An MFS Investment Manager Is Fighting FOMO and Dumping Stocks

An MFS Investment Manager Is Fighting FOMO and Dumping Stocks

(Bloomberg) -- Wall Street is counting on FOMO, or fear of missing out, to power the next leg of this fierce stock rally. But some, like Rob Almeida, refuse to be drawn in.

The veteran strategist and portfolio manager at MFS Investment Management, a nearly century-old firm overseeing about $500 billion, is digging in his heels. With stocks volatile in the wake of their epic run, Almeida argues stretched corporate balance sheets and overly rosy economic projections make it too early to dive back in.

“The conditions going into this recession and this type of recession that we’re in are worse,” Almeida said in an interview. “I would expect the earnings degradation to be something worse than average, but the market has it something materially better.”

Almeida has slashed net equity exposure in the long-short fund he manages to 10%, its lowest ever. The market-neutral strategy has beaten 90% of its peers this year. In his income fund, he’s cutting stocks in favor of bonds. Elsewhere at MFS, his colleagues are selling cyclical equities, a sign of pessimism in the economic recovery.

Many of his peers are watching the market recovery “with an incredulous and frustrated look on their faces,” said the strategist.

Almeida’s skepticism lies at the heart of the debate on what it will take for institutional investors to unleash their trillions to buttress the rally anew.

Even with the recent swings, U.S. stocks have jumped 34% from their trough in defiance of the pandemic-induced crash. Weekly jobless claims remain in the seven-digit range and exceeded forecasts for a second straight week. Profits are collapsing and bankruptcies are piling up. Coronavirus cases are surging again in parts of America.

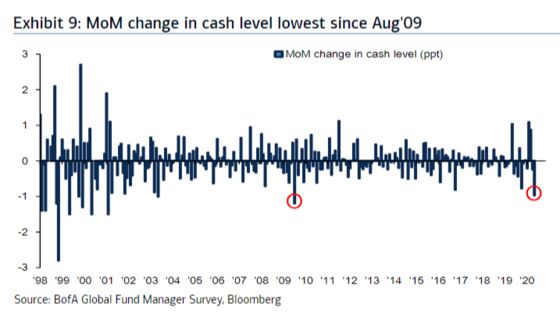

Some have found the FOMO irresistible. In a sign of capitulation, cash levels have dropped by the most since 2009, according to a Bank of America Corp. survey of fund managers in June. Hedge fund exposure is at the highest since 2018. Quants and other systematic players have started to chase U.S. shares higher, according to Deutsche Bank Group AG.

Still, a record majority of managers call equities overvalued, according to that same Bank of America survey. Only 30% of mutual funds beat their benchmarks this month, a sign their exposure remains defensive, according to Barclays Plc.

Unlike previous downturns, the problem is U.S. corporate balance sheets were worsening even before the crisis hit, and there’s a low chance consumers can power business profits anytime soon, according to Almeida.

“Balance sheet are weaker versus six months ago not stronger -- yet credit spreads are back to near pre-pandemic levels and the equity risk premium is materially lower,” he said.

The S&P 500’s net-debt-to-earnings ratio, excluding the financial sector, has been climbing over the past six years and now stands at the highest since at least 2003. Meanwhile, both equity and credit issuance have risen this year while share repurchases plunged -- a trend that should be unfavorable to stock buyers.

Even if a majority of customers return to businesses, it won’t be sufficient to bump corporate profits back to pre-Covid levels, Almeida said.

Last Customer

“It’s that last customer that drives all the operating leverage,” he said. “The remaining 10%, 20%, 30% of their customer base hasn’t returned and I don’t think they will until you see immunity.”

Of course, there’s always the bull’s ultimate rebuttal: Don’t fight the Fed. With bond yields near record low, stocks look more attractive. That’s helped push the S&P 500 to near the highest level versus the coming year’s earnings since 2000.

But as painful as the equity rebound has been for professional investors, Almeida doesn’t see much in the Fed argument.

“It works in the near term because money needs to find its home,” he said. “In the longer term, if the asset isn’t supported by cash flow, it isn’t going to work.”

©2020 Bloomberg L.P.