As Credit Fears Snowball, Hedge Fund Places Short-Volatility Bet

As Credit Fears Snowball, Hedge Fund Places Short-Volatility Bet

(Bloomberg) -- A hedge fund is placing a risky wager equivalent to 11 percent of its volatility portfolio that the fear gripping global debt markets will prove short-lived.

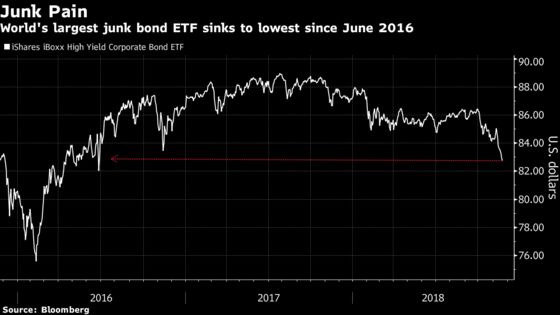

Credence Capital, the volatility-trading arm of KM Cube Asset Management with 110 million euros ($125 million), is shorting expected price swings in the world’s largest junk-bond ETF, which has nose-dived this month in the most violent upheaval since 2016.

Greece-based Credence is selling put options on the iShares iBoxx High Yield Corporate Bond exchange-traded fund to anxious investors who have sent the price of the derivatives soaring in an attempt to shield themselves from further pain.

The trade is looking too good to pass up as a seemingly indiscriminate sell-off in risk assets pushes volatility premiums to levels last seen in the blowout in equity swings earlier this year.

“Credit was never an easy market to short,” said Yannis Couletsis, director at Credence. “But this kind of vol risk premium is the highest since the February volmageddon.”

The trade will profit if volatility falls and the price of the ETF doesn’t decline too sharply, or rises. Selling vol has traditionally been the domain of equity investors, who use derivatives to bet that price swings in stocks will be more subdued than those implied by options prices. In so doing, they are taking advantage of the so-called volatility risk premium, or the asymmetry between sellers -- who expose themselves to the prospect of unlimited losses in tail scenarios -- and option buyers, whose pain is limited by the premium paid.

As jitters have spread to markets like commodities and credit however, these risky strategies, which are prone to spectacular blow-ups, have followed suit.

Credit Caution

Cracks in credit markets are widening as investors fret over everything from rising rates, slower growth and oil prices. U.S. junk spreads have widened the most since December 2016 and yields have risen to a 30-month high in November.

“In the past few days we are observing higher vol in assets other than equities,” said Couletsis. In addition to shorting volatility of the iShares bond fund, the firm has also been selling it on the Brexit-battered British pound and oil.

With some $14 billion in assets and a robust derivatives and shorting market, the iShares High Yield ETF, known as HYG, is a popular venue for junk traders to express their views. Short interest in the fund is above this year’s average, while its implied volatility has soared to the highest since February.

With over-the-counter credit derivatives opaque and difficult to access, Couletsis sees HYG as a “good enough alternative.”

He’s not the only one advocating the trade.

“Unless the cycle ends soon, we think that earning the risk premium in HYG offers good risk reward,” Macro Risk Advisors strategists Mayank Seksaria and Vinay Viswanathan wrote in a Nov. 20 note.

“Substantial buying of protection in HYG” has made put options on the fund “expensive,” the strategists wrote. It’s advocating a strategy for harvesting the volatility-risk premium known as a put spread, where options are simultaneously bought and sold on HYG.

Shorting volatility can be immensely profitable -- until it’s not. Scores of S&P 500 volatility sellers got caught unawares in February when the VIX surged, leaving at least one shattered exchange-traded product in its wake.

More recently, violent swings in energy prices led to the demise of a hedge fund devoted to writing options contracts.

For Macro Risk Advisors, the risks to the HYG trade include an abrupt end to the economic cycle, a blow-up in high yield due to stress in the energy sector or structural problems in the passive space that could cause more violent price swings than anticipated.

“Ours is a tactical trade from which we will probably be out before it expires next month,” said Couletsis.

To contact the reporter on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Todd White

©2018 Bloomberg L.P.