Banks, Managers Cut Fees in Dysfunctional Europe CLO Market

Banks, Managers Cut Fees in Dysfunctional European CLO Market

(Bloomberg) -- All is not well in Europe’s CLO market. Strong supply of nearly 10 billion euros ($11.2 billion) masks a market that is requiring arrangers and managers to work for less in order to price deals.

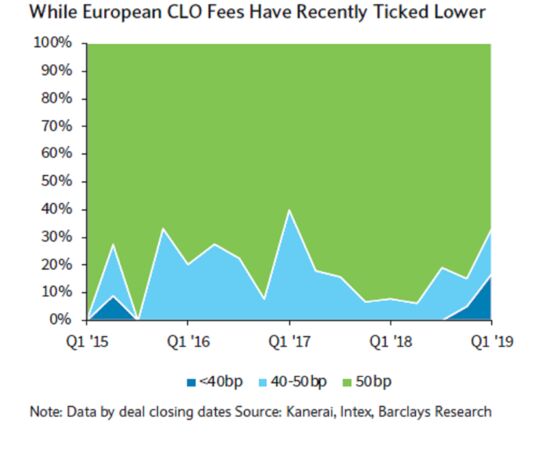

To entice investors into the equity tranche of the CLO structure, some arranging banks are working for a fraction of what they are used to, while on the manager side, the traditional 50 basis point management fee has been reduced by more than 10 basis points in some recent cases.

The fee sacrifice has been vital to help shift CLO warehouses -- the facility arranging banks provide to managers to buy the loan assets -- that might otherwise have clogged a lender’s balance sheet. But it’s seen as a short-term fix to the market’s arbitrage problem and an unsustainable drain on arranging banks’ revenues, according to participants across all segments of the market.

This crunch has happened before, but until it gets fixed there’s concern that the new issue market, which drives demand for leveraged loans, could falter in the months ahead.

Less Pay

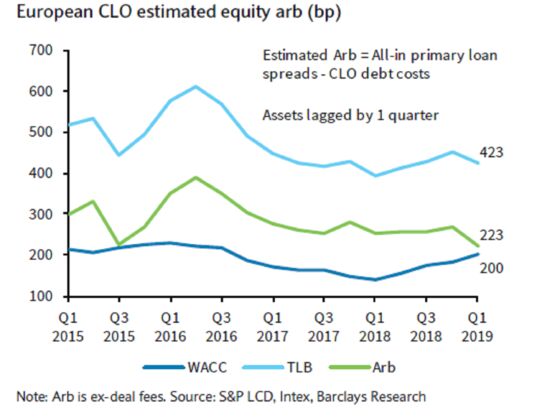

The root of the problem is the out-of-whack arbitrage -- the excess between loan and CLO spreads -- which has moved to its tightest level since 2015, according to research by Barclays Plc. The arbitrage moved out of kilter when loan spreads failed to track CLO spreads wider during the second half of last year amid broader market volatility. As a result, the interest paid by the loans is not enough to pay an attractive equity return after covering the payments due on the bonds.

To make up for any shortfall, investors able to take the lion’s share of an equity tranche, so called “majority investors,” have negotiated more favorable terms.

“Primary equity investors may have the opportunity to negotiate smaller management fees, lower equity purchase prices and private side-letter rebates," Barclays strategist Geoffrey Horton wrote in an April 12 research note. A 10 basis point cut to management fees equates to a 1-1.5 point increase in estimated equity return for a new issue deal, Horton noted.

Arrangers have taken a greater hit. In a market when the arbitrage is working they can expect to make between 50 to 100 basis points on a new issue, but in today’s market the fee can be significantly less, in some cases as little as 12.5 basis points, managers say.

Knowing they may not be paid, some arrangers have opted not to open a new warehouse this year. They have also taken steps to protect their future fee income by looking to open warehouses with managers who have their own equity solutions, be that in-house retention vehicles or otherwise.

That could leave managers reliant on external investors for their equity tranche in a tricky spot. If they are unable to get the required return, but still want to price a deal, they could have to take their own equity, or alternatively fold the CLO warehouse.

Tidal flows

Primary market conditions were tough back in 2015 in the wake of the oil and gas crisis. CLO spreads ballooned to post crisis highs squeezing the arbitrage and slowing issuance. Eventually an influx of investors in 2016, including those from Japan, helped liability spreads to contract quickly and restore the arbitrage.

The trigger for change this time is unclear, although few doubt that the arbitrage dynamics will reset. Conditions are rarely ideal, according to one CLO manager, but equity arbitrage is tidal and this all goes in waves, the manager said.

And perhaps a pause in issuance would be healthy, if it resets CLO pricing expectations and cuts demand for loans. Investors have grown accustomed to an endless supply of new transactions. Less choice could help spreads contract again and benefit the arbitrage.

(Sarah Husband is a leveraged finance strategist who writes for Bloomberg. The observations she makes are her own and are not intended as investment advice.)

--With assistance from Ruth McGavin.

To contact the reporter on this story: Sarah Husband in London at shusband@bloomberg.net

To contact the editors responsible for this story: Vivianne Rodrigues at vrodrigues3@bloomberg.net, Charles Daly

©2019 Bloomberg L.P.