After Taming Yields, RBI May Take Another Leaf From ECB

RBI may tie future LTROs to actual credit growth, IDFC AMC says.

(Bloomberg) -- Terms of Trade is a daily newsletter that untangles a world threatened by trade wars. Sign up here.

India’s central bank may follow up on its generous funding offer to banks with another unconventional measure as it seeks to boost lending to the real economy.

The authority may unveil another European Central Bank-styled facility called Targeted Longer-Term Refinancing Operations to expand credit to businesses and households, after concluding an ongoing program to lend $14 billion at the policy rate, according to Standard Chartered Plc and Nomura Holdings Inc.

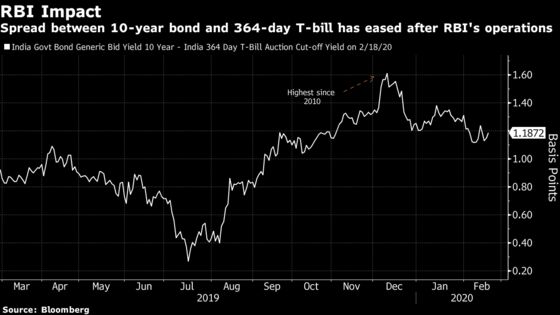

The Reserve Bank of India has tapped the toolkit of its peers to pull down corporate borrowing costs after five rate cuts in 2019 failed to spur credit demand. A mix of a Federal Reserve-style ‘Operation Twist’ and the ECB-like cash boost to banks has led to term spreads -- the gap between 10-year debt and 364-day Treasury bill yields -- shrinking from a decade-high in December.

“The RBI may now choose to tweak these programs to make them more targeted as market rates have fallen to a reasonable level, wherein incremental fall will not meaningfully incentivize incremental credit off-take,” said Suyash Choudhary, head of fixed income at IDFC Asset Management Co.

RBI Governor Shaktikanta Das told reporters earlier this month that the central bank has more tools than the regular repurchase rate at its disposal. That meant he would take more steps to ensure that policy transmission is effective.

Yields on benchmark 10-year and four-year debt have declined by more than 40 basis points since the mid-December announcement of Operation Twist -- buying long-dated bonds and selling the shorter tenor ones -- and LTROs in early February. Borrowing costs for companies have also fallen, with the yields on 10-year AAA-rated bonds down about 40 basis points.

“RBI’s OT/LTRO operations have succeeded in bringing down yields and they should be comfortable at these levels,” said Teresa John, an economist at Nirmal Bang Equities Pvt. in Mumbai. With yields below now 6.5% “we don’t expect any concerted effort to bring them down further,” she said.

The yield on 10-year bonds rose 4 basis points to 6.38% at 4:20 p.m. in Mumbai.

The ECB began the so-called TLTRO in 2014, with the aim to push banks to lend more to businesses and households. Initially, they were loans with longer-than-normal maturities tied to lending targets, but the terms became increasingly generous in subsequent iterations.

A key feature since 2016 has been that banks can get cash back if they comply with lending goals, as the loans are remunerated at a rate as low as the ECB’s negative deposit rate. TLTROs were revived in a third round last September, and have inspired a number of central banks around the world, including the People’s Bank of China.

--With assistance from Carolynn Look.

To contact the reporter on this story: Kartik Goyal in Mumbai at kgoyal@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Ravil Shirodkar, Karthikeyan Sundaram

©2020 Bloomberg L.P.