All Eyes on Saudis as Oil Bulls Cut Bets to Lowest Since 2016

All Eyes on Saudis as Oil Bulls Cut Bets to Lowest Since 2016

(Bloomberg) -- Hedge funds aren’t buying into OPEC’s oil-production cuts just yet.

They slashed net wagers on a rally of West Texas Intermediate crude to the lowest in more than two years, while short-selling of Brent oil climbed for a record 11th week. Both benchmarks ended the week lower as the cartel’s efforts were overshadowed by concern about booming shale production and waning global demand. It’s mostly up to Saudi Arabia now to try to win investors over.

“Demand is now decreasing and you have a problem with Chinese growth,” said Tariq Zahir, a commodity fund manager at Tyche Capital Advisors LLC. “Right now, everything is dependent on what Saudi Arabia does.”

Saudi Arabia clearly knows that. The oil-rich kingdom has plans to slash exports to the U.S. in coming weeks in an effort to dampen visible build-ups in crude supplies, telling local refiners to expect much lower shipments in January, according to people briefed on the plans. That could bolster confidence among traders that OPEC’s de facto leader is serious about rebalancing supply and demand.

“We should be at just about the end of the cycle where longs have gotten wiped out,” said John Kilduff, a partner at New York-hedge fund Again Capital LLC “In the medium term, the Saudis exporting less to the U.S. should help us head higher.”

The biggest challenge for the Saudis is the concern that growth in prolific U.S. fields could surpass supply curbs by OPEC and its allies. North Dakota’s Bakken shale play produced a record 1.4 million barrels a day in October, while the Permian Basin of West Texas and New Mexico is forecast to surpass 4 million next month.

On Friday, traders continued to sell off oil, as Brent futures for February delivery fell 1.9 percent to settle at $60.28 a barrel in London, putting it down 2.3 percent on the week. WTI for January closed down 2.6 percent on the day, closing out the week down 2.7 percent.

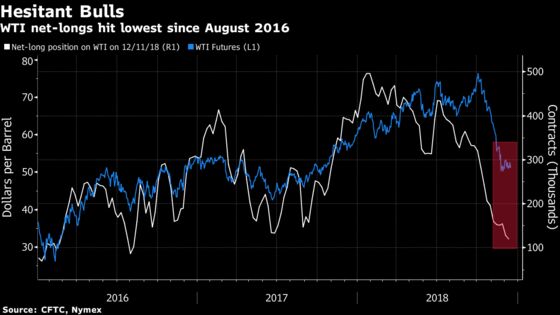

Hedge funds’ net-long position on WTI -- the difference between bets on higher prices and wagers on a drop -- slid 6.7 percent to 119,675 in the week ended Dec 11, the U.S. Commodity Futures Trading Commission said Friday. That was the least bullish since August 2016. Longs-only fell 0.8 percent to the lowest since March 2013, while shorts rose 7.8 percent.

Brent net-longs edged up from a three-year low over the same period, rising by 2.3 percent to 139,597 contracts, ICE Futures Europe data showed. Longs rose 3.1 percent, while shorts rose 3.9 percent to the highest since July 2017.

“Market observers may need to wait for the cuts to percolate to inventory data,” Barclays analysts including Michael Cohen said in a note, adding that Brent and WTI prices are poised to rebound in the first half of next year.

| Other Positions: |

|

To contact the reporter on this story: Catherine Ngai in New York at cngai16@bloomberg.net

To contact the editors responsible for this story: David Marino at dmarino4@bloomberg.net, Carlos Caminada, Dan Reichl

©2018 Bloomberg L.P.