Australia Will Need to Wean Itself Off Iron Ore Export Reliance

Australia Will Need to Wean Itself Off Iron Ore Export Reliance

(Bloomberg) -- Australia will have to get used to being less reliant on iron ore, with government forecasts showing price declines for the steel-making material will trigger a steep plunge in its resources export revenue within two years.

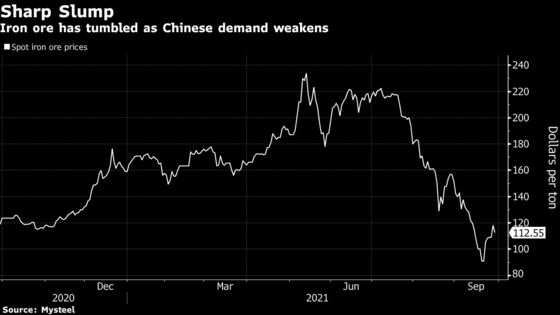

Prices of iron ore, which have halved since May as demand from China plunges, are set to average below $100 a ton next year, the Department of Industry, Science, Energy and Resources said in its latest quarterly report released Thursday. The price is currently trading at around $112 a ton.

The predicted entrenched price decline is the main catalyst for the department’s forecast that revenue from all commodities and energy exports will fall from a record A$349 billion ($253 billion) in the year to June 30, 2022, to A$299 billion a year later. In the two years from June 2021, it’s expecting the amount iron ore contributes to Australia’s resource sales will dive from about half to a third.

“Iron ore prices look to have peaked,” the department said. Earnings from the material over the next two years are expected to decline sharply, it said, adding that total resource export revenue will fall in the period “with world economic growth expected to be more moderate and the price of commodities to soften.”

Along with a hit to giant miners including BHP Group and Rio Tinto Group, the revenue plunge could have a big impact on Australia’s budget position, which has tumbled into a massive deficit due to pandemic stimulus and bailout spending.

Treasury forecasts the deficit will still be an elevated A$106.6 billion in the 12 months through June 2022, a figure that may actually worsen due to the government’s increased bailout spending for workers and companies impacted by lockdowns during the nation’s latest delta-variant outbreaks in recent months.

Australia’s longer-term export prospects are also complicated by its worsening geopolitical dispute with China that’s spilled into trade reprisals against imports of a range of goods including coal, barley, wheat and wine.

While top revenue-earner iron ore is yet to be affected by the spat, earlier this year Beijing pledged to slash its reliance on third parties for the steelmaking material over the next five years. For the time being, Australia remains responsible for more than 60% of China’s imports of iron ore.

Beyond iron ore, the report said the outlook for Australia’s mineral exports remains strong in the short term, as the world economy rebounds from the impact of the Covid-19 pandemic. “High prices, good volume growth and a weaker Australian dollar are driving a surge in export earnings” for now, it said.

Risk factors remain though, including a global inflation spike that could lead to higher interest rates, the shortage of semi-conductor chips, and a further deterioration in the trade relationship with China. Logistical problems exacerbated by the pandemic remain, with container shortages and other supply chain blockages adversely impacting global trade and output, and contributing to upward price pressure, it said.

| Key points from the report: |

|---|

|

©2021 Bloomberg L.P.