After Quant Bust 2020 Comes a Reckoning for Stock Math Wizzes

After Quant Bust 2020 Comes a Reckoning for Stock Math Wizze

(Bloomberg) -- As this year’s market storm recedes, the forced stock selling among Wall Street’s quant investors is finally ending.

Now the reckoning can begin.

These systematic players, who use rules-based strategies to determine what and when to trade, were already suffering through what some called a “Quant Winter” when the mayhem hit. In fact, the turmoil was a chance to show the strength of their math-powered methods, which aim to outperform in a sell-off.

It didn’t work out that way. Instead, the coronavirus fallout has exposed more clearly than ever the existential crisis the systematic cohort faces.

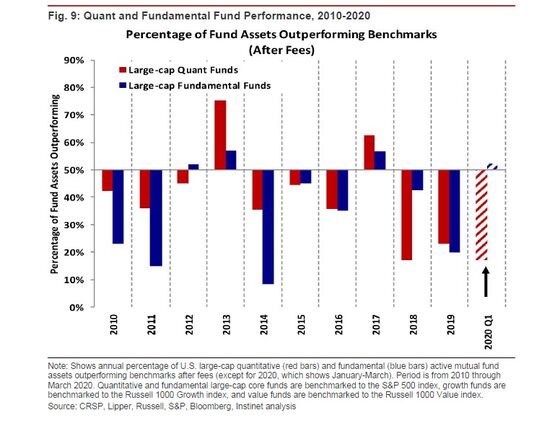

Large-cap quant mutual funds underperformed their discretionary peers. So-called market-neutral bets -- designed to beat benchmarks in a drawdown -- misfired. Even alternative risk premia, which are touted specifically for being uncorrelated, failed to live up to the hype.

“Our biggest disappointment was after quant managers struggled for several years they were hit severely in the market turmoil,” said Gerben de Zwart, managing director for quantitative strategies at APG Asset Management, which oversees 565 billion euros ($620 billion) of pension assets overall in the Netherlands. “That was another challenge on top of several other challenges.”

The good news is that working out why is easier than usual for this opaque part of the investment world.

As price swings and asset correlations reached records in the crisis, quant funds invested in hundreds of securities were forced to delever en masse -- igniting a vicious cycle in which selling spurred more volatility.

But knowing whether something is structurally broken -- and if it is, how to fix it -- is harder than ever on the heels of a once-in-century pathogen.

In one view, the unprecedented events have exposed the folly of using traditional rules-based methods built around decades of historical behavior. That means urgent fixes are now needed, like letting humans override models, or using alternative data to overhaul strategies that dissect securities by traits like their apparent cheapness, known as factor investing.

On the other hand, what if tried-and-tested rules grounded in science are best-placed to exploit the historic premiums on offer after the market carnage?

This debate is playing out among proponents of a quant approach called statistical arbitrage, which seeks to exploit unhinged relationships -- like when shares of PepsiCo Inc. and The Coca-Cola Co. trade in opposite directions for no good reason -- while staying neutral on market direction overall.

The style cratered as liquidations by long-only funds upended the trading patterns these models typically profit from, while the liquidity crisis made it harder to build short bets. This inadvertently meant quants were more exposed to their losing longs.

In such an environment, “these kind of strategies are designed to lose money,” Zura Kakushadze, chief executive officer of Quantigic Solutions, wrote in a paper titled “Quant Bust 2020.” “During extreme market routs there is no snap-back.”

Robot Reckoning

Some contend the quant industry needs a wholesale revamp after a decade of bull-market underperformance. The failure of equity market-neutral trades in the bear market that finally arrived this year only underscores the point.

Marcos Lopez de Prado is seizing the opportunity to pitch his machine-learning solutions. The former quant at AQR Capital Management and Guggenheim Partners says the systematic cohort should unleash artificial intelligence to mine alternative data in order to help strategies ride fast-moving markets and discover new sources of returns.

The decades of numbers you use to predict future returns can’t tell you who’s buying what during the pandemic. Satellite imagery and email receipts just might.

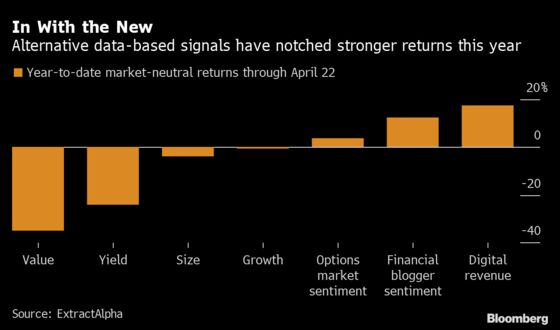

This oft-cited AI remedy may have gained more converts in the pandemic, especially after the failure of a few traditional factors. Value and size, for instance, have only extended their long-standing underperformance.

Meanwhile, signals based on alternative inputs like digital sales or blogger sentiment fared better, according to research firm ExtractAlpha.

All this boosts the case for giving portfolios a discretionary tilt, known as a “quantamental” approach. Joseph Mezrich, a quantitative strategist at Nomura Instinet, suggests that fundamental investors have beaten quants in the crisis because they adapted more quickly to the new reality, judging by how much more the former deviated from their benchmarks.

As economies shut down around the globe, human traders rapidly adjusted their portfolios, while the computer models -- trained on decades of data -- were slower.

The speed of reaction could be key. At HSBC Global Asset Management, deteriorating short-term indicators prompted the Multi-Asset Style Factors fund to cut its risk target by 30% by early March, helping the strategy cling to a 2% gain this year, says Mathieu Guillemet, head of multi-asset specialist strategies.

At Dutch pension manager APG, de Zwart says a system that lets humans override models has helped it respond more quickly.

“It really makes our portfolio managers market-aware and not only hide between models and say the models are deciding this or buying this position,” he said.

It’s all profoundly controversial for an industry built on rules drawn from analysis of decades of behavior. So while reformists shift long-standing allocation practices, many purists are in fighting spirits.

They see ample scope to outperform in the crisis aftermath -- underscoring the manifold divisions in the systematic corner of high-octane finance.

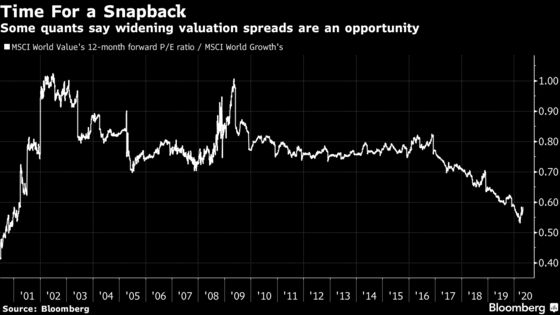

“Those valuation differences between cheap and expensive stocks are massive dislocations,” said Gavin Smith, a portfolio manager at QMA. “Deep-value opportunities are evident in all segments of the market.”

©2020 Bloomberg L.P.