Empty Hotels Might Just Be Next Big Short for Hedge Funds

Empty Hotels Might Just Be Next Big Short for Hedge Funds

(Bloomberg) -- Hedge funds and other short sellers are beginning to set their sights on a U.S. credit-derivatives index with outsized exposure to hotel debt as the pandemic sinks the hospitality industry into distress.

The firms are starting to build up wagers against the synthetic index, known as CMBX 9, shifting attention from a high-profile bet against America’s challenged malls. The shift, which market participants say is beginning to show up in some trading flows, comes as delinquencies on hospitality property loans surge and even begin to exceed those in retail.

“In the last month there has been more selling pressure on the CMBX 9 than any of the other CMBS indices,” said Dan McNamara, a principal at MP Securitized Credit Partners, a hedge fund focused on shorting commercial mortgage bonds. “That’s because some hedge funds are actively looking to play the short side on the Series 9 index due to its significant hotel exposure.”

Retail debt has been a lucrative bearish bet this year as people stayed home amid lockdowns and shopped online, exacerbating an existing threat to brick-and-mortar stores. Traders have been taking positions on retail through a 2012 version of the commercial mortgage index called CMBX 6, which has a high concentration of debt tied to shopping malls.

“Funds have been coming out of the CMBX 6 and moving onto the CMBX 9,” said Christopher Sullivan, chief investment officer of United Nations Federal Credit Union. “The CMBX 6 trade has gone a bit long in the tooth and is now more fairly priced given the likely pandemic effects. We can see this series becoming the favorite option now.”

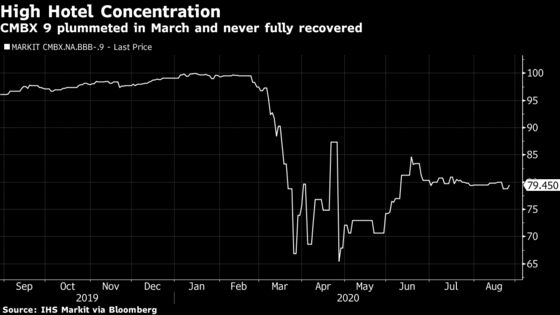

Hotel loans make up about 17% of the commercial mortgage debt underlying the CMBX 9 index, which is tied to 25 commercial mortgage securities created in 2015. The debt includes a now-defaulted $200 million loan backed by 50 extended-stay hotels owned by Starwood Capital Group. The loan was relatively stable at the end of 2019, according to Fitch Ratings, but defaulted at maturity in July because of lost business during pandemic-induced shutdowns.

Hotel Pain

Nearly 25% of hotel loans in CMBS are now delinquent, Cantor Fitzgerald LP researchers said in a Wednesday note, compared to about 20% for anchored retail loans. Across the broader CMBS universe, about 10% of hotel loans securitized in bonds are now more than 90 days overdue, compared to only 3.7% for retail loans, according to Darrell Wheeler, head of research at the New York-based firm.

The BBB- tranche of the CMBX 9 series fell to 65.5 cents on the dollar by late April from almost par in early March. It’s since gradually fallen in price to 79 cents on the dollar Thursday from its mid-June peak of about 85 cents.

UNFCU’s Sullivan said CMBX 9 trading volume has been increasing for well over a month, and was among the most actively traded across CMBS indexes for several days in July and August, according to aggregated swap depository data compiled by Bloomberg. Total cumulative trading volume for all tranches of the CMBX 9 increased to $258.5 million on Aug. 26 from $30.2 million on July 28, the data show.

For the week ending Aug. 21, the BB tranche of CMBX 9 had $95 million of CDS contracts trading in the market, the highest of any series’ BB tier, according to JPMorgan Chase & Co. data. CMBX 6 had the next greatest amount trading, at $35 million.

Retail Short

MP Securitized Credit’s short bet on retail through the CMBX 6 fueled a 75.4% gain in one of its flagship vehicles for the year through July, according to an investor letter seen by Bloomberg. That bearish wager references a basket of 25 CMBS with significant mall exposure.

It’s also produced a $1.3 billion windfall for Carl Icahn, who increased his position after the pandemic shutdowns escalated the already poor performance of mall debt.

So far MP Securitized Credit remains focused on shorting the retail space. The hotel industry has a better chance for a broader recovery than retail, which was already up against secular challenges such as growth in online sales, McNamara said.

Risky Trade

Among the biggest risks in shorting CMBS is mis-timing the wager. That’s what happened to some of the earliest proponents of the CMBX 6 short trade. Hedge fund Alder Hill Management, which had been short the CMBX 6 since at least early 2017, shuttered last year as losses on the wager piled up.

One downside of the CMBX 9 trade is that it doesn’t mature until 2025, while CMBX 6 shorts can get their payouts in 2022. And for short sellers, “CMBX 9 is not as clear cut as CMBX 6, where we expected several BBB- bond classes to take full losses,” Cantor’s Wheeler said.

It’s not clear whether there will be enough two-way volume in the CMBX 9 index to sustain large bets, said Matt Weinstein, a partner at Axonic Capital, a hedge fund specializing in structured products and commercial real estate. But the thesis makes sense, he said. With one in four hotels in CMBS already in default and revenue per available room still down nearly 50% year-over-year, defaults are likely to pile up as forbearance agreements with lenders roll off.

“From a thematic viewpoint, it makes sense to short hotels,” he said.

©2020 Bloomberg L.P.