Australian Bonds Rally as RBA Lays Out Roadmap for Rate Cuts, QE

Australia Signals the Rally Bond Traders Wanted Isn’t Coming

(Bloomberg) -- The road map for quantitative easing laid out by Reserve Bank of Australia Governor Philip Lowe is spurring a rally in the nation’s bonds as investors seize on his comments to bet on deeper interest-rate cuts.

The nation’s sovereign debt rallied from the start of trade following Lowe’s speech late on Tuesday, and then extended gains when Westpac Banking Corp.’s economist Bill Evans predicted the central bank would cut borrowing costs to the 0.25% lower bound rate flagged by RBA. Three-year yields slid the most in seven months.

“The curve is steepening today as people trade the 0.25% view,” said Shane Oliver, head of investment strategy at AMP Capital Investors Ltd. “Longer-dated bonds will also start to anticipate those cuts at some point and that QE is still on the shopping list -- just not immediately.”

Lowe’s landmark speech on Tuesday, while highlighting his reluctance for quantitative easing, laid out the conditions required for the unorthodox measures as well as what the RBA would buy. While some analysts dialed back expectations for QE, others saw the road map as a sign that policy is inevitably headed that way.

The speech was a “clear signal to us that the RBA will be prepared to cut the cash rate” to 0.25% by June, Westpac’s Evans wrote in a research note. The central bank will embark on QE in the second half of next year, he said.

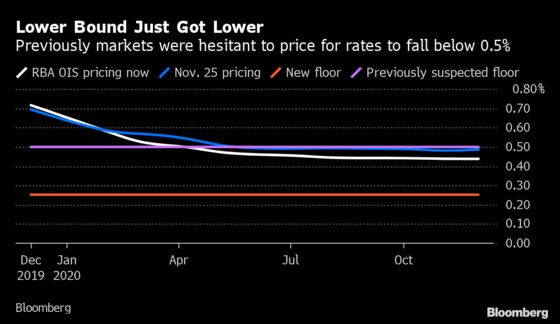

Bond traders had previously hesitated to price interest-rates falling below 0.50%, which they had assumed was the floor.

The three-year bond yield dropped as much as 10 basis points, the most since April, to 0.632%, while the 10-year fell six basis points to 1.018%.

Lowe made clear that the hurdle to QE is very high and “not a smooth continuum from interest-rate reductions.” If it comes, it is likely to be in the form of government-bond buying, with no appetite for purchasing private-sector assets, he said.

Corporate Bonds

Lowe’s comments on private asset purchases are expected to knock some of the wind from corporate bonds and residential mortgage-backed securities, according to Antares Capital.

“At the very least, this takes away the QE bid,” said Tano Pelosi, a portfolio manager who helps oversee A$28 billion ($19 billion) in assets at the firm in Sydney.

The average yield of Australian corporate bonds has tumbled 135 basis points to 1.69% this year on speculation unconventional monetary policy would boost the sector’s performance.

Still, investors have reason to question whether the RBA will limit itself to government bonds if it’s forced to plunge into unconventional policy.

The debt-buying programs of the European Central Bank have mutated since the initial foray in 2010, expanding to include corporate bonds and asset-backed securities. Tweaks have also been made to maturities and minimum yield levels on purchased assets.

“Any bond-buying program will still benefit the wider market,” AMP’s Oliver said. “Ultimately, there’ll be some sort of bid and ripples across markets if the RBA steps in as a buyer of government debt.”

To contact the reporters on this story: Ruth Carson in Singapore at rliew6@bloomberg.net;Stephen Spratt in Hong Kong at sspratt3@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Brett Miller, Nicholas Reynolds

©2019 Bloomberg L.P.