Hedge Funds Burned by Short Trade as America’s Malls Refuse to Die

America’s Malls Aren’t Dying as Fast as Some Traders Would Like

(Bloomberg) -- For traders betting on the death of America’s malls, being right and making money are proving to be two very different things.

Reminiscent of Michael Burry of “The Big Short” fame, these hedge funds have piled into a trade that could reap huge profits if loans taken out by beleaguered mall and shopping-center operators eventually go bust.

While the strategy has largely been a winning one, on paper at least, there’s still one catch: the actual cost to maintain the trade month after month keeps growing as the mall industry refuses to die.

And that’s squeezing short sellers as they play a costly waiting game.

“The longs and the shorts are very much in a kind of Mexican standoff and seeing who is going to blink first,” said Gareth Davies, the head of research for commercial mortgage-backed securities at JPMorgan Chase & Co. The issue isn’t about where retail is headed, but rather the timing, he said.

To paraphrase an adage attributed to famed economist John Maynard Keynes, the current stalemate is a reminder to the short sellers that markets can remain irrational longer than they can remain solvent.

According to JPMorgan, a hypothetical $25 million position would put a short seller on the hook for more than $60,000 in premiums each month. Based on those numbers, over the course of 18 months, the cost to hold on to the trade could top $1 million.

That hasn’t kept investors from piling in. This year alone, they’ve traded more than $15 billion on one series of CMBS.

“I think a lot of people bought the theory or the story of why they might want to short this index because of ‘The Big Short,’” said Janet Tavakoli, president of risk consulting firm Tavakoli Structured Finance. “But the execution of it is always more difficult.”

The Trade

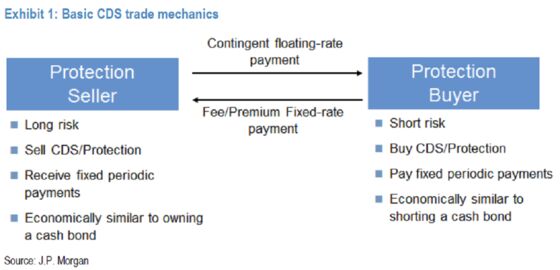

Investors have been betting on indexes that track baskets of commercial mortgages with outsize exposure to malls across the country. Through buying and selling credit default swaps, they’re effectively wagering on whether -- or when -- the underlying loans will go bust and which way the index will move.

But the malls and other real-estate in the indexes have mostly stayed on top of their loan payments. That’s been bad news for shorts, as they’re making hefty monthly premiums to maintain their positions. Those on the other side of the bet receive the premiums but are on the hook for losses if the loans go bad.

One of the main avenues for making the wager is on the BBB- basket of the Markit CMBX Series 6 index (the other is called Series 7). They’re popular for this trade because of their higher exposure to malls. Early last year, that sub-index fell sharply, losing more than 9 percent of its value in about a month and hitting a record low in November. That was good news for shorts at the time, but this year it’s gained and sits 8 percent above the all-time low.

Around the time the benchmark started to decline, Deutsche Bank AG analysts recommended the short. Ed Reardon, head of securitization research at the firm, recently doubled down on the recommendation even though its showing a loss.

“Our own thesis is you’re not paid enough in spread today to compensate for the risks you might have,” he said, referring to the long side of the trade. “We have stayed short.”

In an example laid out by JPMorgan, the short pays a premium each month in exchange for a payout if there is a so-called “credit event” involving the underlying loans, like missed payments. Some investors hedge their short trades by going long on another part of the index, offsetting a bit of the risk, according to Reardon.

But investors betting against the mall loans don’t have to wait for them to go bad to turn a profit. When the trades are executed, an upfront payment is made based on the level of the index. At any time, investors can try to unwind the trade with a market maker and cash in.

Hedge fund Alder Hill Management went public with its short bet last year, one of a handful to do so. On the long side, money management giant Putnam Investments has disclosed a large stake in the trade, the Wall Street Journal reported.

But shorting malls isn’t as straightforward as betting against subprime residential mortgages ahead of the financial crisis. Just 36 percent of the loans tracked by one index used to short malls are backed by retail, according JPMorgan’s note. The proportion of those loans specifically backed by malls is even smaller.

“We talk about the tail,” Davies said. “We don’t talk about the dog.”

Still, if mall loans go sour, it could trigger huge payouts to the shorts. Unfortunately, the majority of defaults in commercial mortgage-backed securities happen when the loans are refinanced, which for many mall loans tracked by CMBX Series 6 isn’t until 2022, Davies said.

The nature of malls is that they’re often able to hang on for a long time, even if tenants are struggling, according Nitin Bhasin, a senior managing director in the CMBS group at Kroll Bond Rating Agency Inc.

“These are large, living, breathing entities,” he said.

--With assistance from Adam Tempkin.

To contact the reporter on this story: Jeremy Hill in New York at jhill273@bloomberg.net

To contact the editors responsible for this story: Christopher DeReza at cdereza1@bloomberg.net, ;Jeremy Herron at jherron8@bloomberg.net, Randall Jensen, Michael Tsang

©2018 Bloomberg L.P.