A VIX Copycat Tries to Break Cboe’s Monopoly on Volatility Products

Wall Street’s wildly popular fear gauge -- the VIX -- may finally get some real competition.

(Bloomberg) -- Wall Street’s wildly popular fear gauge -- the VIX -- may finally get some real competition.

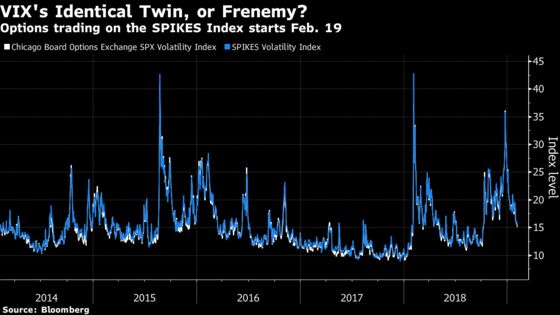

On Feb. 19, MIAX Options plans to debut options on a VIX copycat, the SPIKES Index, in an attempt to break up Cboe Global Markets Inc.’s monopoly on exchange-traded volatility products.

Cboe’s VIX propels a robust market for options and futures at the Chicago-based exchange, a lucrative business for the company. Prior attempts to compete with it have failed, and MIAX probably faces an uphill battle too. Daily volume for VIX options averaged more than 550,000 contracts at Cboe during the past three months.

The new product is being pitched as a lower-cost alternative to the VIX, with cheaper fees to trade the MIAX contracts. A company called T3 developed SPIKES. Its chief executive officer, Simon Ho, said it lowers “the cost of doing business significantly” and will compete on “quality, price, and innovation.”

SPIKES isn’t new. It was created in concert with Bats Global Markets Inc., an exchange Cboe bought in 2017. Introduced in 2016, there were never any options tied to it. Ho has now spent about four years talking to industry experts about what they like and don’t like about current volatility products, attempting to drum up support for the initiative.

“It’s been a monopoly -- and Cboe did a fantastic job -- but that’s why prices are high,” he said.

In a written statement, Cboe indicated that additional volatility products could boost demand for related securities it already offers.

“Any trading potential for VIX-like products would depend on traders being able to hedge those products likely using our liquid market for VIX futures and options,” the company said. “We would expect to benefit from the hedging flow that would potentially result from other volatility based products, reinforcing our confidence that the VIX Index will remain a premiere volatility benchmark.”

The VIX is calculated from out-of-the-money S&P 500 options, as are its futures and options. SPIKES is derived from options on the $253 billion SPDR S&P 500 ETF Trust, the largest exchange-traded fund in the world. Because both are based on the same benchmark U.S. stock index, SPIKES and VIX move almost in lockstep.

According to Ho, five banks want to be involved in these options from “almost day one,” and consultations with agency brokers, hedge funds and tail-risk managers have been “extremely positive.”

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Nick Baker, Dan Reichl

©2019 Bloomberg L.P.