AQR Quants Say Most Long-Vol Bets Lose Even If They're Right

AQR Quants Say Volatility Bets Can Lose Even If They're Right

(Bloomberg) -- Punting on an outbreak of volatility is a mug’s game, even at the best of times.

A new paper this month from two executives at AQR Capital Management delivers a sobering conclusion: Buying options to profit from a surge in equity-price swings is typically a losing proposition, even if volatility jumps.

Thank the persistently huge disparity between expected moves and what comes to pass.

And it’s the fuel for the enduring boom in the short-vol trade -- one that keeps regulators and investors on Wall Street awake at night.

“Tactical long volatility traders face a steep uphill battle,” Roni Israelov and Harsha Tummala at the quant giant write. “Some amount of healthy skepticism is likely warranted for those who claim to consistently have such exceptional skill.”

The long-vol investor is in effect virtually always buying when the trade is expensive and selling when it’s cheap, the authors conclude.

It’s human nature to bet good times can’t last, with speculators and hedgers keeping their faith. Net long positions in VIX exchange-traded products are at their highest in a year, according to JPMorgan Chase & Co.

Even as monetary policy makers unwind crisis-era measures while trade wars and political risks loom large, stock markets remain notably calm. The Cboe Volatility Index, or VIX, is hovering at around 13, compared with the 10-year average of about 20.

The so-called fear gauge spiked above 50 -- but only briefly -- during the February stock rout.

“Many proponents of long volatility exposure often advocate this trade in a low implied volatility market environment,” Israelov, who heads AQR’s vol-trading strategies, and Tummala write.

“Heightened levels of uncertainty, geopolitical risk, or merely a reversion to long-term volatility are some of the arguments put forth by those who expect volatility to spike.”

20 Percent

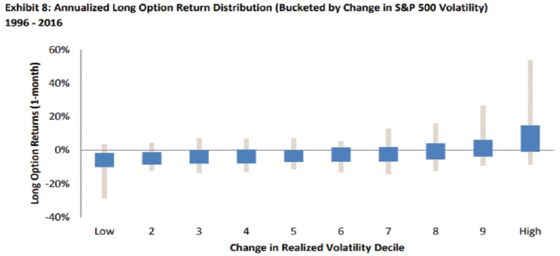

Using one-month equity index options, the authors demonstrate that such trades profit from an increase in vol only around 20 percent of the time. In other words, it can rise -- even substantially -- and the trades are still losers.

“You have to be exceptional at forecasting both the magnitude and the timing of large volatility increases, to simply not lose money on average,” they write. Volatility rises in the top decile are the only time that such a trade would be consistently profitable.

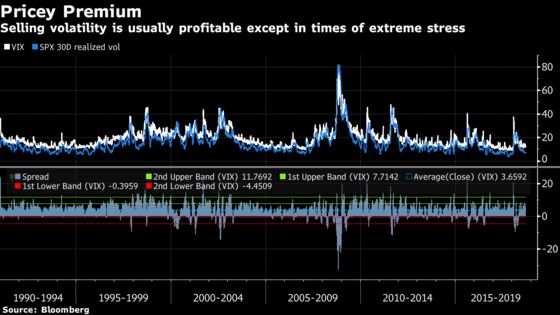

The headwind is the same force that powers the short-vol trade: the risk premium, or the difference between implied and realized equity moves.

In order to make money going long using options, traders must first overcome what can be a considerable difference between the price of vol baked into the option and the actualized level.

“The spread typically accrues to the volatility seller, paid by the long volatility investor,” the authors write.

‘Few Good Instruments’

The paper underscores how there remains no easy and foolproof way to place a direct bet that calm markets won’t last.

Derivatives on the VIX have their issues, while long bets on market swings via ETPs on the gauge are notorious cash incinerators. Variance swaps may be the preferred way for professionals to isolate bets on market swings.

Allegations that the VIX itself was being manipulated -- which the Cboe said were unfounded -- have also drawn the attention of regulators this year.

And it’s not just speculators who are often losers on long-volatility wagers, according to AQR researchers. Hedgers stand to suffer too by overpaying for protection, even when it’s considered cheap relative to historic levels, Israelov and AQR’s Lars Nielsen argued in a 2015 paper.

There are “too few good instruments” to position for choppy market conditions, Stephen Diggle, chief executive officer of family office Vulpes Investment Management, told Bloomberg News last week.

--With assistance from Luke Kawa.

To contact the reporter on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2018 Bloomberg L.P.