A Vanishing Treasuries Trade Poses Threat to Largest Debt Market

A Vanishing Treasuries Trade Poses Threat to Largest Debt Market

(Bloomberg) -- A Treasuries arbitrage strategy favored by hedge funds has fallen into near-hibernation, threatening liquidity in the world’s largest debt market.

Bets that use borrowed money to profit from tiny price discrepancies between futures and the underlying cash Treasuries unraveled in a matter of weeks amid the global rush to safety in March. Known as the cash-futures basis trade and commanding almost $1 trillion at its peak, the strategy is now about half that size, and many analysts doubt it will revive: The profit potential has shrunk, and traders are still smarting from their first-quarter pain.

The fate of the trade has crucial implications for the $20 trillion Treasury market, with the Federal Reserve already buying billions of dollars of U.S. obligations to keep it functioning smoothly. The popular wager’s decline risks making it harder to transact in America’s debt at a time when investors are facing a record glut of government bonds.

“For the foreseeable future, there are many good reasons why people would be cautious about getting back into the basis trade,” said Ken Monahan, a senior analyst covering market structure and technology at research firm Greenwich Associates. “That has implications for bond-market liquidity because it’s been a huge driver of activity on most cash-trading platforms” as well as on dealers’ so-called dark pools.

The trade works like this: the price of Treasury futures, a product of CME Group Inc., converges with underlying securities at expiration. Before then, investors may be able to buy the “cheap” bonds and sell the futures to capture any difference that exceeds the cost of financing the trade. The spread between the two, or the basis, is usually minuscule, so funds borrow cash to leverage positions and increase returns.

But in the panic of March, investors piled into the most liquid assets, which in Treasuries meant futures over cash. That blew out the spread between the two and triggered a stampede out of the cash-futures basis trade. When the Fed then intervened to pump in liquidity, there was a sense of relief on Wall Street but also of frustration over how some firms had once again landed in trouble by heaping on leverage. Now the market is keen to see the trade return.

Ripple Effect

The dislocation was so great at the time that it rippled across fixed income, causing a key source of corporate cash to seize up. That spurred the Fed to promise trillions of dollars of liquidity to calm short-term financing markets. Meanwhile, in cash Treasuries, the tremendous volatility of the period caused turnover to shrivel and spurred the Fed to step in there too.

Months later, activity has yet to recover in certain areas, and the diminished basis trade is a contributor to that -- on top of Fed policy that has helped quash volatility.

“It impacts the amount of volume in the Treasury futures market,” said Tom di Galoma, managing director of government trading and strategy at Seaport Global Holdings. “And it will negatively impact liquidity in the off-the-run Treasuries, which are used in many basis trades.”

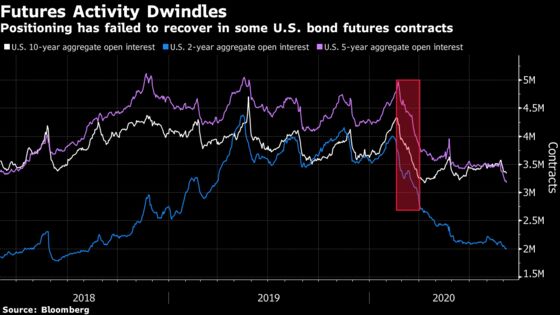

Volume in Treasury futures and other interest-rate products was down about 35% from April through August compared with the year-earlier period, CME data show. In one example, open interest in U.S. five-year note futures has tumbled to the lowest since 2018.

In cash Treasuries, turnover on CME’s BrokerTec, the biggest platform for electronic trading of Treasuries, fell roughly 38%.

There are a couple of ways to estimate how much activity in the basis trade itself has shrunk. One is leveraged funds’ gross short positions in Treasury futures, which have plunged from their 2020 peak reached before the pandemic-sparked volatility.

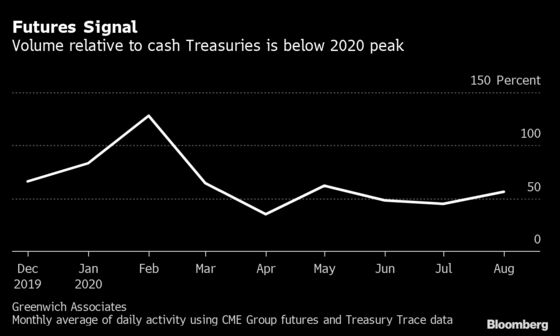

Another is Treasury futures volume as a percentage of cash dealings, a metric Monahan points to. This also shows a big drop, with futures volume plunging.

Before March, the basis trade was viewed as a low-risk arbitrage. But its profitability relies on stability in financing rates and futures margin requirements. Those things went out the window amid the March turmoil.

And because of where financing rates and the basis itself wound up, returns on new basis trades have become negative, researchers at the Treasury Department’s Office of Financial Research wrote in a July report.

“Basis trades remain unattractive for hedge funds,” the researchers wrote.

Rebound Scenario

Still, regulatory mandates on banks continue to make it one appealing way to use their balance sheet, according to Joshua Younger, head of U.S. interest-rate derivatives strategy at JPMorgan Chase & Co., who expects basis activity to recover. And hedge funds will want to preserve access to that leverage.

The leverage in the trade can threaten financial stability, as evident in March, he said. But a rebound would be positive as “less basis trading by hedge funds means less demand for Treasuries, which could lead to higher interest rates,” Younger said. “It creates a place to put the massive quantity of Treasuries that are being issued to fund the deficit in a way that has less price impact.”

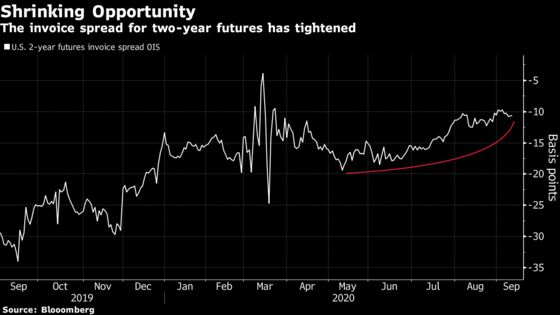

Even so, its appeal has undoubtedly ebbed. For one thing, lower volatility has made other trades, such as those using options, more attractive. But even more important, the gap between cash and futures prices has shrunk, as seen in what’s known as the invoice spread.

By contrast, at the peak of the basis trade, most futures were even more costly relative to cash Treasuries than extremes reached in 2006, according to UBS Group AG.

“There is less incentive for the hedge funds to do the trade now as the basis isn’t so negative,” said Michael Cloherty, a strategist at UBS. “And volatility out to five years is low given the Fed is expected to be on hold for years. So less volatility means less relative-value opportunities, so you’ll just see less RV trade, such as the basis.”

©2020 Bloomberg L.P.