Banks. Italy. Greece. And Now, Higher Volatility: Taking Stock

Banks. Italy. Greece. And Now, Higher Volatility: Taking Stock

(Bloomberg) -- (Bloomberg News has renamed our European Equity Pre-Market column Taking Stock. It will appear every trading day at the same time as the previous column.)

Euro Stoxx 50 futures are little changed after U.S. stocks fell the most since June and volatility spiked higher, while yields hit multiyear highs. Later today will be the release of non-farm payrolls. There is a consensus of 184,000 but several economists are anticipating a number ahead of 200,000, that would likely send bond yields higher. Most attention will be on the pace of the wage growth that accelerated in August, a trend that may continue in the coming months, especially if other companies follow Amazon’s path of wage increase. More signs of overheating are likely to weigh on equities. In the meantime, outflows gave no respite to European shares.

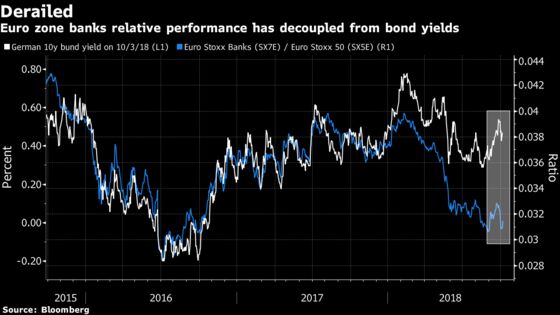

Banks are still the center of attention of investors and strategists. As Credit Suisse’s Andrew Garthwaite highlighted, continental European stocks used to be a play on bund yields, but the relationship is broken, essentially because banks are no longer linked to bund yields. This anomaly can only be reversed by the banking sector’s outperformance, which is anticipated by Garthwaite. The strategist is not buyer of other European shares, essentially because they are not cheap enough relative to their U.S. counterparts.

European Banks have been “terrible performers this year,” Jonathan Stubbs wrote in a note to clients, nothing that they are back to "toxic" global financial crisis valuation levels. The de-rating has tracked lower ECB rate expectations but appears overdone versus fundamentals. “Investors are not positioned for inflation or higher ECB rates," Citi strategist Jonathan Stubbs wrote in a note to clients. "We think that is a mistake.” Nevertheless, caution is probably advised on peripherals, as further development in the Italian debt target will hold the key to the performance of Italian banks, something to keep in mind.

Outside banks, tech will be the sector to keep an eye on after a selloff in tech stocks in both the U.S. and Asia. Chipmakers and chip-equipment firms, are likely to be active in Europe trading.

Luxury goods went out of fashion yesterday amid fear that China is cracking down on travelers returning home with suitcases full of luxury goods. Tightened border enforcement “could be phase 2 of China’s efforts to repatriate consumer spending of its citizens,” according to Exane BNP Paribas analyst Luca Solca.

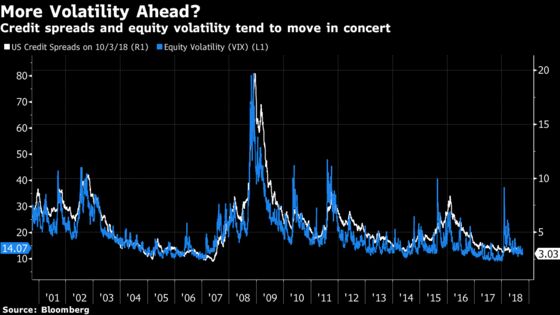

Another theme that’s been on the radar is volatility. The European gauge (V2X spiked above 16 yesterday, and is up 27% from September lows. Volatility is still historically low, which can be surprising given the uncertainty surrounding European equities. The same thing can be said about U.S. markets. Treasuries are selling off and rates are soaring, 10-year yields reached 3.23% -- their highest level since 2011, mid-term elections are coming, and a full-blown trade war scenario is in play, even more so after the the Chinese hack was revealed. Bottom line, volatility seems too low to both Credit Suisse and Societe Generale strategists.

Elsewhere, Hong Kong property stocks have lost as much as 20% from highs and

Asian stocks rounded out a tough week with a further sell-off as technology companies were roiled by escalating concerns about their business in the U.S. Crude oil is bouncing slightly this morning after falling 2.5% on Thursday. Copper is showing further weakness, while gold is steady.

Finally, a few words on Danish jewelry-maker Pandora. The stock used to be one of hedge funds’ favorite short story. Today’s short interest stands below 6% of its float versus 12% in June. After a 40% drop in the share price this year, the firing of the CEO and the release of a profit warning, the stock has still not regained investors confidence, mostly because there is no CEO in place. The announcement of a new chief could be the trigger of a re-rating.

COMMENT:

- “Just eight months after short positions on the VIX suddenly blew up in February and forced a number of familiar hedge fund names to close their doors, short volatility trades are just a shade off their historical highs. Similarly, net long positions on the S&P 500 look uncomfortably high (SG target for end-2019 stands at 2,200, implying a 30% drop in the S&P),” Societe Generale strategists Arthur van Slooten and Alain Bokobza wrote in a note to clients.

NOTES FROM THE SELL SIDE:

- Berenberg says it remains “deeply excited” about the health of the video games sector and sees many further trends to support growth and margin expansion in a note initiating coverage on EA and Activision Blizzard and making Ubisoft its top pick.

- Jefferies gave Brunello Cucinelli its only buy rating of the street, citing recent weakness of shares and the unique characteristics of the brand that justify a premium vs most peers.

COMPANY NEWS AND M&A:

- Unilever abandoned plans to consolidate its headquarters in the Netherlands, saying it would maintain a second base in the U.K., after mounting opposition from Britain-based investors.

- Ahmed Badr is set to rejoin Credit Suisse in Dubai four years after Renaissance Capital hired him from the Swiss bank.

- Regensburg has all the attributes typical of historic German cities: a 12th century bridge across the Danube, a 500-year-old bratwurst stand, a palace with a real-life princess—and a mayor who serves on the board of the local savings bank.

- European industry risks being hobbled by its own environment policies unless Paris climate envoys come up with a universal plan for reducing emissions, according to one of Britain’s largest money managers.

- Watch European Tech After U.S., Asia Selloff But Samsung Beat

- Danske’s $1.5 Billion Capital Penalty Forms Buffer for Fines

- Norsk Hydro Says Closing Alumina Plant Will Take 30-60 Days

- Italy Stocks Still in Focus as Economy Forecasts Look Optimistic

- Bridgepoint Considering IPO of Diaverum, Dagens Industri Reports

- Carlsberg Cuts 74 Jobs in Germany, Jyllands-Posten Reports

- Danske Made Up to EU8.5b Mirror Trades for Russia Customers: FT

- EMS-Chemie Nine Month Net Sales CHF1.77 Bln

- Sonae to Raise as Much as EU412m From Sonae MC IPO

- Gazprom, Fortum Discuss Ongoing Construction of Nord Stream 2

- Bosch to Face Racketeering Claims Over Diesel Cheating

- Greencoat U.K. to Acquire Tom Nan Clach Wind Farm in Scotland

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 383.2 (50-DMA); 384.1 (200-DMA)

- Support at 371.9 (Sept. low); 365 (38.2% Fibo);

- RSI: 49.9

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,413 (50-DMA); 3,460 (200-DMA)

- Support at 3,315 (38.2% Fibo); 3,274 (Sept. low)

- RSI: 48.8

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Bodycote upgraded to buy at HSBC; PT 11 Pounds

- Brunello Cucinelli upgraded to buy at Jefferies; PT 39 Euros

- Eutelsat upgraded to buy at Goldman; PT 26 Euros

- Intertek upgraded to buy at Berenberg

- Kotipizza Group raised to neutral at OP Corporate Bank

- Moncler raised to buy at Kepler Cheuvreux; Price Target 41 Euros

- Rentokil upgraded to buy at Stifel; PT 4.10 Pounds

- SES GDRs upgraded to neutral at Goldman; PT 19 Euros

- TomTom upgraded to buy at Kepler Cheuvreux; PT 9 Euros

- Veolia raised to outperform at Macquarie; Price Target 22 Euros

DOWNGRADES:

- Antofagasta downgraded to sell at Goldman; PT 7.25 Pounds

- Atrium Ljungberg cut to sell at SEB Equities; PT 160 Kronor

- Balder downgraded to hold at SEB Equities; PT 255 Kronor

- Castellum cut to sell at SEB Equities; Price Target 150 Kronor

- D. Carnegie cut to hold at SEB Equities; Price Target 180 Kronor

- Eurofins Scientific downgraded to hold at Berenberg

- Helvetia downgraded to hold at Baader Helvea; PT 625 Francs

- Henkel downgraded to market perform at Raymond James

- Novo Nordisk cut to hold at Pareto Securities; PT 305 Kroner

- Royal Mail downgraded to sell at Citi

- Scout24 downgraded to hold at HSBC; PT 42 Euros

- SkiStar downgraded to hold at DNB Markets; PT 259 Kronor

- UBM Development cut to accumulate at Erste Group; PT 48 Euros

INITIATIONS:

- CLS Holdings rated new buy at Berenberg; PT 2.65 Pounds

- CYBG rated new sell at SocGen; PT 2.90 Pounds

- Opus rated new hold at Kepler Cheuvreux; PT 7 Kronor

- Rosenblatt Group rated new buy at Arden Partners; PT 1.20 Pounds

MARKETS:

- MSCI Asia Pacific down 1.1%, Nikkei 225 down 0.7%

- S&P 500 down 0.8%, Dow down 0.7%, Nasdaq down 1.8%

- Euro down 0.1% at $1.1503

- Dollar Index up 0.11% at 95.86

- Yen up 0.02% at 113.89

- Brent up 0.5% at $85/bbl, WTI up 0.7% to $74.9/bbl

- LME 3m Copper down 1.2% at $6216.5/MT

- Gold spot down 0.1% at $1198.6/oz

- US 10Yr yield up 1bps at 3.19%

MAIN MACRO DATA all times CET:

- 9am: (SP) Aug. Industrial Production MoM, est. 0.7%, prior -0.26%

- 9:30am: (UK) Sept. Halifax House Prices MoM, est. 0.2%, prior 0.1%

- 9:30am: (SW) Aug. Industrial Orders MoM, prior 9.8%

- 10am: (IT) Aug. Retail Sales MoM, est. 0.1%, prior -0.1%

- 10:30am: (UK) 2Q Unit Labor Costs YoY, prior 3.1%

- 11am: (IT) Istat Releases the Monthly Economic Note

- (IT) Bank of Italy Report on Balance-Sheet Aggregates

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Celeste Perri

©2018 Bloomberg L.P.