Active Managers Get Caught With Too Much Money in Growth Stocks

Active Managers Get Caught With Too Much Money in Growth Stocks

(Bloomberg) -- The reopening rally, billed as a blessing for stock pickers, has failed to match hopes, at least as of yet. For many funds it made November another painful one when it came to competing with benchmarks.

Blame it on habits formed earlier in the year, when white-hot gains in tech megacaps and virtually nothing else chased managers into an ever-shrinking subset of growth companies. While the broadening stock-market gains of November may one day provide more fertile ground for picking stocks, right now fundamental managers are struggling.

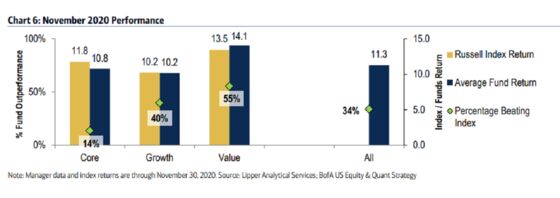

As good news on vaccines fueled a rotation out of tech, their leadership was supplanted by energy and financial shares, both of which have been shunned by money managers despite trading cheaply to earnings, Bank of America Corp. data shows. As a result, only 14% of large-cap core funds beat the Russell 1000 Index in November, the third-lowest hit rate in any month going back to 1991, according to data compiled by BofA.

“It was just a couple of weeks ago that every asset manager and portfolio manager that found their way to a microphone was saying tech is the winner, Covid is an influence that is going to be compelling and long lasting,” Scott Knapp, chief market strategist of CUNA Mutual Group. “Then along comes the vaccine. A lot of that groupthink means a large portion of the funds were tilted in the wrong direction as the rotation was taking place.”

The pattern played out Wednesday, a day when the S&P 500 rose about 0.2% while financial firms gained 1% and energy producers surged 3%.

The poor performance extends a tough year for active funds that first were punished for not owning enough of the five biggest stocks, Apple Inc. in particular, and then battered by the swift rotation from growth to value. At the end of November, only 20% of the funds have outperformed in 2020, down from 27% in September.

With a few weeks left to make up for the lost ground in 2020, managers may be forced to decide whether to embrace cheap stocks, according to BofA strategists led by Savita Subramanian.

“If market leadership remains biased toward value, current active funds’ embedded tilts toward growth stocks may hurt rather than help,” the strategists wrote in a note. “Lagging November performance was partly attributable to a negative value bias.”

Count the Fidelity Disciplined Equity Fund among those who took a hit in November, albeit a small one compared with the full year. The $1.7 billion fund, whose tech holdings made up about two-fifths of its portfolio, is up 26% this year, beating 95% of its peers tracked by Bloomberg. Over the past month, however, its ranking has fallen to the 12th percentile with a gain of a little more than 10%.

The Eaton Vance Stock Fund is another example where the reliance on tech giants became a brief alpha detractor. At the end of the third quarter, the fund allocated 28% of its money in the big five -- Microsoft Corp., Amazon.com Inc., Facebook Inc., Alphabet Inc. and Apple. The quintet trailed the rest of the S&P 500 by 5 percentage points in November.

Funds that pick stocks using a simple value or growth approach did better in November. About 55% of value funds tracked by BofA beat their benchmark and 40% of growth funds outperformed.

For blended funds, their preference for growth stocks likely reflected some level of doubt over the economic recovery with Covid-19 cases surging. As promising as vaccine development has been, questions remain about production, distribution, and the capability of the shot. But should the recovery trade continue, managers can’t afford missing the last opportunity to close their performance gap before their scorecard is booked for the year, according to John Augustine, chief investment officer at Huntington Private Bank.

“The fourth quarter is likely going to be the arbiter of how well active managers can be as fluid as the market is right now,” Augustine said by phone. “We will find out which active managers are deft enough to make that rotation.”

©2020 Bloomberg L.P.