After Crushing the London Whale, a Hedge-Fund Star Lost His Way

Feldstein’s comedown in part reflects struggles plaguing the hedge fund industry, which has been littered with firm closures.

(Bloomberg) --

In the aftermath of the financial crisis, hedge-fund titan Andrew Feldstein was hailed on Wall Street as one of the big winners.

His BlueMountain Capital Management fund made $300 million in 2012 betting against a former employer, JPMorgan Chase & Co., which was embroiled in the infamous London Whale credit securities scandal. In a kind of victory lap, he was even brought in by Jamie Dimon to help the bank unwind $20 billion of those busted trades.

But last week, after years of lackluster hedge fund performance, the 54-year-old Feldstein took a big step backwards. He sold his credit firm and its $19 billion asset base to an insurer, Assured Guaranty Ltd., for a bargain price of $160 million. Feldstein, a Harvard law school classmate of President Barack Obama, will now work in-house at Assured as chief investment officer.

“To succeed in the asset management business, you need scale, duration of capital, and a stable, motivated talent base,” Feldstein said in an interview, explaining the sale to Assured Guaranty. “That requires investment.”

BlueMountain will be getting a $500 million investment into its funds from Assured Guaranty, along with $90 million in working capital. Feldstein will receive $22.5 million of Assured stock as part of the deal.

Feldstein’s comedown in part reflects struggles plaguing the hedge fund industry, which has been littered with firm closures and widespread investor redemptions, $45 billion this year alone. But interviews with a dozen industry experts and past and present BlueMountain staff also paint a picture of a firm that faced numerous strains, including recent trading missteps.

PG&E Bet

A flop came in December when BlueMountain bet big on the comeback of utility PG&E Corp., believing liabilities from the California wildfires were overstated, according to a person familiar with the situation. PG&E filed for bankruptcy just a month later. In December PG&E’s stock plunged 10% to about $24. It’s currently trading at about $17, far below BlueMountain’s price target of more than $50 at the time. The firm is up on PG&E for the year, a person close to the fund said.

“The cynical view is he’s just cashing out before things get worse,” said Jeffrey Vale, chief investment officer of Infinity Capital Partners, which invests in hedge funds.

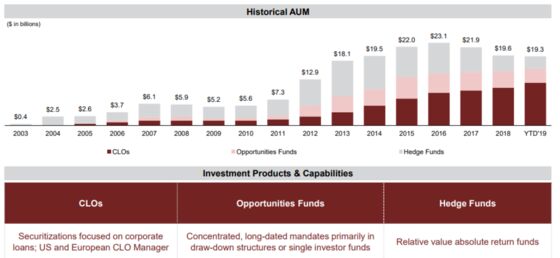

Feldstein co-founded BlueMountain in 2003 after working at JPMorgan for a decade. The fund was on a tear for its first 10 years, returning an average of 10% a year as firm assets swelled to more than $18 billion by 2013. It traded in abstruse derivative contracts such as credit-default swaps and mortgage bonds.

Feldstein’s reputation wasn’t that of a typical hedge fund manager known for markets or trading savvy, people who know him say. Rather, they describe him as a business-builder who is freakishly bright, bookish and introverted, someone who responds to challenges cautiously and with deep academic study.

But after the fund’s first decade that approach seemed to falter. Feldstein sold control of the firm to Affiliated Managers Group Inc., which came in as a minority investor in 2007 and later increased its stake to 54%.

In May, AMG wrote down its stake in BlueMountain by $415 million. AMG said in a filing at the time that the fair value of its investment in BlueMountain “had declined below its carrying value” and that the decline was “other-than-temporary.” AMG will receive $91 million as part of the stake sale.

Redemption Flow

BlueMountain’s flagship Credit Alternatives fund hasn’t met its return target of 8 to 10% since 2012. It has only beaten the U.S. 10-year Treasury bond once in five years. Despite that record, the fund charges performance fees of as much as 30% -- far above the industry standard.

Investors have yanked their money in recent years. Assets at BlueMountain’s hedge and opportunity funds plunged to $7.4 billion as of July from $14 billion in 2016. The flagship hedge fund in particular has lost more than $4 billion in just three years. It had just $2.6 billion as of July. Investors have asked BlueMountain for another $2 billion in redemptions over the next three years.

BlueMountain had carved out an expertise in the credit space, but Feldstein had broader ambitions. It began to push into stocks, launching a long-short equity book and raising a $1 billion quant equity portfolio. Both shuttered this year. One investor who declined to be identified said he pulled money out of frustration with the firm’s move beyond credit and with its high employee turnover.

“I think Andrew wanted to be a big multi-strategy manager, and I don’t think that was particularly successful,” Vale said.

As the hedge funds shrank, BlueMountain’s collateralized loan obligations business grew to nearly $12 billion, making up the vast majority of the firm’s assets now. That market has been booming even as regulators have raised concerns that such investment vehicles -- which rely on highly leveraged loans -- could suffer if the economy weakens.

Feldstein plans to grow BlueMountain’s CLO exposure by an additional $2 billion by mid-2020. On average, the firm’s CLO equity deals have returned 14% since 2005. While CLO fees are far lower than those for hedge funds, the business is considered lucrative because it’s easier to raise large sums of money.

Dominic Frederico, Assured’s CEO, said his company looked at 60 to 70 asset management companies over three years before deciding on BlueMountain.

“We found the right company with the right fit,” he said in an interview.

Assured Guaranty is paying the equivalent of just 0.83% of BlueMountain’s $19 billion in total assets under management -- and about 2.2% of the firm’s hedge fund assets alone. Brookfield Asset Management Inc. paid a 6.41% price-to-AUM ratio to buy Oaktree Capital Group LLC in March, for example. And Fortress Investment Group LLC got about 4.7% of its AUM in 2017.

Still, Feldstein, who once compared himself to Ulysses trying to avoid crashing his ship while charting through a rock and a hard place, remains optimistic.

“I’m really excited about the transaction,” he said. “We’re completely satisfied with the purchase price.”

--With assistance from Tom Maloney.

To contact the reporters on this story: Hema Parmar in New York at hparmar6@bloomberg.net;Nabila Ahmed in New York at nahmed54@bloomberg.net

To contact the editors responsible for this story: David Papadopoulos at papadopoulos@bloomberg.net, Larry Reibstein, Vincent Bielski

©2019 Bloomberg L.P.