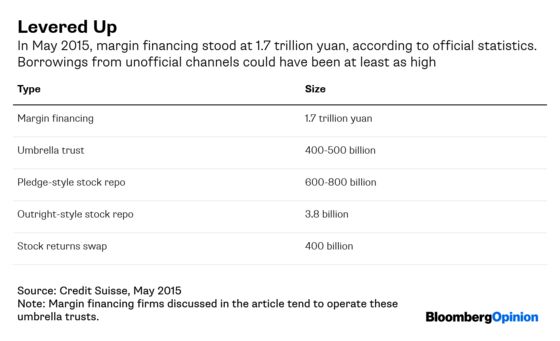

The channel served as a back door to leveraged stock investing, adding close to 500 billion yuan of money into the stock market, according to the CSRC. It also helped precipitate a meteoric rise and equally spectacular crash.

And so the mainland stock market became the wild, wild West. Everyone could borrow to trade, levering up as much as 10-to-1. That’s a stark contrast to the practices that fell under Beijing’s purview. Even in 2015, regulators kept a fairly tight grip on margin lending by brokers. Only certain stocks were eligible for margin trading, and only investors with at least half a million yuan in their securities accounts could borrow. Leverage was capped at 2 yuan in loans for every 1 yuan of collateral.

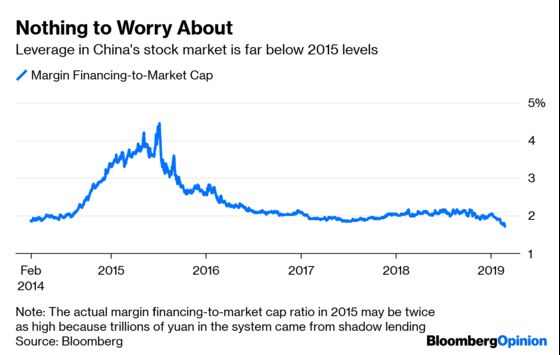

Official margin lending peaked at 2.2 trillion yuan in June 2015, but shadow lending could have been even larger. Beijing had a handle on neither the amount of debt in China’s stocks, nor the scope of forced selling if the broader market tipped downward.

Many investors now see a parallel. Just like 2015, Beijing needs to rekindle bull spirits so consumers can feel richer and start spending again. There’s little chance of that if trading volumes are languishing.

So there’s an alternate reading of the CSRC’s notice. The regulator is only watching “shadow margin financing,” and asking brokers to monitor the “security” of their electronic systems. In other words: Hedge funds, please trade and churn; margin financing firms, stay in your coffin.

Right now, leverage is by no means high. Official margin financing is only back at December 2014 levels, when the bull market just got started. Shadow lending is likely minimal too, because (let’s be frank) who wants to take out loans to invest in this mega bear?

For a government that installs millions of surveillance cameras, what Beijing wants is control and accurate data. If leveraged investing stays below, say, 1 trillion yuan, the A-shares market may well be allowed to blossom. But if margin financing shoots up too fast, brokers could once again get window guidance.

What China wants is a slow bull, not a mad cow. Good luck taming that beast.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.