Wall Street Says a Volatility Doom Loop Is Gripping Markets

Wall Street Says a Volatility Doom Loop Is Gripping Markets

(Bloomberg) -- There have been plenty of scares in the market horror show of recent weeks, but one idea in particular is increasingly sending shivers around Wall Street: that extreme stock turbulence may now be feeding itself.

The fear is that recent epic swings could be happening because volatility-sensitive players like risk-parity strategies and fast-money funds are aggressively deleveraging, exacerbating moves and sapping liquidity.

Throw in options dealers selling into weakness, and you have the stuff of market nightmares.

“High volatility combined with poor liquidity is creating a self-reinforcing loop,” Deutsche Bank AG strategist Parag Thatte wrote in an email.

A complex that has been a Wall Street whipping boy despite operating largely in the shadows is finding itself thrust into the spotlight given the sheer magnitude of swings. U.S. equity futures hit limit down again on Wednesday, a day after the underlying index surged 6%. In fact the S&P 500 Index has now moved an average 7.7% in the past seven sessions -- a bout of turmoil not seen since the Great Depression.

These volatility actors could help explain the link between the seemingly indiscriminate selling, the gruesome market depth and the violent shudders that have rocked assets in recent days.

Forced Selling

One trigger for all this was the S&P 500 Index’s 3.4% drop on February 24, according to Societe Generale SA.

On that day, dealers who make markets in equity options doubled down on selling stocks into weakness in order to hedge their exposure, a condition known as “negative gamma.”

“After that, all the other drivers went into play,” according to strategists at the French bank. “Deleveraging from passive funds (risk parity and vol target), short covering in the VIX market and forced selling in various assets to meet mark to-market constraints among others. The plunge in the oil price came as the final blow.”

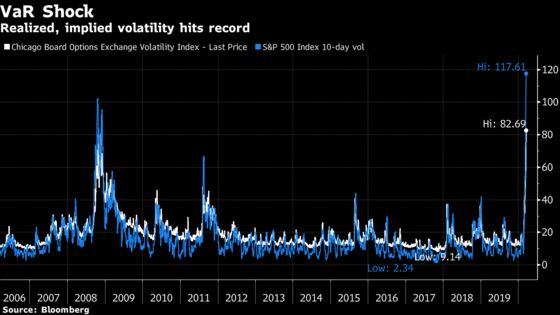

The carnage goes beyond stocks. At one point the entire U.S. Treasury yield curve fell below 1% for the first time ever. Oil crashed the most in 29 years. The Cboe Volatility Index closed at a record 82.69 on Monday -- but even at that eye-watering level, it’s actually lower than realized swings over the past 10 sessions.

In other words, markets are in the midst of a cross-asset maelstrom that looks strikingly like a “correlated asset market crash.” That’s what Vineer Bhansali and Larry Harris predicted might result from the boom in trades betting against price swings in a 2018 paper.

‘High Positioning’

Back then, Bhansali of LongTail Alpha LLC and Harris, a professor at USC’s Marshall School of Business, estimated the invisible hands of volatility-sensitive investors controlled more than $1.5 trillion. The group includes hedge funds, mutual fund managers, risk parity funds, banks, dealers and market makers, according to JPMorgan Chase & Co.

Lulled by an extended period of low-volatility, and aided by an implicit central bank put, the assets and leverage in such strategies kept growing. Risk-parity strategies alone hold an estimated $500 billion while volatility-targeting funds manage another $350 billion.

As long as market swings remain under control, these players continue to buy. But when a volatility shock arrives, they start to sell, and the more they have, the faster they unload. “Positioning going into this episode was very high,” said Deutsche Bank’s Thatte.

The loop comes because dealers and market makers -- those tasked with absorbing these flows -- also react to changes in volatility. When it’s high, these intermediaries widen bid-ask spreads to reduce their risk.

“One is feeding the other,” JPMorgan strategists led by Nikolaos Panigirtzoglou wrote in a note on Friday. “As volatility rises market makers step back from their market making role and raise bid offer spreads inducing low market depth and lower liquidity which in turns creates even more volatility.”

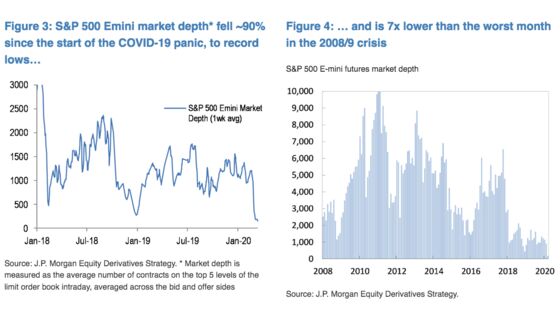

Depth Depleted

Market depth in U.S. equity futures is seven times worse than the poorest levels during the financial crisis, according to JPMorgan.

In bond markets, dealers have widened spreads and curbed their willingness to buy and sell, strategists at Bank of America Corp. wrote in a recent note. These dynamics “have materially worsened market functioning,” they said.

Equilibrium is restored only when prices reach a level where volatility-insensitive players -- like pension funds, insurance companies and sovereign wealth funds -- step in, according to JPMorgan. On the hopeful side, the bank says a crucial condition for that to happen has been met.

Meanwhile, Nomura’s Charlie McElligott reckons the pressure dealers are exerting on stock moves may ease following Friday’s options expiration, which will help put a damper on the stomach-churning swings.

But if Bhansali and Harris are to be believed, things could actually get worse before they get better.

The VIX climbing into uncharted territory makes predictions about the course of U.S. stocks uncertain at best. However in the black-and-white world of systematic volatility-sensitive investors, it’s likely just a sign of more forced selling to come.

“Strategies follow the VIX for risk allocation,” they wrote in the paper. “Large gyrations in the VIX affect the behavior of larger investors, creating a classic ‘tail wagging the dog’ outcome.”

©2020 Bloomberg L.P.