Meltdown of America-First Strategy Puts Small-Caps on a Tough Turnaround Path

Meltdown of America-First Strategy Puts Small-Caps on a Tough Turnaround Path

(Bloomberg) -- The rise and fall of small-cap U.S. stocks was one of the most jarring market reversals this year. And 2019 is expected to only bring a modest recovery thanks to pressure from higher interest rates and concerns about peaking earnings growth.

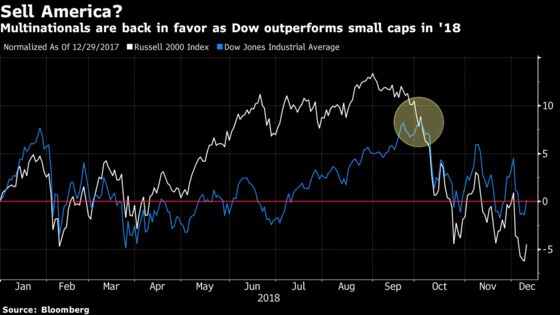

Investing in smaller, domestically focused companies had been among most popular strategies in 2018, as tariff tensions and a fiscal stimulus boost made them into safe havens. But the so-called America First trade has completely unwound. The Russell 2000 Index has plunged 16 percent from an August record and is on track for the first annual decline since 2015.

Wall Street strategists are warning investors to brace for more turbulence. From the U.S.-China trade war to rising interest rates and cuts in profit estimates, there’s no shortage of headwinds for small firms, they say. Despite trading at the biggest discount to their large-cap counterparts in years, the risk-reward of small caps is unattractive at this late stage of the business cycle, Barclays analyst Venu Krishna cautioned in a note this week, forecasting the Russell 2000 to rise to 1,560 by the end of 2019, a 6.4 percent increase from current levels.

Jefferies is projecting the index to finish next year at 1,550, implying a 5.7 percent gain. Both estimates are below the gauge’s average 9.2 percent annual return over the past 10 years.

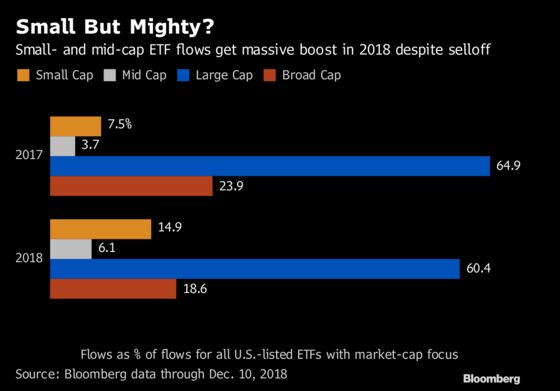

Flows into exchange-traded funds paint a more optimistic picture. Buyers continued to pile into ETFs tracking small-cap companies through the sector’s slide in September, allocating more than $25 billion for the year, topping the group’s 2017 flows.

For most of the year, domestic firms’ perceived insulation from global turmoil drove investor bullishness, so trade concerns have probably played a role in funds flows, according to Todd Rosenbluth, director of ETF research at CFRA Research.

Even riskier funds offering leveraged exposure to small caps have attracted a lot of interest, especially during October’s market volatility. The $809 million Direxion Daily Small Cap Bull 3X Shares fund, which gives investors three-times the daily performance of an index of small caps, took in more than $381 million in October, the most for any month going back to August 2011.

Direxion Investments managing director Sylvia Jablonski has seen quick and consistent inflows to funds that that have been falling the most, with investors betting on a near-term rebound.

Here’s what strategists are saying about the sector’s outlook:

Barclays, Deputy Head of U.S. Equity Research Venu Krishna

Krishna expects small caps to continue to underperform their larger peers amid slower domestic economic growth next year, which “could take the wind out of the sails for top-line growth” at small firms. While Barclays is not forecasting a recession next year, analysts expect “risk aversion to firmly be in place,” which will hurt small-cap stocks.

Despite perceptions that domestic firms are more insulated from the trade dispute with China, small companies actually have higher exports and imports relative to their sales, as well as lower margins and less pricing power to pass along higher tariffs to customers, Krishna points out. Barclays estimates tariffs to cut small-cap Ebitda growth by around 2.5 percent over the next year.

BofAML, Equity and Quantitative Strategist Savita Subramanian

Bank of America continues to prefer large caps over small caps in 2019. Small, domestically focused firms have posted “weaker trends than large caps the past few earnings seasons, management is guiding more below than above consensus on earnings, and small caps have seen more earnings estimate cuts than raises by analysts.”

Leverage near record levels is also a “key risk.” More than half of small firms’ debt has floating interest rates, leaving them more exposed to rising rates and widening credit spreads.

Analysts forecast volatility, measured by the VIX, to double over the next three years, which doesn’t bode well for small caps. Investors should stick to large caps. “What works when volatility rises? Quality of earnings,” analysts led by Subramanian wrote in a Nov. 20 note.

Jefferies, Equity Strategist Steven DeSanctis

DeSanctis says small- and mid-cap investors should get used to bigger swings after this year’s roller coaster ride. “We want to be domestic,” as global growth is not showing signs of improving, DeSanctis wrote in a note earlier this week.

Concerns about an inverted yield curve are “overblown,” and “if it’s one hike, three hikes, doesn’t matter. Fed raises equals OK performance” for small caps in 2019. The strategist also forecasts that 12 percent earnings growth for small firms is achievable, despite reduced estimates due to a stronger dollar. Merger momentum should remain strong as valuations have come down and larger companies are looking to grow.

To weather volatility, investors should stick to quality stocks, which are “very cheap,” DeSanctis points out. Jefferies’s new sector allocation leans toward growth over value, and the firm is now more bullish on beaten-down tech stocks, while bearish on communication services. Financials were cut to market weight from overweight as earnings growth estimates for 2019 need to come down.

Morgan Stanley, Chief U.S. Equity Strategist Mike Wilson

The bank is still underweight small caps -- for now. Morgan Stanley’s view is that the global economy will bottom out in the first quarter while the U.S. will trough in the third quarter, “which means domestically-oriented companies probably underperform,” Wilson said in an interview on Bloomberg TV Wednesday.

But some time early next year, maybe during the second quarter, small caps “become probably pretty attractive again,” Wilson said. He notes that the Federal Reserve is probably going to “lean more dovish” when it raises rates next week. “That means maybe they are not going to do as many rate hikes next year.”

--With assistance from Lu Wang.

To contact the reporters on this story: Tatiana Darie in New York at tdarie1@bloomberg.net;Carolina Wilson in New York City at cwilson166@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Richard Richtmyer, Eric J. Weiner

©2018 Bloomberg L.P.