Australia's ASX Prepares for Negative Interest-Rate Trading

Australia's ASX Prepares for Negative Interest-Rate Trading

(Bloomberg) -- Australia’s ASX Ltd. is testing its systems for the trading of negative interest-rate products, underscoring how markets are preparing for the potential introduction of quantitative easing in yet another Group-of-10 nation.

The exchange has made available trial environments so market participants can test their processes for interest-rate futures prices that are greater than or equal to 100.00, according to a July 10 market notice. The firms taking part include JPMorgan Securities Australia Ltd, Goldman Sachs Australia Pty and HSBC Bank Australia Ltd.

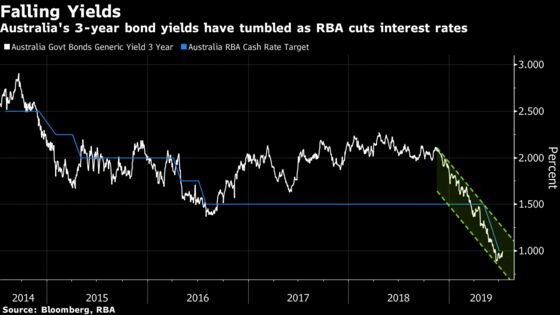

Australia’s three-year bond yield slid below 1% in June for the first time, while the Reserve Bank of Australia has cut interest rates twice this year to counter slowing growth. Although Governor Philip Lowe has said it’s unlikely policy makers would need to implement negative rates, some economists have started flagging the possibility should growth stay below expectations.

“Our testing is based on the fact of two recent rate cuts in Australia that have resulted in interest rates at record lows,” Matthew Gibbs, a spokesman for the ASX, wrote in an email reply to Bloomberg queries. “Our requirement for testing is to ensure that participants are prepared in the event that the market expects further cuts.”

The amount of negative-yielding bonds globally has jumped 47% this year to more than $12 trillion as signs the Federal Reserve and European Central Bank will boost monetary easing spurred a rally in debt around the world. There are currently no Australian bonds with yields below zero.

The RBA cut its benchmark cash rate to 1% this month, with Lowe signaling a willingness to ease further if needed. The three-year yield dropped to a record 0.883% in June, and was at 0.997% on Monday.

The ASX24 trading platform currently restricts orders entered in interest-rate futures products where prices are greater than or equal to 100.00, while option strike listings are also currently contained to under 100.00.

The tests are important for ASX’s listed bank bills, bond futures and options, given the products have a “variable tick” that changes in accordance with the underlying interest rate, Gibbs said. The trials will run through to Aug. 9, according to the notice.

According to its website, ASX’s A$47 trillion ($33 trillion) interest-rate derivative market is the largest in Asia.

“With interest rates globally moving further into negative territory, it’s just part of prudent management to do the testing,” said Prashant Newnaha, senior rates strategist at TD Securities Inc. in Singapore.

To contact the reporters on this story: Tommi Utoslahti in Singapore at tutoslahti1@bloomberg.net;Ruth Carson in Singapore at rliew6@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, ;Garfield Reynolds at greynolds1@bloomberg.net, Nicholas Reynolds

©2019 Bloomberg L.P.