Asia’s Red-Hot Bond Funds Are Raising Risks For Investors

With the fixed-maturity funds, there are risks that their managers will reduce payouts if weaker bonds they hold default.

(Bloomberg) -- An increasingly popular financial product in Asia that invests in bonds is coming under greater scrutiny as concerns about risks to individual investors mount.

The so-called fixed-maturity funds typically offer regular payouts, but don’t guarantee returns even if some cite targets. While the funds can provide stable income, in times of market strains that can crumble. A limited menu of options given the requirements on maturities mean fund managers may at times need to load up on riskier notes.

The red hot rally in Asia credit this year has prompted yield-hungry investors to flock to these funds, with increasing participation from mom and pop buyers. That’s expanded risks, as nonpayments in the Asia dollar note market have picked up in the past two months. Wealthy investors had already been borrowing money to buy into the products. Read more about that here.

“Some funds are sensitive to ratings and in the event of a default or credit event, this could trigger forced selling,” said Anne Zhang, head of fixed income for Asia at JPMorgan Private Bank.

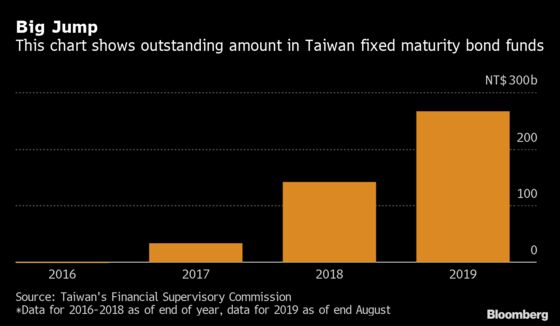

Taiwan’s regulator last month tightened rules, after NT$266.1 billion ($8.7 billion) had poured into the funds in Taiwan as of August, eight times the outstanding amount at the end of 2017. BEA Union Investment Management estimates that such funds have raised over $1.5 billion from the retail market in Hong Kong this year.

Individuals are making riskier investments in countries from South Korea to Singapore in a range of products as falling global interest rates drag down returns.

With the fixed-maturity funds, there are risks that their managers will reduce payouts if weaker bonds they hold default.

Taiwan’s regulator gave verbal guidance to fund companies due to the popularity of fixed-maturity products, asking the firms to not focus solely on their sale but to intersperse them with other products, said Taiwan’s Financial Supervisory Commission department head Ku Kun-jung.

The key risk investors face is the “funds’ underlying bonds defaulting on interest or principal payment,” according to Eric Fang, portfolio manager at Eastspring Investments. The firm has raised almost 1.1 billion pounds ($1.4 billion) this year from fixed-maturity funds and has been “proactively working” on alternatives for new product development for 2020, said Xavier Meyer, head of distribution at Eastspring Investments.

‘Forced Selling’

Fixed-term bond funds sold to retail and wealthy investors received nearly $7 billion of net flows during the 12 months ending June this year, according to Morningstar Direct data covering Taiwan, Hong Kong, Singapore, Japan and Australia.

Unlike a high-yield fund, the fixed-maturity products typically don’t take bets on distressed bonds. If the credit quality of a company weakens, this can prompt a wave of selling.

Current default rates are low compared to the financial crisis period, and the risks related to such funds are “still managable,” according to Manulife Investment Management fund manager Megan Chung, who runs three fixed-maturity bond funds.

The popularity of such products is also affecting liquidity in the broader market, as they adopt a buy and hold strategy.

“The voracious demand for these fixed-maturity products could certainly result in a shrunken pool of available assets, since they are essentially ‘put away’ in these funds and not available to be traded anymore,” said Todd Schubert, head of fixed income research at Bank of Singapore Ltd.

To contact the reporters on this story: Denise Wee in Hong Kong at dwee10@bloomberg.net;Miaojung Lin in Taipei at mlin179@bloomberg.net

To contact the editors responsible for this story: Andrew Monahan at amonahan@bloomberg.net, Ken McCallum

©2019 Bloomberg L.P.