All of a Sudden, the New Year Market Rally Is Under Threat

All of a Sudden, the New Year Market Rally Looks Under Threat

(Bloomberg) -- February is shaping up to be a lot less friendly than January, as the cheer that drove last month’s global equity rally -- the biggest in more than seven years -- dissipates under a cloud of negative developments.

The most obvious trigger for the slide in stocks Thursday and Friday was newfound doubts on prospects for the U.S. and China to avoid an escalation in tariffs on March 1, just three weeks away. President Donald Trump’s comment that he’s not likely to meet with President Xi Jinping calls into question the conventional wisdom that a deal was in sight, or at least that talks would keep going without further damage to trade flows.

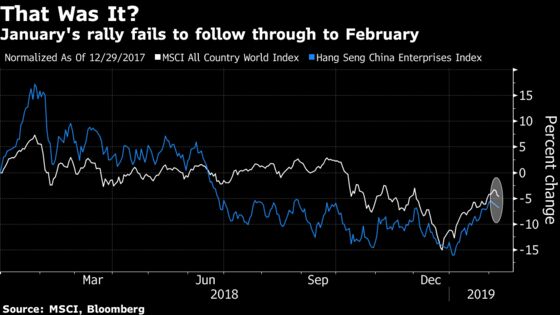

But a panoply of other concerns are also starting to take hold, leaving investors with little appetite to double down on bets made in January, from rallies in developed-world equities to an appreciation in China’s yuan. The tumble of as much as 2.2 percent in the Hang Seng China Enterprises Index Friday boded ill for the domestic Chinese market’s Monday reopening after a week off, though the gauge pared losses later in the day. The broader MSCI Asia Pacific Index saw the biggest loss in a month.

“Share markets have had a great rebound from oversold conditions in December and are now up against technical resistance and getting overbought,” Shane Oliver, head of investment strategy at AMP Capital Investors Ltd., said by email Friday. “Meanwhile a bunch of balls remain up in the air regarding the trade war, the U.S. shutdown and slowing global growth. So there is a high risk of a pull back from here.”

The following are some of the worries for investors to consider:

Growth Outlook

The U.S. jobs and manufacturing PMI reports came in strong on Feb. 1, but there’s a lot of other evidence that the global slowdown has yet to find a trough. The Reserve Bank of Australia on Friday slashed its forecast for the year through June by 0.75 percentage point, to 2.5 percent. Keep in mind Australia has close ties to the Chinese economy, thanks to iron and coal exports.

European concerns are deepening, and it’s not just the Italian recession or German manufacturing drop that’s at issue. The European Union’s executive authority now sees “substantial” risks. The commission cut forecasts for all major euro region economies Thursday. Even before Trump’s comment on the unlikelihood of Xi meeting this month, the Stoxx Europe 600 fell into the red Thursday, and kept dropping Friday. Futures on the S&P 500 Index signalled a third day of declines.

There’s also just a week left for the U.S. to pass a spending bill to avert another government shutdown.

Bond Market

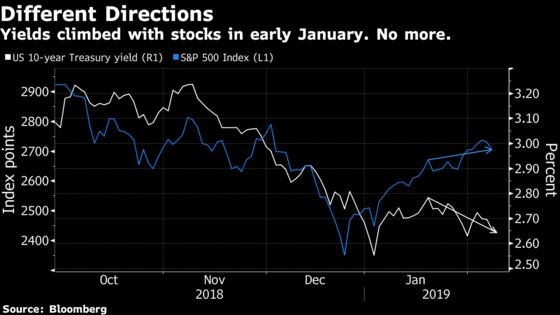

When the risk rally began in early January, Treasury yields climbed along with stocks. But that’s changed. True, cheaper borrowing costs should be helpful to the growth outlook and theoretically mean a lower discount rate to apply to corporate earnings streams. But falling yields could also suggest that bond investors are seeing greater dangers than equity investors have in recent weeks.

Not only have Treasury yields come down, but the universe of negative-yielding debt has expanded again. Japan’s 10-year government bond yields fell to as low as minus 0.035 percent Friday. Elsewhere, Australian 10-year yields have tumbled about 10 basis points this week thanks to the central bank’s official shift to a neutral stance. New Zealand’s 10-year bond yields hit their lowest level on record, a day after a weak employment report.

One proviso on the fixed-income front: inflows into U.S. high-yield credit have jumped.

For more on the outlook: |

|

Earnings Disappointment

This season is a whole lot less robust than past quarters when it comes to corporate results. With 73 percent of the U.S. S&P 500 Index members having reported, Bank of America Merrill Lynch analysts estimate that the proportion of “beats” relative to expectations is the weakest in four years. And that’s after analysts had “trimmed expectations more than usual heading into the quarter,” the bank’s Jill Carey Hall and Savita Subramanian wrote Wednesday.

Buybacks have helped in some instances, including announcements from Softbank and Sony this week, but don’t appear to be enough. Certainly not enough to stop Japan’s Topix Index from heading toward a near 2 percent slide on Friday, the worst since the December carnage.

Valuation

Cheaper valuations after the historic slide in equities at the end of 2018 were one big reason to dive in at the start of 2019. But to some analysts they’re now looking less compelling, after the MSCI ACWI Index of world stocks posted the best month since 2011 in January.

“The New Year recovery in risky assets has been impressive, to say the least,” George Davis, chief technical strategist at RBC Capital Markets, wrote in a note Thursday. “However, in our recent discussions with clients, we have been highlighting what we feel is the increasing probability of a correction.”

Davis cited valuation metrics including the Canadian dollar as a proxy bet for risk. It was poised for a bullish trend reversal Thursday, he wrote.

Trade

Last but not least, next week brings the U.S. delegation’s trip to Beijing to continue the trade negotiations. White House economic adviser Larry Kudlow’s said Thursday that a “sizable distance" remained, though he had a “good vibe” about ongoing talks. With little clarity on the endgame, investors will need to keep close watch on developments as they assess just how long the 2019 rally can continue.

--With assistance from Cormac Mullen.

To contact the reporters on this story: Christopher Anstey in Tokyo at canstey@bloomberg.net;Abhishek Vishnoi in Singapore at avishnoi4@bloomberg.net

To contact the editors responsible for this story: Divya Balji at dbalji1@bloomberg.net, Ravil Shirodkar

©2019 Bloomberg L.P.