S&P 500 Tops Record in Data-Rich Week; Bonds Drop: Markets Wrap

All you need to know about what’s moving markets today.

(Bloomberg) --

U.S. stocks rose above their record high at the start of a week packed with data that will provide clues on global economic growth. Bonds fell.

Financial companies led gains in the S&P 500 Index, while real-estate shares retreated. Benchmark Treasury yields climbed after a large five-year block sale. The U.S. dollar was little changed and the euro rallied. Crude had a volatile session as a severe crackdown on Iranian oil exports ticked closer.

Investors are assessing whether the economy and corporate earnings will continue to support the equity bull run. U.S. consumer spending rebounded in March while the Federal Reserve’s preferred underlying inflation gauge eased to a one-year low, according to a Commerce Department report on Monday. Policy makers are expected to hold rates steady on Wednesday, though new growth and prices data may affect their characterization of the economy.

The next round of trade talks with China will get under way this week with significant issues still unresolved, but with enforcement mechanisms “close to done,” according to U.S. Treasury Secretary Steven Mnuchin.

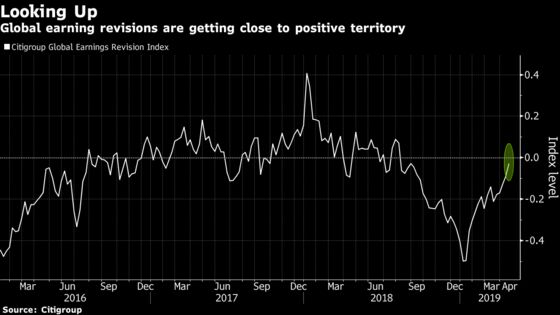

“There’s a lot of things from a macro standpoint that appear to be pretty supportive of the stock market,” said Mark Stoeckle, chief executive officer of Adams Funds, which has about $2.5 billion in assets under management. “The Fed pivoted, and trade -- at least on the surface -- appears to be progressing in the right direction. In addition to that, you see a lot of companies that are reporting some pretty good numbers.”

Almost 80 percent of the S&P 500 companies that have reported quarterly earnings beat analyst estimates, data compiled by Bloomberg show. The results are looking good as the bar had been lowered coming into this season, said Michael Hans, chief investment officer at Clarfeld Financial Advisors.

Elsewhere, the Stoxx Europe 600 Index rebounded as a rally in banks outweighed a drop in euro-area economic confidence to a two-year low. Markets in Japan remained shut for holidays, with many others set to follow suit on May 1.

Here are some notable events coming up:

- Companies reporting earnings include: Apple, GE, Pfizer, HSBC, Macquarie, BP, Royal Dutch Shell and McDonald’s.

- U.S. Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin travel to Beijing to continue trade talks. China and the U.S. hope to seal a deal by early May.

- Euro-zone GDP data and China’s manufacturing PMI are due on Tuesday.

- The U.S. Fed’s rate decision is on Wednesday, while the Bank of England sets interest rates Thursday.

- Friday brings the U.S. jobs report: non-farm payrolls are projected to rise by 187,000 in April. Economists expect an unemployment rate of 3.8 percent, with average hourly earnings growth picking up to 3.3 percent.

These are the main moves in markets:

Stocks

- The S&P 500 rose 0.1 percent to 2,943.03 at 4 p.m. in New York.

- The Stoxx Europe 600 Index increased 0.1 percent.

- The MSCI Asia Pacific Index advanced 0.3 percent.

- The MSCI Emerging Market Index added 0.5 percent.

Currencies

- The Bloomberg Dollar Spot Index was little changed.

- The euro climbed 0.3 percent to $1.1185.

- The British pound rose 0.2 percent to $1.2937.

- The Japanese yen fell 0.1 percent to 111.67 per dollar.

Bonds

- The yield on 10-year Treasuries rose three basis points to 2.53 percent.

- Germany’s 10-year yield climbed three basis points to 0.00 percent.

- Britain’s 10-year yield increased two basis points to 1.157 percent.

Commodities

- The Bloomberg Commodity Index declined 0.3 percent.

- West Texas Intermediate crude settled at $63.50 a barrel.

- Gold fell 0.6 percent to $1,281.50 an ounce.

--With assistance from Yakob Peterseil, Adam Haigh, Robert Brand, Todd White, Sarah Ponczek and Lu Wang.

To contact the reporters on this story: Rita Nazareth in New York at rnazareth@bloomberg.net;Vildana Hajric in New York at vhajric1@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Rita Nazareth

©2019 Bloomberg L.P.