Bad Liquidity or Bad Markets? Traders Weigh in on Stock Tumult

Bad Liquidity or Bad Markets? Traders Weigh in on Stock Tumult

(Bloomberg) -- Seeing prices run away is part of doing business in smaller stocks. Seeing it happen when he was trying to fill an order in blue chips recently was something unusual for Beltran de la Lastra.

“If you go into the large caps and you try to do a significant trade -– let’s say in a big fund company of $200 billion you’re trying to do a $50 million clip, a $100 million clip -– you should be able to do it fairly quickly,” said de la Lastra, chief investment officer at Spanish asset manager Bestinver Gestion. “The reality is that you may have to be working on it for a few days.”

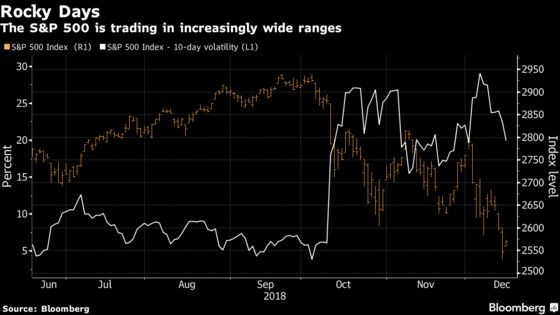

As a decade-long equity bull run starts to waver, liquidity risk -- the possibility markets will struggle to absorb selling demand without large price moves -- has been mentioned by everyone from Goldman Sachs to Donald Trump. Worries like that aren’t new and predictably increase when markets are in free fall, as they have been recently. But rarely have they gotten a bigger test than in the last few weeks.

Few topics on Wall Street get blood boiling faster than liquidity, particularly when worries about exchange structure are dragged in, as they are by critics who decry the supplanting of human market makers by machines. Those arguments may never be convincingly decided. But a few traders were willing to discuss what they saw over the last few weeks amid some of the toughest markets in a decade.

- Delores Rubin, senior equities trader at Deutsche Bank Wealth Management: “I’ve had my normal activity, I haven’t had anything out of the ordinary from what I would see this time of year in terms of being able to trade in and out of names that I have on both sides of the market,” she said. “It’s really about the timing. If you happen to have a huge block to move, and it’s during one of those times that there’s other movement in that same direction, it does become more difficult.”

- Jake Rappaport, head of equities at INTL FCstone Financial: “We’re having a sell-off, but we still have buy orders. With the tax selling and the year-end coupled with the political turmoil -- it’s scary, but I think it’s too soon to tell if people are going to stay on the sidelines,” he said. “Ultimately, they have to make a choice. Is the market giving them the price they’re willing to transact? ... The panic ‘Get me out’ trades, we just haven’t seen them yet.”

- Mike Beth, vice president for equity and derivative trading, WallachBeth Capital: “As the markets has been getting more volatile, we have been seeing an increase in the number of people wanting to get rid of large blocks as a whole, basically take out the timing risk of the stock moving. There are two things that we’re looking at every day, market impact and timing risk, and you want to find a happy medium between the two. When the market’s moving around like this, it increases people’s urgency to get rid of large quantities at once.”

- Joseph Saluzzi, Themis Trading LLC partner and co-head of equity trading: “By definition when volatility picks up, liquidity is thinner, It’s not new. In this time it’s been more dramatic -- I can judge that by the depth of liquidity in a particular quote. Maybe you’re used to seeing 5,000 shares on a bid -- you’re now seeing maybe half of that, or lower numbers. People are willing to supply less liquidity because they don’t want to get run over.”

The depth of the S&P 500 futures market has thinned by 70 percent over the past year to a new decade low, Goldman Sachs strategists led by John Marshall wrote in a note on Dec. 18. Single stock liquidity has fallen 42 percent over the past year to some of the lowest levels since the crisis, the bank said, citing a proprietary model.

The problem isn’t structural or related to high-frequency traders or passive products, Goldman contended. Simple risk aversion among professional investors is the more likely driver of reduced liquidity, rather than the growth in electronic trading, according to its strategists.

Evidence of risk aversion is everywhere, of course. More than $5 trillion has been erased from U.S. stock values in the last three months as the S&P 500 slid within points of a bear market. At the same time, share totals on U.S. exchanges have regularly exceeded 9 billion in the last few weeks, a fact mentioned by skeptics who say it’s to tough frame that much volume as a bust in liquidity.

Just because Goldman Sachs chalks it up to more sellers than buyers, it doesn’t mean everyone else does. Several investors spoken to for this article expressed concern that structural changes since the crisis have made the market more vulnerable.

Squishy Prices

Particularly in Europe, concern was voiced that spreads proved a bit less sturdy than versus recent history. Again -- perfectly ordinary, when markets go south. But a contingent of analysts and investors say that even given the relentless selling that has plagued markets since October, it doesn’t totally explain the squishiness of prices over the last few months.

A common theory of these investors is that passive funds sap liquidity when pressed into harmonized action and that their selling overwhelms high-frequency market makers -- a theory that academic research is skeptical of. Other critics cite post-crisis regulations that made it costlier for banks to hold positions.

“If you don’t play the market by trying to value one stock versus the other and those kinds of things, but by being in and out of the market, the minute you have a shift in the sentiment then it can reduce significantly the liquidity in the market,” said Francois Savary, chief investment officer at Prime Partners SA in Geneva.

Spreads have widened because of the market’s changing structure, according to Aram Green, fund manager at ClearBridge Investments in New York, though he doesn’t agree that liquidity has worsened.

“You’ll see a price on your screen of a stock down 30 dollars and you go to buy it and there’s no volume to buy it. And next thing you know it’s back to flat,” he said. At the same time, “we decide that we’re going to get out of half a million shares, and the thing only trades 300,000 shares a day and we put it out there in some dark pool, and it’s gone in 30 seconds. So you don’t know until you test it.”

--With assistance from Vildana Hajric, Elena Popina and Sarah Ponczek.

To contact the reporter on this story: Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Chris Nagi, Jeremy Herron

©2018 Bloomberg L.P.