Battered Quants Get Shot at Redemption in the Stock Rotation

Battered Quants Get Shot at Redemption in Record Stock Rotation

(Bloomberg) -- For quants battered by a stock rally built on Big Tech, Monday’s record rotation brought sweet relief. But it’s going to take far more than one dose of good news to save their long-suffering strategies.

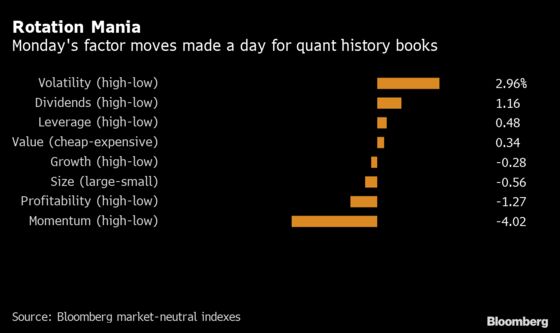

After Pfizer Inc.’s vaccine candidate buoyed hopes for a post-pandemic world, a momentum investing style stuffed with defensive stock bets crashed, breaking records going back to 2000. An equal-weighted S&P 500 beat the regular cap-weighted one by the most ever, a sign of weakening mega-cap dominance. Volatile shares had their best day in nearly two decades.

On Twitter, AQR Capital Management founder Cliff Asness pointed out the plunge in momentum -- which buys the past year’s winners and dumps its losers -- might mark a turning point. “Hope this is one,” he added.

For now, the dramatic moves might benefit quants less than one might think.

Value’s gains on Monday were not enough to make up for the slump in other factors, resulting in losses in some long-short factor portfolios, including the AQR Equity Market Neutral Fund. The iShares MSCI USA Multifactor ETF only rose a modest 0.45%. The $10.5 billion Goldman Sachs ActiveBeta U.S. Large Cap Equity ETF dropped.

Long-short value rose less than 0.6% in both Bloomberg’s and Citigroup Inc.’s indexes -- a mere blip for a strategy that has been a chronic drag on traditional factor portfolios. Meanwhile, hedge funds are clinging to their tech longs as the market’s most reliable winners.

While broadening equity leadership bodes well for systematic funds, wild factor swings are still preventing them from putting more money on their books. That’s capping their gross exposure at below pre-pandemic levels, according to Credit Suisse Group AG’s prime brokerage.

In short, the jury is out on whether the vaccine news will prove a turning point for quantitative investors desperate for stock gains to broaden and to make their math-powered methods look smart again.

The good news is: the risk-on shift is poised to last at least another day. Value rose further Tuesday in New York trading while momentum dropped. The more cyclical Dow Jones Industrial Average and Russell 2000 are beating the Nasdaq 100.

“It certainly was a crazy day,” said Matthew Yeates, head of alternative and quantitative strategy at Seven Investment Management LLP. “It’s one day, a big day, but I think it relies on a change in the policy environment to really get legs.”

For much of this year -- and the past decade -- an equity rally led by Big Tech had undermined computer-powered strategies that tend to buy smaller and cheaper shares. Now, a sustained rotation would be momentous for active managers of all stripes, since a rally dominated by blue-chip growth companies has made it harder to outshine index trackers, especially for those stock pickers with a value tilt.

To the skeptics, there are good reasons why value has failed to sustain any resurgence since the global financial crisis. Low interest rates and anemic economic growth make growth stocks -- as expensive as they may be -- more attractive, and equities trading with low valuations much less so since they tend to be sensitive to the business cycle.

Monday’s moves were likely amplified by just how stretched the virus trades had become. Value stocks have been trading near a record discount to growth for much of this year as investors piled onto tech stocks benefiting from the pandemic.

“Is yesterday’s announcement the definitive turning point for the relative performance of value stocks?” BCA Research strategists wrote in a note. “’Yes’ is a tempting answer, but for now, there is still too much uncertainty concerning the vaccine and its effectiveness to answer resoundingly in the affirmative.”

Among hedge funds, there also isn’t that much conviction in a sustained value-growth rotation, if Credit Suisse’s data are anything to go by. Such players hung onto their long positions on growth names on Monday and were helped by the fact that they already cut their shorts on value last week.

A basket of their favorite bullish bets trailed their bearish wagers by 300 basis points on Monday, Credit Suisse’s numbers show. It’s a wide spread, but the fact that it held steady throughout the day showed there was little forced unwinding, global head of risk advisory Mark Connors wrote in a note to clients. If that continues to be the case, it would limit investor firepower to further fuel a risk-on rotation.

Rising bets on U.S. mega-caps also took equity long-short funds’ net stock exposure to a record 44% last week, according to the bank.

“Permanence of value leadership is the question given previous false starts,” Connors wrote. “Funds are not abandoning core tech longs.”

©2020 Bloomberg L.P.