Bank of Canada Set to Hold Amid Oil Crisis: Decision-Day Guide

Bank of Canada Set to Hold Amid Oil Crisis: Decision-Day Guide

(Bloomberg) -- Bank of Canada Governor Stephen Poloz is expected to hold borrowing costs steady Wednesday, with investors eager for clues on how the country’s unfolding oil crisis will affect plans for future rate increases.

Analysts anticipate policy makers will leave the benchmark overnight interest rate at 1.75 percent in a rate decision at 10 a.m. in Ottawa, before returning to a hiking path next month. The central bank has hiked five times since mid-2017, including at its last meeting in October.

Poloz is trying to return borrowing costs to more normal levels -- possibly as high as 3 percent, according to recent statements. But the dramatic slump in oil prices, and efforts by the Alberta government to remedy the situation with production cuts, have muddied the picture for the economy and reignited doubts the Bank of Canada will be able to hike much more from current levels.

“You can’t really look through that,” Mark Chandler, head of fixed income research at Royal Bank of Canada, said in a telephone interview. “Most people think oil will be the big wild card” for the rate path.

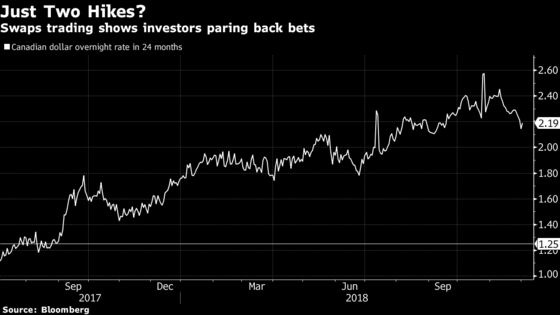

As recently as October, investors were anticipating at least three more rate increases by the end of next year -- but those expectations have dwindled to no more than two. Swaps trading suggests the Bank of Canada will cap its hiking cycle at 2.25 percent, well below what it estimates as its “neutral rate.”

Inflation running above the central bank’s 2 percent target is one key reason policy makers want to raise rates. Another is that the economy continues to do relatively well. It grew by a Group-of-Seven-best 3.1 percent in 2017, and has expanded at a healthy 2.2 percent clip so far this year.

But risks remain, particularly with the nation’s highly-indebted households, leading some to question whether the economy can cope with multiple headwinds on top of rising borrowing costs. The crisis in an oil industry that generates about 10 percent of Canada’s export receipts qualifies as a major snag.

Output Cuts

The price of heavy Canadian crude fell to $13.46 a barrel in November, its lowest in at least a decade, after a global oil sell off was exacerbated by surging oil-sands output, a shortage of pipeline space and heavy U.S. refinery maintenance. While prices for Western Canada Select rallied Monday after Alberta ordered production cuts, they remain below the central bank’s most recent projections.

The Bank of Canada assumed in its October monetary policy report that WCS would average $35 a barrel, half the level of benchmark West Texas Intermediate at $70. As of Tuesday, WCS was trading at about $29.70, after spending most of November below $20. WTI traded around $52.95.

Oil sector woes add to other recent headwinds such as financial market volatility, soft economic data at home and growing concerns about the health of the global expansion that could be prompting policy makers to rethink how quickly to move rates higher. A report last week showed business investment unexpectedly declined in the third quarter. A reduction in the number of rate hikes expected in the U.S. may also complicate the Bank of Canada’s ability to tighten more quickly.

What Our Economists Say |

| “Should the Council conclude that the investment slowdown is due to more than just temporary factors, or that the sharp decline in oil prices will drag on exports, the BoC’s hesitance to raise rates could persist into early next year.” --Tim Mahedy, Bloomberg Economics (read the full report here) |

Still, the case for hikes remains compelling. Pressure on heavy crude prices would likely have been temporary, even without the government-mandated production cuts. Investment data should also rebound, given survey data suggest businesses are much more optimistic than third-quarter spending would suggest. The new North American trade pact and moves by the federal government to provide tax breaks on new investments will also help.

“My bias remains that the Bank of Canada would likely look through much of the oil price effect on the terms of trade as transitory –- and have more reasons to do so now,” Derek Holt, an economist at Bank of Nova Scotia, said in a note to investors, citing the production cuts. The firm sees four rate hikes next year. “I expect Poloz to signal that he remains on track with plans for gradual hikes.”

To contact the reporter on this story: Theophilos Argitis in Ottawa at targitis@bloomberg.net

To contact the editors responsible for this story: Theophilos Argitis at targitis@bloomberg.net, Chris Fournier, Stephen Wicary

©2018 Bloomberg L.P.