Baffled Analysts Have No Idea What They Want in Jobs Data

Anticipation is running hot. Anticipation of what, is a separate question.

(Bloomberg) -- While forecasting cause and effect is always hard in financial markets, Wall Street’s best minds are having a particularly brutal time deciding if they want Friday’s payroll data to come in high or low.

Anticipation is running hot. Anticipation of what, is a separate question. Will a weak report boost rate-cut odds? Or maybe the cuts are priced in and the sight of a tanking economy will sow terror. Maybe solid data will douse recession fears. Or maybe just stiffen resolve against easing.

Good may be good, or good may be bad. Wall Street is decidedly undecided.

Mixed economic data isn’t helping. A measure of U.S. manufacturing activity fell in May to the lowest level since October 2016. But U.S. household wealth hit a record in the first quarter and different measures of confidence have soared. Then again, a preview of private sector hiring wasn’t just ominous -- it was downright doomy. Data from ADP Research Institute showed companies in May added the fewest U.S. workers in any month since 2010.

Read here about BMO’s survey on Treasuries strategy post-payrolls.

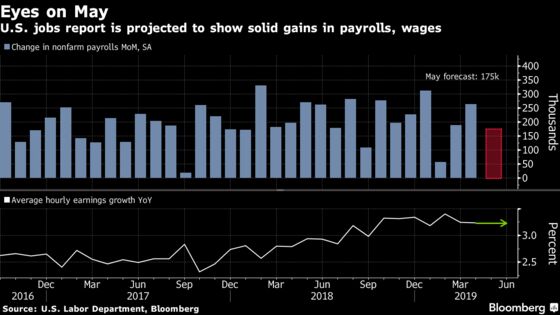

Economists are expecting an increase of 175,000 in payrolls on Friday, according to Bloomberg’s survey, with the unemployment rate staying at 3.6%. Here are four views from market watchers on the differing scenarios:

- Chris Gaffney, president of world markets at TIAA:

“That’s the crazy thing right now -- we’re back in this environment where a bad jobs report may actually help the markets because they look at that and they say ‘Well, now the Fed’s really going to come in with some more stimulus.’ It’s a case of if we get a really bad number, you could actually see stocks rebound somewhat.

We’ve seen some of that already. Valuations are decent right now, stocks aren’t as expensive as they were. And again, the U.S. economy is holding up fairly well. I think that a bad report, depending on just how bad it is and where we see it end up, if we see jobs decreasing that’s one thing, but wages are an important factor. If we see wages start to slip again, which I don’t expect, that could really come in and hurt the market because consumers are still fairly confident.”

- Jim Paulsen, chief investment strategist at Leuthold Group:

“If we see a really bad number, the market’s going to go down. If it’s anything close to the ADP number, and if it’s supported by the data -- pickup in unemployment and a really weak payroll number -- I think the market falls quite a bit. And the bond yield, more importantly, probably drops below 2% on the 10-year. That would be spooky. We’re not that far. It probably won’t happen, but I do think there’s a risk.”

“If we get a jump in claims and a bad report on Friday with jobs, I think the stock market will be back below 2,700 and the bond yield could be below 2%. There’s a risk of having a series of bad reports given where the market is right now. That’s why I do think the Fed needs to act -- or, they’ll be reacting on Friday after the fact, which won’t be as good.”

- Ed Campbell, managing director and portfolio manager at QMA:

If the report is strong, “then the case is that maybe the economy is not sinking as quickly and maybe the Fed is right to say, ‘Hey, we’ve got policy about right at this point, so bond market, you have probably overreacted and maybe that inverted yield curve needs to become less inverted.’ In that case, it might be good for stocks but bad for bonds. I personally would take comfort from a stronger report than a weaker report.”

“It should attract outsize attention because of the current context. U.S. economic growth looks like it lost momentum in the second quarter. We’ve had a string of disappointing economic data and with the trade tensions escalating and the trade war looking like it could be with us for a while, the odds for a deal seem to have declined pretty significantly over the past month. That’s something that could sour business and consumer confidence going forward. The U.S. labor market so far has been a pillar of strength despite clear signs of manufacturing slowdown.”

- Hank Smith, co-chief investment officer at Haverford Trust:

“You need to see multiple months of either a low print or a high print to get conviction on a trend. We’re not going to be too worried about it, but it [ADP] does show that business are cautious right now because of the uncertainty. The surprise part of that ADP was small businesses are actually seeing a contraction. That was a bit of a surprise and worth paying attention to. But again, you need to see several months to gain any type of confidence that a trend is being established.”

- Ilya Feygin, senior strategist at WallachBeth Capital LLC:

“If we get a strong jobs report, probably equities will decline slightly because the probability of a rate cut would decline. And a good part of this recent rally was due to more rate cuts priced. It also depends what average hourly earnings are.”

--With assistance from Sarah Ponczek.

To contact the reporters on this story: Vildana Hajric in New York at vhajric1@bloomberg.net;Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.