Aramco Bond Sale So Popular That Yield Premium May Be Near Zero

Aramco Bond Sale So Popular That Yield Premium May Be Near Zero

(Bloomberg) -- The demand for Saudi Aramco’s debut issue of debt is so strong that the world’s largest oil producer may need to offer only a small premium to the kingdom’s bonds. Even that spread may vanish, some investors say.

“Aramco’s bond is likely to be very well subscribed given its strong credit profile,” said Anita Yadav, head of fixed-income research at Emirates NBD in Dubai. “Depending on the tenure, the pricing on Aramco could be zero to up to 20 basis points wider than the relevant Saudi government curve.”

Aramco was the world’s most profitable company in 2018, surpassing Apple Inc. and Exxon Mobil Corp., according to accounts published by ratings agencies before the firm’s debut in the international bond market. It enjoys the fifth-highest investment grade rating at both Moody’s Investors Service and Fitch Ratings as it plans meetings with global investors this week to market its debut dollar bond offering. It’s selling debt with maturities ranging from three to 30 years, investors said.

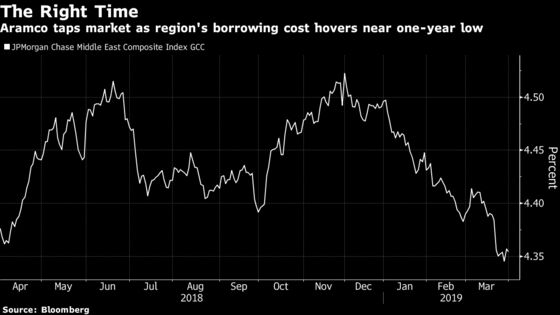

Proceeds from the sale, which Saudi Energy Minister Khalid Al-Falih said in January could be about $10 billion, will be used to help fund its purchase of a 70 percent stake in Saudi Basic Industries Corp. Saudi Arabia’s sovereign-debt yields have declined this year, making it cheaper for Aramco to borrow. Brent crude has also advanced 28 percent since end-December.

While Aramco has many characteristics of an Aaa-rated company -- including minimal debt relative to cash flows and access to one of the world’s largest hydrocarbon reserves -- the final rating is constrained by the government’s A1 rating, Moody’s says.

Here’s what some investors say about Aramco’s bond offer:

Richard Segal, a senior emerging-markets analyst at Manulife Asset Management in London:

- “This launch has been eagerly awaited for some time and strong demand has already preceded it”

- Aramco is set to trade flat to or as much as 10 basis points wider than the sovereign yield curve for a 10-year maturity, until investors become familiar with the oil producer as a credit

- Sabic’s 2028 debt is trading at 25 basis points above the sovereign, while Saudi Electricity Co.’s bond of similar maturity at a yield premium of about 43 basis points

- Aramco’s bonds will trade in line with these or slightly tighter

- Aramco “is obviously highly profitable, though there is the potential for its balance sheet to become more leveraged, which will count against it”

Sergey Dergachev, senior portfolio manager at Union Investment Privatfonds GmbH in Frankfurt:

- Aramco may offer a yield premium of 20 basis points to 40 basis points to the sovereign

- It is unlikely that Aramco will come flat to the kingdom’s yield curve

- “There is no case of a quasi-sovereign trading inside sovereign in EM that is known to me, especially if it also a debut issue”

- “Aramco will be debut issuer and some new issue premium is needed by investors to place a successful deal”

- “Demand will be immense, since there is very small supply out from Saudi corporate sector,” and investors in the U.S. and the Gulf region are set to dominate bids

- “The fact that Aramco finally decided to go with the deal is a very strong positive confirmation to investors that it is implementing its plans and trying to open itself up incrementally for investors”

--With assistance from Mohammed Aly Sergie.

To contact the reporters on this story: Netty Ismail in Dubai at nismail3@bloomberg.net;Archana Narayanan in Dubai at anarayanan16@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Srinivasan Sivabalan, Alex Nicholson

©2019 Bloomberg L.P.