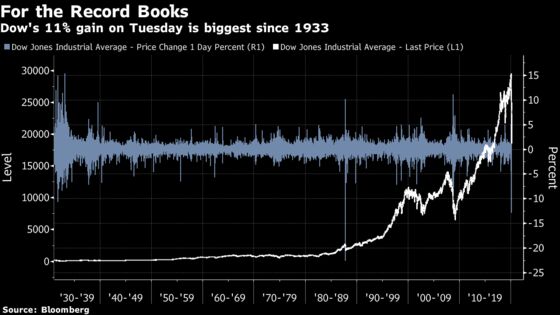

Another 11% Swing in the Dow Average Shows Value Still a Mystery

Volatility is just too high: the Dow has swung an average of 7% a day since March 12

(Bloomberg) -- As Wall Street celebrates the Dow Jones Industrial Average’s biggest surge in nine decades, spare a thought for the people paid to figure out value in the stock market.

A lot of them are just giving up, sick of trying to make sense of a market whose view of a company like Boeing Co. changes by tens of billions of dollars a day. Volatility is just too high: the Dow has swung an average of 7% a day since March 12 -- that’s well over $1 trillion of market value gained or lost in each session -- compared with 0.6% in 2019.

Throw in circuit breakers that limit moves in futures for hours, the slow drip of economic data that doesn’t yet reflect the coronavirus’s impact and companies that pull profit forecasts by the day -- it’s a landscape that defies any kind of valuation logic.

“The market has been flying blind, lacking two of its typical reference points, which are historical precedent and data,” says Dan Suzuki, Richard Bernstein Advisors deputy chief investment officer. “The data that the market typically relies on is too slow to keep up with how rapidly the situation has been changing.”

Financial models are going dark as virus angst roils prices, shuts businesses and upends supply chains. It’s impossible to assess how the Federal Reserve’s unprecedented stimulus will affect U.S. corporates, or when. That process takes time. During the financial crisis, four months and a 40% S&P 500 rout were needed before a 2008 package of fiscal stimulus kicked in for stocks. Nobody knows if the playbook will repeat.

Normally, when things go crazy in stocks, clients of big investment banks have strategists to turn to for advice on what to do. At the moment, the strategists have no clue.

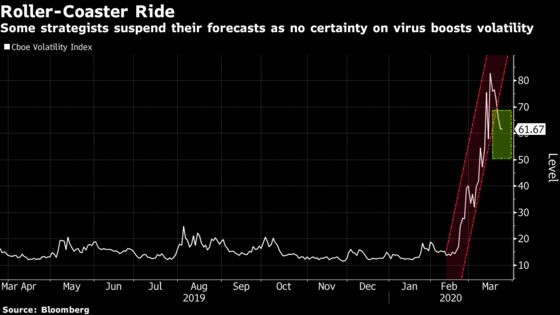

BMO Capital’s Brian Belski and Oppenheimer’s John Stoltzfus suspended their year-end S&P targets on Tuesday, saying they need more economic certainty and specific data on the virus’s hit on earnings to make recommendations. Canaccord Genuity’s Tony Dwyer did the same last week.

“For the first time in our collective careers, we have decided to suspend our year-end S&P 500 price and EPS targets,” BMO’s Belski and Nicholas Roccanova said in a note late Monday. “There is minimal rational method for predicting the path of U.S. stocks given the rapidity and volatility of data, forecasts, and emotions on a nearly daily basis.”

Historical models do nothing to clarify what will happen to the market or corporate earnings. In 11 recessions since World War II, profits in the S&P 500 have fallen as little as 2%, while the median drop was 13%, Goldman Sachs says. If you’re of the extreme view that the current situation resembles 2008’s financial crisis, equities may have a lot further to fall.

Everything is contingent. How will the virus progress? What happens when you turn off an economy? Will problems in the credit market make a recovery impossible? Dubravko Lakos-Bujas, a strategist at JPMorgan Chase & Co., wrote last week that if policy makers fail to pass a comprehensive fiscal package promptly, selling will accelerate, taking out momentum stocks that have so far held up -- relatively speaking. Marking those down to December 2018 lows -- when they saw their last big beating -- implies the index drops to 1,940, 43% from the February record.

“I don’t think it’s worth trying to estimate this disaster,” said Chris Zaccarelli, chief investment officer at Independent Advisor Alliance.

©2020 Bloomberg L.P.