Bad News Weighs on Baht But Thailand's Bonds Are Re-Energized

Bad News Weighs on Baht But Thailand's Bonds Are Re-Energized

(Bloomberg) -- Anti-government protests and renewed concern about the virus’s impact on the economy are making the Thai baht one of the region’s worst-performing currencies. When it comes to the nation’s bonds, things are looking more positive.

The baht has suffered since protesters last month held the biggest demonstration since the military’s coup in 2014, and called for a general strike to put further pressure on the government. Optimism about the potential reopening of the country to tourism also received a setback in September as the detection of a locally transmitted virus case ended a run of 100 days without any transmission.

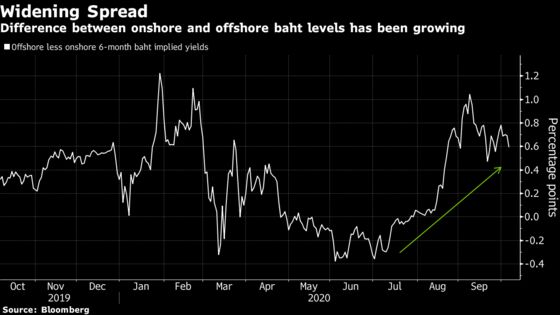

The pressure on the local currency can be seen in the widening yield difference between offshore and onshore forwards, which has expanded to a 60 basis-point premium from a 40 basis-point discount in July. The differential can be seen as a proxy for political risks, according to Duncan Tan, a strategist at DBS Group Holdings Ltd. in Singapore.

While the baht is underperforming, bonds are shrugging off the political unrest, and benefiting from haven demand caused by the virus. The most recent auction of 10-year debt last month drew a bid-to-cover ratio of almost 4 times, versus an average of 2.5 since the start of the 2020. A sale of 2038 securities also in September saw a ratio of 3.9 times.

“Auction bids have been healthy due to haven demand as the virus continues to weigh on the nation’s corporate outlook, the comparatively attractive domestic yields versus foreign returns, and moderate bond supply from corporates as well as the central bank,” said Jitipol Puksamatanan, head of market strategy at SCB Securities Co. in Bangkok.

The political protests haven’t been a deterrent for onshore investors, and healthy demand at bond sales is expected to continue at least into the final quarter, Jitipol said.

Inflows Recover

Foreign inflows into Thai debt have also bounced back. Overseas investors boosted holdings of the nation’s bonds by $1.4 billion last quarter, and have continued to be net buyers in October. That said, there’s still a long way to go to offset the $3 billion of outflows in the first half caused by the pandemic.

Fears of a potential oversupply of debt have also eased after the government announced it would only borrow 1.47 trillion baht ($47 billion) for the fiscal year starting Oct. 1, 11% lower than the previous 12 months. One reason behind the reduction is that the government has spent only a third of the planned 1.9 trillion baht stimulus it announced in May.

The benchmark 10-year bond yield has dropped to around 1.30%, from as high as 1.42% in August when concerns about oversupply were increasing.

While lingering concern about the government’s fiscal deficit is likely to cap any excessive exuberance in the local bond market, the increase in haven demand and the return of foreign funds mean there’s little reason to be worried about any sharp sell-off either.

What to Watch

- Malaysia will publish industrial-production data for August on Monday after July’s numbers showed factory output rose for the first time in five months

- Bank Indonesia will announce a monetary policy decision on Tuesday, and the government will release trade data on Thursday

- Thailand will auction 15 billion baht of new benchmark three-year bonds (LB246A) on Wednesday, along with 3 billion baht of 2071 securities (LB716A)

- The Philippines is scheduled to release remittance data on Thursday

Note: Marcus Wong is an EM macro strategist who writes for Bloomberg. The observations he makes are his own and not intended as investment advice.

©2020 Bloomberg L.P.