AQR's Asness Is Right. It's a `Crappy' Time for Factor Investing

AQR's Asness Is Right. It's a `Crappy' Time for Factor Investing

(Bloomberg) -- When the ultimate champion of factor investing uses the words “crappy” and “terrible” to describe recent performance, you know times are tough in quant land.

Cliff Asness, pioneer of quantitative trading and co-founder of industry giant AQR Capital Management LLC, remains an avowed proponent of strategies that pick stocks based on common traits like quality or value. But he got blunt about the current miserable climate while speaking at a conference last week.

And hit the nail on the head.

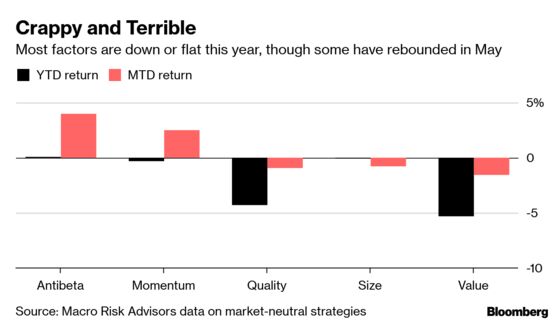

All five major equity factors tracked by Macro Risk Advisors are down or nearly flat this year, while the S&P 500 boasts a 14% gain even after this month’s pullback. The same trade war turbulence is also making it harder to see factors breaking out of their funk any time soon.

“It’s not just one factor that’s not working,” said Ian Heslop, London-based head of global equities at Merian Global Investors, who manages the firm’s absolute return fund. “It’s a material cross-section of standard factor implementations that are not predicting stock returns at the moment.”

One of the big issues: the nature of these late-cycle stock gyrations.

Risk appetite and economic growth expectations haven’t been strong enough to help revive a factor like value, which tends to be made up of cheaper and thus riskier equities. Others, like quality and low-volatility, have looked out of tune with the new year rally -- not to mention they had become expensive thanks to their haven appeal in late 2018.

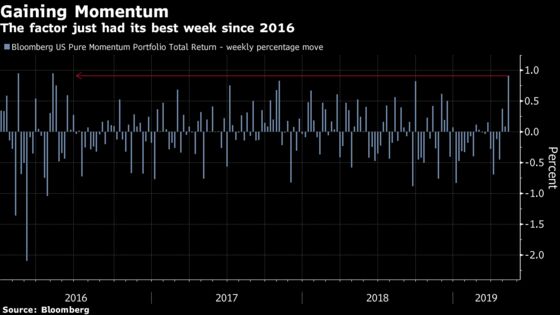

Even the momentum factor, which has made money in eight of the last 10 years, plunged in 2019. The strategy of buying winners of the past year and selling its losers became loaded with more defensive bets in the fourth quarter, and they turned into laggards as the S&P 500 surged in the new year.

That defensive positioning contributed to a rebound for momentum last week, according to a simplified version of the strategy represented by a Bloomberg index. But with the global stock sell-off losing some steam -- the S&P 500 jumped on Tuesday and was 0.7% higher as of midday in New York -- it’s unclear if defensive shares will sustain the performance.

A resumption of the 2019 rally may hammer the momentum factor anew.

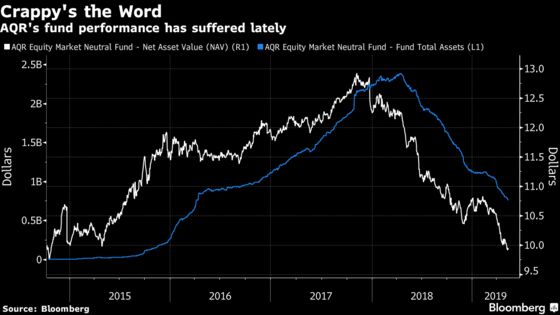

Asness’s own AQR Equity Market Neutral Fund is set for its fifth straight monthly decline, but he is by no means alone. Other funds, like the $1 billion Vanguard Market Neutral Fund and the BMO Global Equity Market Neutral V6 Fund, have also lost money in 2019.

Despite the challenging conditions and his colorful remarks, Asness told the Morningstar conference in Chicago he intends “to stick like grim death” to his beliefs and work on improving his explanations to help investors.

Proponents argue that recent factor underperformance is statistically nothing out of the ordinary and needs to be considered in the long term. If and when portfolios rebound, these declines might seem like a blip in retrospect. Asness reckons stock valuations are currently stretched to levels not seen since the 1990s tech bubble -- a signal that his strategies may be ready to pay off.

For now, the headache is that factor declines have been occurring in concert. Sanford C. Bernstein noted earlier this year that rising correlations in the field, which reached the highest in at least two decades, have made it harder for quants to generate idiosyncratic returns and stave off unwanted risks.

For instance, both value and momentum -- two factors that in the past have moved in opposite directions -- have dropped together in the last two quarters.

“If no one particular factor or theme is dominant -- think momentum in 2017 when FAANG stocks led the market higher, or low-beta in 2008 -- factor investment will show significant underperformance when juxtaposed against a positively-trending market benchmark,” said Maxwell Grinacoff, a quantitative strategist at Macro Risk Advisors.

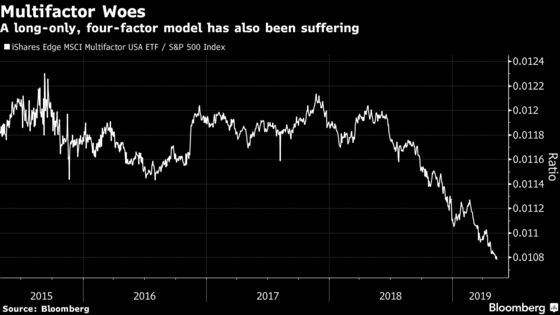

Heslop admits he’s “not unconcerned” about factor performance. His own large multi-factor fund -- the $10 billion Merian Global Equity Absolute Return Fund -- is down in 2019. But he reckons the pain is temporary.

“I’m not suggesting that there is some kind of new paradigm for factors themselves,” he said. “We are in a finite, and relatively short-term weak factor environment.”

--With assistance from John Gittelsohn.

To contact the reporter on this story: Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Samuel Potter, Chris Nagi

©2019 Bloomberg L.P.