Best Asia Bond Rallies at Risk of Pricing in Too Much Easing

Some money managers have begun to warn the trade of Indian and Indonesian bonds is getting risky.

(Bloomberg) -- Follow Bloomberg on LINE messenger for all the business news and analysis you need.

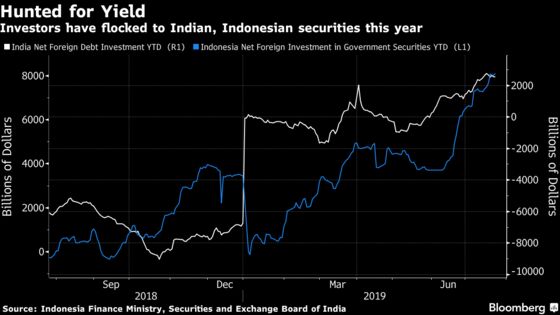

The global hunt for yield has led to a surge in demand for Indian and Indonesian bonds this year, but some money managers have begun to warn the trade is getting risky.

Foreign investors have poured over $11 billion into rupee and rupiah bonds this year, after a combined $3 billion withdrawal in 2018. An enthusiasm for easy monetary policy that may have gone too far and uncertainty over the U.S.-China trade war raises the specter that inflows could reverse, according to investors including S.E.A. Asset Management Pte and Schroder Investment Management Ltd.

“The EM Asia market outlook has seen a boost from the Fed comments which will bring only short-term relief to markets,” said Alexander Zeeh, chief executive officer of S.E.A. Asset in Singapore, referring to Chair Jerome Powell’s dovish testimony to lawmakers earlier this month. “We would caution regarding the robustness of Asian economies amid reduced trade and falling PMIs. Eventually markets and riskier assets could still sell off.”

With global markets in a renewed era of monetary easing, bond investors have been quick to move to markets where yields are high and there is ample room for rate cuts. Indian sovereign bonds have capped a third month of gains, with benchmark yields down 100 basis points this year to 6.37% Wednesday, while their Indonesian equivalents have fallen over half a percentage point to 7.37% -- among the biggest declines in Asia.

For PineBridge Investments, which favors rupee and rupiah securities, emerging-market bonds now face the risk that any easing by the Fed could fall short of market expectations.

“Considering how much easing has already been discounted by European debt markets and the rally this year in U.S. Treasuries, any signs the central bank will be unwilling to back up their dovish rhetoric with easing action would be negative for risk markets,” said London-based PineBridge fund manager Anders Faergemann.

Read why SocGen sees no EM currency rally from a Fed rate cut

Fed Chair Jerome Powell looks poised to cut interest rates by a quarter percentage point on Wednesday, with traders pricing in roughly two more by the beginning of next year, according to futures markets. Yet with U.S. economic data still relatively strong, uncertainty over the pace of cuts remains high.

While Indonesia lowered its benchmark interest rate for the first time in almost two years on July 18, after raising it by 175 basis points in 2018, its Indian counterpart has already cut three times this year. Reserve Bank of India Governor Shaktikanta Das said last week policy makers have effectively delivered more easing than the cuts suggest, signaling a key pillar of support for Indian debt could soon disappear.

Trade Woes

On the growth front, the U.S.-China trade war continues to loom large over the region’s economy and markets. Washington and Beijing concluded a new round of talks in Shanghai on Wednesday with little immediate evidence of progress.

“With weakening exports, it is unlikely that EM Asia will post very strong economic data in the coming quarter,” said Manu George, director of fixed income in Singapore at Schroder Investment. Given the uncertainty about talks “between the Chinese and U.S. trade negotiators, EM Asian bond performance will likely oscillate for a while.”

The prospect of U.S. tariffs on Indian goods and a spat between South Korea and Japan have only added to the fallout from the ongoing Sino-American dispute, according to S.E.A.’s Zeeh.

Easing Cycle

Still, for Todd Schubert, head of fixed-income research at Bank of Singapore Ltd., it all comes back to the Fed. As long as central banks keep their easing bias, EM Asian bonds stand ready to benefit, he said.

“The Fed’s (still anticipated) rate cut will set off a global monetary easing cycle as other central banks follow suit that will be positive for risk assets,” Schubert said. Foreign “inflows into higher beta markets such as India and Indonesia should increase as global monetary easing encourages a risk-on, search for yield environment.”

To contact the reporters on this story: Liau Y-Sing in Kuala Lumpur at yliau@bloomberg.net;Hooyeon Kim in Seoul at hkim592@bloomberg.net;Kartik Goyal in Mumbai at kgoyal@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Cormac Mullen

©2019 Bloomberg L.P.