Asset Bubbles Are Just Fine If They Don't Go Pop

Asset Bubbles Are Just Fine If They Don't Go Pop

(Bloomberg) --

With oil prices getting so much attention, central banks have slipped out of focus for markets. That’s all about to change today with the Fed policy announcement due later. Following the ECB’s stimulus package last week, the U.S. central bank could opt to provide some market support, but lurking in the background is the threat of a credit bubble.

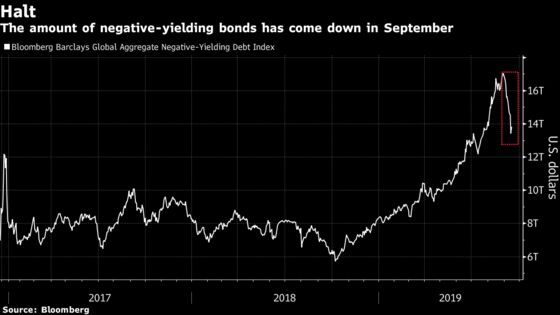

There are some obvious warning signals. Falling government yields have pushed investors toward riskier sovereign bonds and corporate credit. The very fact that globally, bonds with a negative yield recently reached an astonishing $17 trillion -- 30% of the total outstanding market value of global bonds -- is one big sign, even though the level has slipped back this month.

Corporate credit has rarely been this rich relative to equities, according to strategists at Societe Generale. If this makes stocks relatively attractive in the short term, the risk increases in the medium term as the credit bubble is puffed up by central banks, Bank of America strategists say. That’s why BofA is bullish on risk assets this year but expect the bubble to burst in 2020, which would drag down equity markets in the process.

Even if you’re a pure equity investor, tensions on the credit market can’t be ignored, as a credit bubble would surely take down the stock market, just like it did back in 2008. At the moment, the equity-risk premium still looks extreme in Europe, theoretically favoring equities over bonds.

“Central banks are pumping money into a global economy that is slowing down structurally,” says Sebastien Galy, senior macro strategist at Nordea Investment Funds. That is increasing demand for assets with limited supply, leading to bubbles from gold to real estate and also fixed income, he says.

Galy isn’t alone worrying about inflated asset prices. UBS CEO Sergio Ermottiwarned in July that the ECB’s stimulus could create asset bubbles. The debate seems to be heating up as ECB governors representing the core of the euro-area economy resisted President Mario Draghi’s ultimately successful bid to restart quantitative easing.

As for the Fed, it has more room to maneuver after some deleveraging. The case for a rate cut is also strengthening after this week’s spike in oil prices. The odds of an interest-rate cut are currently at 100%. Given the tensions on the repo market, it seems the Fed may have some trouble controlling short-term funding rates.

In the meantime, Euro Stoxx 50 futures are little changed ahead of the European open, while S&P 500 contracts are down 0.1%.

- Watch European logistics operators after U.S. group FedEx slashed its profit outlook, sending its shares plummeting in extended trading. Watch Deutsche Post, Royal Mail, Bpost, PostNL, Austrian Post and Poste Italiane.

- Watch the pound and U.K. stocks as the U.K. Supreme Court will continue to examine the legality of Prime Minister Boris Johnson’s parliamentary proroguing over the next few days.

- Watch oil stocks as Brent and WTI futures edged lower on Wednesday after tumbling Tuesday after Saudi Aramco said it had revived 41% of capacity at a key crude-processing complex

- Watch Spanish stocks including utilities, real estate and banks after the country’s political parties failed to agree on creating a new governing alliance, setting Spain up for new elections in November.

COMMENT:

- “Value/growth saw its biggest one-day gain in a decade last week, but many are skeptical about a prolonged style rotation,” Barclays strategists write in a note. “Taking a stance against Value has worked well for a while, but we think the recent reversal could have legs, irrespective of market conditions. Crowded positioning and stretched valuations make growth vulnerable to either a broadening of the macro slowdown, or a revival of the reflation trade.”

NOTES FROM THE SELL SIDE:

- Morgan Stanley begins coverage of European fertilizers with a preference for OCI (overweight) and Yara (equal-weight). MS favors urea players over potash, with K+S started at underweight. The urea preference is based on better operational, cash flow and ROIC development, scope for special returns and asset monetization.

- BMW is cash rich, while Jaguar Land Rover is severely challenged and could “massively” lower costs under a bigger partner, so BMW and JLR’s Indian parent Tata need to talk, Bernstein analysts say in research report.

- European banks which have self-help angles to improve returns and those with underpinned dividends are RBC’s preferred picks in the sector. UniCredit remains top pick, ING, BNP Paribas, DNB and Swedbank all outperform; “more skeptical” about return potential of Commerzbank, Deutsche Bank and Nordea.

COMPANY NEWS AND M&A:

- Europe Car Industry Woes Deepen as August Sales Drop Sharply

- EON Said to Hire BNP to Sell $1.1 Billion Czech Retail Business

- Total CEO Fears Attacks in Saudi Arabia May Trigger Retaliation

- Novartis Sees Kisquali Becoming Blockbuster: Schaffert in FuW

- Atlantia CEO Giovanni Castellucci Resigns

- Facebook Enlists Luxottica to Develop Smart Glasses: CNBC

- German Bafin Fines Deutsche Wohnen EU427,000 Over Late Reporting

- Kingfisher First Half Sales Meet Estimates

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 395.1 (July high); 397.9 (June 2018 high)

- Support at 381.1 (50-DMA); 373.2 (200-DMA); 365.5 (50% Fibo)

- RSI: 62.9

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,573 (July high); 3,596 (May 2018 high)

- Support at 3,435 (50-DMA); 3,403 (61.8% Fibo); 3,328 (200-DMA)

- RSI: 62.6

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Kemira Oyj upgraded to hold at HSBC; PT 12 Euros

- Kering upgraded to buy at UBS; PT Set to 550 Euros

- Severstal GDRs upgraded to overweight at Alfa-Bank; PT $17.60

- TLG Immobilien upgraded to buy at Bankhaus Lampe; PT 29 Euros

DOWNGRADES:

- BAM downgraded to hold at ABN Amro Bank; PT 2.85 Euros

- Beiersdorf downgraded to sell at Goldman; PT 100 Euros

- Elisa Oyj downgraded to underweight at JPMorgan; PT 42 Euros

- Hexagon downgraded to hold at Handelsbanken; PT 525 Kronor

- Kinnevik downgraded to hold at SEB Equities; PT 274 Kronor

- Kuehne + Nagel downgraded to neutral at MainFirst; PT 150 Francs

- Mediclinic cut to reduce at HSBC; Price Target 3.10 Pounds

- Richemont downgraded to sell at UBS

- Telefonica downgraded to hold at Renta 4; PT 7.20 Euros

- Weir downgraded to neutral at JPMorgan; PT 15 Pounds

INITIATIONS:

- Aroundtown rated new overweight at Barclays; PT 8 Euros

- K+S rated new underweight at Morgan Stanley; PT 13.70 Euros

- Swatch rated new sell at UBS; PT 217 Francs

- TLG Immobilien rated new underweight at Barclays; PT 23 Euros

MARKETS:

- MSCI Asia Pacific down 0.4%, Nikkei 225 down 0.2%

- S&P 500 up 0.3%, Dow up 0.1%, Nasdaq up 0.4%

- Euro down 0.05% at $1.1067

- Dollar Index up 0.03% at 98.29

- Yen down 0.09% at 108.23

- Brent little changed at $64.6/bbl, WTI down 0.5% to $59/bbl

- LME 3m Copper up 0.3% at $5837.5/MT

- Gold spot little changed at $1501.9/oz

- US 10Yr yield little changed at 1.8%

ECONOMIC DATA (All times CET):

- 10am: (IT) July Industrial Sales WDA YoY, prior -0.8%

- 10am: (IT) July Industrial Sales MoM, prior -0.5%

- 10am: (IT) July Industrial Orders NSA YoY, prior -4.8%

- 10am: (IT) July Industrial Orders MoM, prior -0.9%

- 10:30am: (UK) Aug. CPIH YoY, est. 1.9%, prior 2.0%

- 10:30am: (UK) Aug. CPI MoM, est. 0.5%, prior 0.0%

- 10:30am: (UK) Aug. CPI YoY, est. 1.9%, prior 2.1%

- 10:30am: (UK) Aug. CPI Core YoY, est. 1.8%, prior 1.9%

- 10:30am: (UK) Aug. Retail Price Index, est. 291.4, prior 289.5

- 10:30am: (UK) Aug. RPI MoM, est. 0.7%, prior 0.0%

- 10:30am: (UK) Aug. RPI YoY, est. 2.6%, prior 2.8%

- 10:30am: (UK) Aug. RPI Ex Mort Int.Payments (YoY), est. 2.5%, prior 2.7%

- 10:30am: (UK) Aug. PPI Input NSA MoM, est. -0.2%, prior 0.9%

- 10:30am: (UK) Aug. PPI Input NSA YoY, est. -0.1%, prior 1.3%

- 10:30am: (UK) Aug. PPI Output NSA MoM, est. 0.2%, prior 0.3%

- 10:30am: (UK) Aug. PPI Output NSA YoY, est. 1.7%, prior 1.8%

- 10:30am: (UK) Aug. PPI Output Core NSA MoM, est. 0.2%, prior 0.4%

- 10:30am: (UK) Aug. PPI Output Core NSA YoY, est. 2.0%, prior 2.0%

- 10:30am: (UK) July House Price Index YoY, est. 0.6%, prior 0.9%

- 11am: (IT) July Trade Balance Total, prior 5.73b

- 11am: (EC) July Construction Output MoM, prior 0.0%

- 11am: (EC) July Construction Output YoY, prior 1.0%

- 11am: (EC) Aug. CPI Core YoY, est. 0.9%, prior 0.9%

- 11am: (EC) Aug. CPI MoM, est. 0.2%, prior -0.5%

- 11am: (EC) Aug. CPI YoY, est. 1.0%, prior 1.0%

- 11am: (IT) July Trade Balance EU, prior 1.88b

- 12:50pm: (EC) ECB’s Guindos Speaks in Madrid

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.