At Sell-Off's Core Is an Earnings Season That's Consoling No One

Beat, Miss or Match, the Market Doesn't Care About Your Earnings

(Bloomberg) -- A quarter of the way through earnings season and 10 months into what is sure to be the biggest year for profit growth this decade, the numbers are strong. The market doesn’t care.

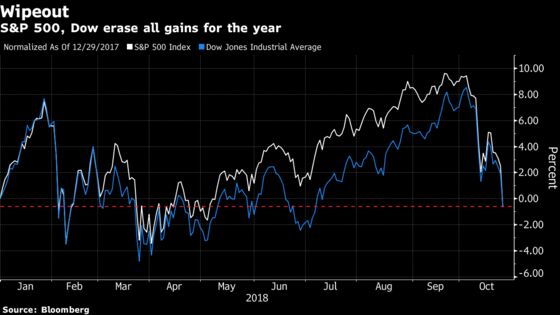

It sounds astonishing: at a time when S&P 500 operating income is surging more than twice the historical average, stocks have gone nowhere, with both the Dow Jones Industrial Average and S&P 500 erasing their annual gain on Wednesday.

“This is really off the wall,” said said Donald Selkin, chief market strategist at Newbridge Securities. “Nothing fundamentally changed during the day. I think it’s a technical breakdown. Look at the Nasdaq -- down 300 points. That’s really off the wall.”

Confidence in the present is quickly becoming panic about the future, as signs of a tottering real estate market, concern about China’s fragile economy and budding indications of inflation blot out optimism that had lifted the S&P 500 almost 10 percent through September. The VIX is at its highest since February.

Aspects of the carnage are different from past corrections. The S&P 500 has declined in 19 of 24 days since peaking in September, with bad days landing at almost twice the frequency of the last three corrections. Unlike earlier selloffs, bulls are fighting the Fed. The central bank has lifted rates eight times since 2015 and given no indication it will let up.

“We’ve been boosting interest rates, inflation, costs. We’re doing all of this in the context of high valuations, low yields, tight spreads,” said Jim Paulsen, chief investment strategist at Leuthold Weeden. “Everyone knows we’re late in the cycle, so what we’ve got is a very narrow path performance in the economy that’s going to be hospitable for the market."

Almost everything fell on Wednesday. Semiconductor stocks, up 15 percent as recently as June, plunged the most since 2014, with trading bellwethers Nvidia and AMD both losing more than 9 percent. High-priced tech stocks in general were crushed, sending the Nasdaq Composite Index into a correction. In the Dow this week, 3M, Goldman Sachs and DowDuPont are down at least 7.5 percent, while Caterpillar has plunged 14 percent.

“What is different this time is that the market is focusing more on the macro issues than earnings,” Gary Bradshaw, a portfolio manager at Hodges Capital Management in Dallas, said by phone. “There’s the Fed, there’s a trade war, there’s China slowing down a little bit, there’s the uncertainty in Europe.”

To the extent earnings matter anymore, it’s not this year’s but next year’s, where forecasts for an 11 percent gain are coming under the strictest of scrutiny. Partly it’s the “peak earnings” argument that says the deceleration to roughly half this year’s rate will leave investors with no reason to buy. But it’s also concern that the estimates themselves won’t hold up.

Before 2018, analyst forecasts proved too optimistic in each of the past five years, with their annual estimates falling an average 3.8 percent from January to December. Should the pattern repeat in 2019, the current profit prediction for $176.60 a share would end up somewhere around $170.00.

“There are some pretty big speed bumps in the road ahead,” Lori Calvasina, head of U.S. equity strategy at RBC Capital Markets, wrote in a note. “Nothing we’ve heard in this first wave of reporting has done anything to change that view. If anything, our concern that margin damaging sources of inflation are ramping up has been confirmed.”

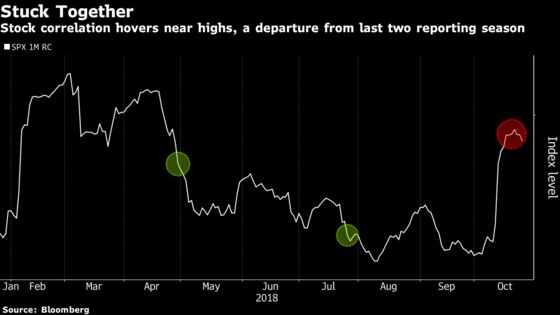

The last few weeks have shown that earnings alone can’t always rescue the market.

Reporting season is supposed to be the time when investors shift focus to individual companies, allowing stocks to break their lockstep moves imposed by macro drivers. It happened in the last two quarters, when correlation among S&P 500 members dropped at this time.

That hasn’t happened in October. Two weeks in, correlation is stuck near a six-month high.

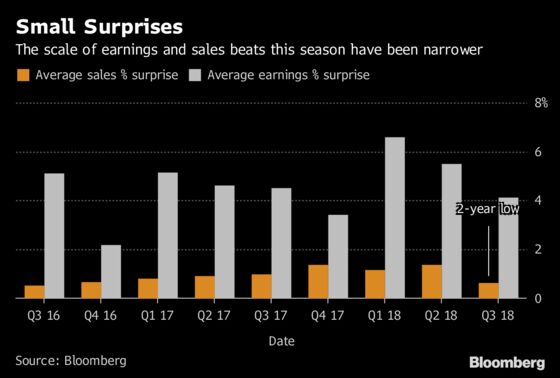

Amid all the chatter about high costs, tariffs, and a stronger dollar, it’s easy to forget this has been a pretty stellar run of profits. Out of 142 S&P companies that have reported results, 78 percent have posted earnings above estimates.

But companies that have posted positive surprises aren’t getting rewarded nearly as much as they used to. On average, firms that have beaten on earnings have gained 0.2 percent the day after reporting, according to Wells Fargo Securities data. That’s less than a fifth of the reward last quarter. Beat on sales, and companies have seen gains of half the last time.

“As we get the earnings, they’re coming in good and most of the outlooks are pretty solid, but everybody focuses on the few that aren’t,” said Kate Warne, investment strategist at Edward D. Jones & Co., which manages almost $1.2 trillion. “You need to get a little further through earnings and a little more beyond the worries about the Fed increasing rates. When you look at the aggregate and look back a couple of months from now it’ll be, ‘Oh, that was a good earnings season too.”’

While positive surprises at large aren’t getting rewarded, though, misses aren’t exactly getting pummeled either, according to Keith Parker, head of equity strategy at UBS Securities. In an environment where investors are set on selling equities no matter the numbers, performance of individual companies just hasn’t mattered as much.

“Passive selling puts pressure on all stocks,” he said in a message. “That performance is more indiscriminate than it normally would be in an environment where investors are not selling equities broadly.”

--With assistance from Lu Wang and Vildana Hajric.

To contact the reporters on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net;Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2018 Bloomberg L.P.