Another Euro Crisis? Here's What Markets Are Saying About Italy

Another Euro Crisis? Here's What Markets Are Saying About Italy

(Bloomberg) -- Italy’s stocks and bonds came under intense pressure on Friday, with the plunge in the country’s banks wiping $10 billion off their market value. Those who remember the chaos of the euro region’s sovereign debt crisis will be asking, whether this is the start of something much worse. Here’s what financial markets are telling us.

Bond Risks

The selloff in the nation’s 10-year bonds drove yields up the most since May -- a time when the Five Star Movement and the League parties were forming their coalition, and holding talks with euroskeptics who had floated the idea of leaving the euro area. The good news is that the hard-line rhetoric has faded somewhat, meaning the concern in markets is about the size of Italy’s debt load, rather than the risk that it leaves the currency bloc.

This is reflected in Italy’s 10-year yield spread over German bunds. That gauge is hovering at around 270 basis points, still short of the year’s highs of around 323 basis points. And this week’s selloff has been relatively orderly in comparison with the sudden, illiquid lurches that were seen in May.

Much could depend on how the credit-rating companies respond to the 2.4 percent deficit projection. Both S&P Global Investors and Moody’s Investors Service are due to review Italy over the course of the next month, and both have the nation just two notches above a junk rating. Foreign investors could flee if Italy loses its investment-grade status, according to Goldman Sachs Group Inc.

The budget deficit unveiled by Italy’s government isn’t disastrous for the country’s public finances, according to Bloomberg Economist David Powell. With a shortfall of 2.4 percent, the nation’s ratio of debt-to-gross domestic product should stay under control, he estimates. However, the European Commission would like Italy to pay off the debt at a faster pace.

Taking Stock

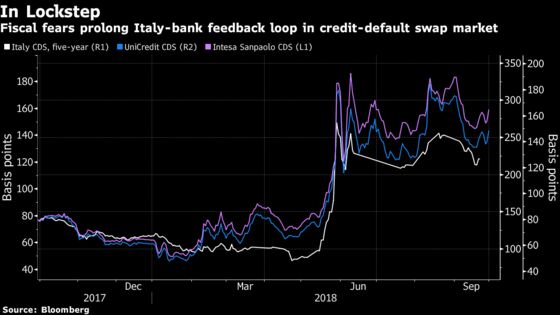

Italy’s banks took a battering Friday, with trading in some the biggest names -- UniCredit SpA, Intesa Sanpaolo SpA, Banco BPM SpA -- being halted at least once during the course of the day. The FTSE Italia All-Share Banks Index fell as much as 8.6 percent, the most in over two years, and representing a market wipeout of around 9 billion euros.

The problem for Italy’s banks stems from the fact that they are the biggest buyers of the country’s bonds, also known as BTPs. When those securities drop as rapidly as they did Friday, it hurts the banks that own them -- a phenomenon known as the sovereign-bank “doom loop.” That brings back memories of the euro-area debt crisis.

While the country’s financial institutions hold by far the most state obligations among lenders in Europe, one factor in banks’ favor is that their balance sheets are much improved since 2011. In addition, so long as the nation retains an investment-grade credit rating, banks are able to access liquidity from the European Central Bank if funding becomes scarce.

No Cold, Yet

The euro fell as the bond market reaction rippled through into the region’s banking sector, but declines were also distorted by an appreciating dollar. Prospects for the currency still look bright as the ECB moves closer to its first deposit-rate increase since 2011, at a time when the euro area is posting a current-account surplus.

Meanwhile, evidence of contagion to other markets was limited. The bonds of peripheral countries such as Spain and Portugal barely budged -- a far cry from the days of the debt crisis, when turmoil that started in Greece eventually forced other nations including Ireland and Portugal to seek bailouts, and toppled Italy’s government.

“It’s going to hang over markets for a while, but it’s not disastrous,” said Kit Juckes, global strategist at Societe Generale SA, who expects the euro to stay within a tight range. “We won’t get proper clarity for a while, and this is really only the start of the fiscal debate. Though we can say with some confidence that apart from the deficit-GDP ratio being below 3 percent, the EU’s fiscal rules will be broken.”

--With assistance from Samuel Potter and Blaise Robinson.

To contact the reporter on this story: John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Paul Dobson

©2018 Bloomberg L.P.