A Wall Street Volatility Giant Gets Ready for a Dramatic Exit

A Wall Street Volatility Giant Gets Ready for a Dramatic Exit

(Bloomberg) -- After it shocked, frustrated and delighted investors for a decade, Credit Suisse Group AG is pulling the plug on the world’s biggest volatility exchange-traded product. Don’t expect it to go quietly.

The VelocityShares Daily 2x VIX Short Term ETN, ticker TVIX, has already flashed signs of becoming untethered from its underlying index following the Swiss bank’s bombshell announcement this week.

The plan to delist and suspend new shares is sending shock waves through the volatility-trading community -- and is even set to impact Wall Street’s infamous fear gauge.

It sets up a fittingly messy end for an invention that has long been a magnet for drama.

“Using TVIX was like taking the wheel of a Ferrari,” said Jim Carroll, portfolio manager at Toroso Advisors. “With a skilled driver, it could deliver outstanding performance. And a bad driver could wind up wrapped around a tree.”

The move is part of a “continuing effort to monitor and manage” exchange-traded offerings, Credit Suisse said in a statement Monday. The delisting will become effective on July 12, and the ETN may continue to trade over-the-counter.

The risks now, as ever, stem from both TVIX’s structure and size.

The ETN is levered, meaning it amplifies returns. It aims to move about twice as much as a basket of near-term futures on the Cboe Volatility Index, a gauge of expected price swings for the S&P 500 known as the VIX Index, and it has been phenomenally successful at attracting cash.

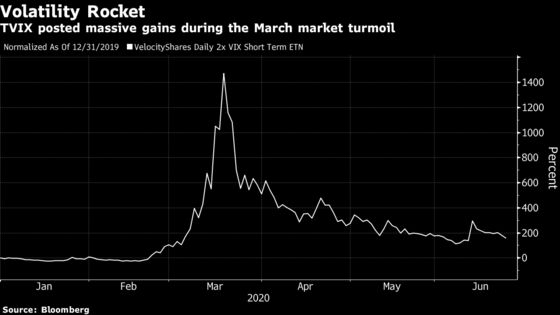

At the height of the coronavirus crisis, its assets swelled to more than $6 billion as stocks plunged and volatility soared. More than $1 billion remains, meaning TVIX is still a whale in the market for VIX futures contracts.

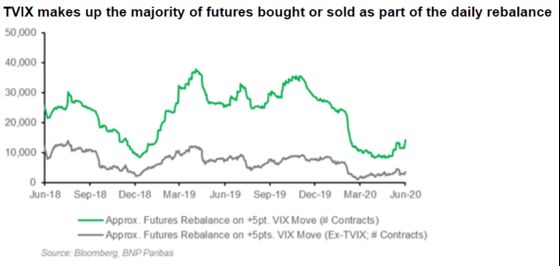

Hedging the note constitutes about half of the daily rebalancing between front-month and second-month VIX futures, according to BNP Paribas SA. Goldman Sachs Group Inc. reckons it has exposure equivalent to one-third of all open interest in the contracts.

As money flees the note in advance of the delisting, those futures will likely be sold. Because it’s such a massive player that means there could be downward pressure not only on the price of futures but on the volatility of the VIX itself, strategists say.

“The VIX ETP space will definitely take a hit until other products inevitably fill the void,” said Pat Hennessy, head trader at IPS Strategic Capital. “It remains to be seen how much of the AUM will actually migrate from TVIX” to similar products, he said.

Notorious ETP

Introduced in 2010, TVIX grew to become the largest product simulating a long position in the VIX, which typically moves inversely to stocks.

Largely shunned by professional traders, it ushered in a boom for retail speculation, with moms and pops able to bet on turbulence or enduring calm in U.S. equities -- with frequently ugly results.

When the bank suspended creations in 2012, TVIX surged to nearly a 100% premium to its net asset value. The price crashed when share issuance resumed, burning investors who bought in at an inflated level and setting off a firestorm of criticism.

“Volatility trading in general has a host of complex factors driving PnL that we suspect many retail investors do not fully understand, therefore making them unsuitable to trade positions of any kind,” said Ed Tom of Macro Risk Advisors.

Yet investors wanted to profit from market storms, or at least to cushion the rest of their portfolio, and TVIX provided their chance.

The VIX itself isn’t tradable, so the Credit Suisse product tracks an index holding a hypothetical basket of first- and second-month VIX futures contracts. It rolls those positions on a daily basis to maintain a constant weighted maturity of one month.

Since the VIX futures curve often takes an upward-sloping shape, one of the more unpleasant surprises awaiting unwitting buyers was the massive costs involved in rolling those contracts. Vance Harwood of Six Figure Investing estimated it cost investors 60% a year.

“They were effectively buying insurance against market drops,” said Harwood. “And insurance is often expensive.”

The dynamic can create striking contradictions. At the time of this week’s delisting announcement, TVIX was the best-performing ETP of 2020 amid wild pandemic markets, returning 204% through Friday. Simultaneously it remains among the worst-performing of all time, losing virtually all of its value since inception.

Another danger to investors has been the VIX’s tendency to mean-revert. For every upward spike there is typically a downward move just as vicious, which could leave holders of the ETN nursing percentage losses in the double digits in a single day.

Meanwhile its whale status means the note itself could make things worse.

While a spokesperson for the bank declined to comment beyond a press release on the reasons for delisting TVIX, experts point to the challenges of managing the note should another storm of volatility erupt.

“Any ETN that represents a large portion of open interest and volume in its underlying instruments is potentially dangerous for market microstructure,” said Benn Eifert, chief investment officer at QVR Advisors. “A sufficiently large adverse move could wipe out TVIX and leave the issuer holding huge losses.”

Any remaining danger will be greatly ameliorated if TVIX’s assets shrink in the lead up to, and aftermath of, its delisting. A shift to over-the-counter trading usually amounts to a death sentence for such funds, with retail investors unlikely to follow it to the pink sheets. Those who do will likely be holding a note priced at a premium to its underlying index that is difficult to trade.

On Monday, TVIX closed at 9.7% above its NAV, the most since March. It has since erased that premium, while no money has exited the product yet. Going forward, “supply and demand” will play a larger role in determining TVIX’s price than its index, said MRA’s Tom.

For all its drawbacks, TVIX’s sensitivity to the fear gauge combined with its leverage made it a potent way to profit from unrest over the past decade, and it continued to win followers right up until its delisting was announced.

The number of users holding the note on trading platform Robinhood climbed to 26,000 this month versus less than 3,000 at the beginning of February, according to Robintrack, a website unaffiliated with the site that uses its data to show trends in positioning.

“I went long TVIX in early/mid 2019 assuming big kabooms were coming given the state of the world and the complacency,” said Rob Majteles, founder of Treehouse Capital LLC. “I no doubt went long too early, but as things played out, despite the flaws of the product and its costs, I was well rewarded in March 2020.”

©2020 Bloomberg L.P.