A Stock Market Dying to Know What Powell Knows About the Economy

Powell seemed more committed than ever to cutting rates. If you own stocks, you’re partly happy, partly scared.

(Bloomberg) -- Two things keep investors awake at night these days. One is wondering how worried to be about manufacturing. The other, a nagging concern that Jerome Powell has better insights into the economy than they do.

Hop on Twitter and you see it, people lambasting the Federal Reserve chairman for even considering stimulus when 224,000 jobs were just added to payrolls, home sales are bouncing back and stocks sit at records. And yet in congressional testimony this week, Powell seemed more committed than ever to cutting rates. If you own stocks, you’re partly happy, partly scared.

“If you just took somebody from outer space who had read every economics book and showed them the data of unemployment and consumer confidence, they’d assume the economy is on fire,” said Peter Mallouk, president of Creative Planning, a wealth-management firm with about $42.5 billion in assets under management. “People feel like he knows something that everybody else doesn’t.”

Maybe it’s a little rich to question Powell’s logic a few months after demanding he act to halt losses. But consistency is often in short supply when investors get anxious. Thanks to Fed doves, the dark days of December have been forgotten, with the obsession over rate cuts replaced by an obsession over what they’re intended to cure.

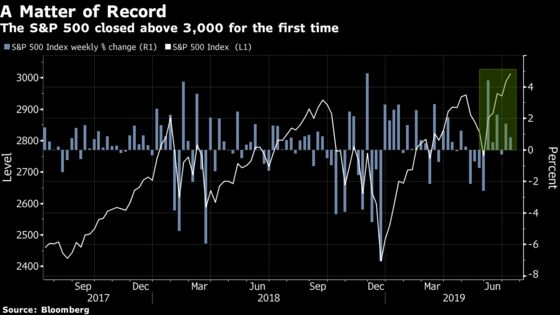

It was a week of conflicting emotions. Headlines trumpeted the S&P 500 powering past 3,000, but the wire-to-wire gain wasn’t even 1%. While nothing to complain about, the advance was the smallest for any pre-earnings week in three quarters.

Into that mix comes the quarterly parade of corporate reports, set to begin in earnest next week. And while early indications are notoriously unreliable when it comes to earnings season, right now they are instilling little confidence.

Profits are expected to drop about 3% from last year, making this season “the worst of times,” according to Bloomberg Intelligence analyst Gina Martin Adams. Eight of 11 sectors are forecast to post declines in per-share earnings growth, with analysts and companies cutting second-quarter views “to the bone,” she said.

Early reports from companies with exposure to multiple sectors have been worrisome. Nuts and bolts supplier Fastenal Co. plunged after disappointing the market. So did peer MSC Industrial Direct Co., which fell after earnings trailed estimates. BASF SE, whose plastics and pesticides are found in everything from cars to crops to computer chips, said the trade war threatened to cut its profits by 30% this year.

“They were talking about tariffs and margins and I think that’s going to be a characteristic of the reporting season,” said Charlie Smith, founding partner and chief investment officer at Fort Pitt Capital Group in Pittsburgh. “Markets are doing their happy dance over the fact that the Fed’s going to cut. But I think there’s going to be some choppiness from weak earnings.”

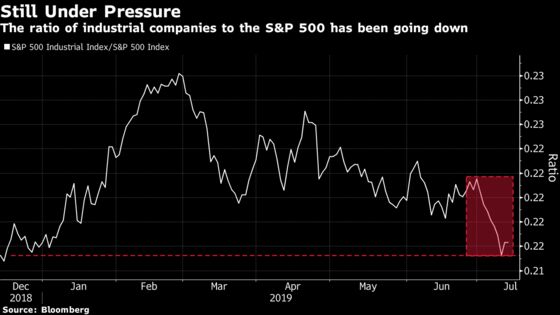

Other all-purpose industries are showing weakness, too. Daimler AG, the world’s biggest producer of luxury cars, sees earnings falling “significantly.” Illumina Inc., a medical technology firm, lowered its expectations for the year. Trucking company U.S. Xpress Enterprises Inc. cut its second quarter expectations, saying freight hasn’t seen typical seasonal improvements due to trade, industrial production and weather.

Transport stocks, in particular -- with their reputation for economic prescience -- are showing weakness, with Citigroup, Deutsche Bank and Credit Suisse all cutting projections on trucks this week. “Broad volume indicators suggest demand remains soft, as shippers are slowing capital deployment given elevated uncertainty in global trade,” wrote Citigroup strategists led by Christian Wetherbee.

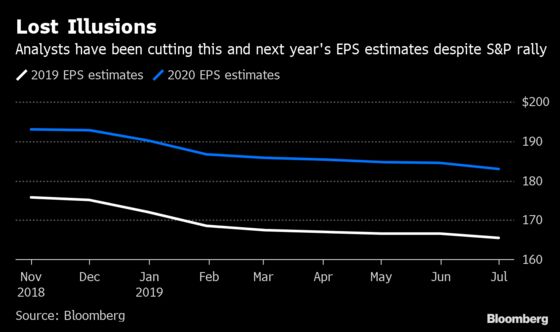

Even if you don’t think any individual quarter moves the needle, you can’t feel great about the larger trend in profit estimates, where analysts have been slashing longer-term views for the better part of a year. They now see the S&P’s per-share earnings at $165.60 in 2019 and $183.00 in 2020. Both are $10 lower than in November.

“There are a lot more risks underlying this market than the tape would imply,” wrote Tom Essaye, a former Merrill Lynch trader who founded “The Sevens Report” newsletter. “If global economic data does not stabilize, or earnings estimates fall further, then that will eventually outweigh the dovishness.”

The common thread is trade. Though phones connecting the U.S. and China are ringing again, the fallout lingers. Chinese export growth slowed last month and imports shrank more than expected. Manufacturing everywhere is slowing. A gauge of U.S. factory activity posted its third monthly decline and dropped to the lowest level since October 2016.

A reasonable response to the negativity is: who cares? The S&P 500 is now up 20% on the year, it closed Friday at a record, and even bond yields perking up a bit. But apathy doesn’t describe investor behavior. A recent Bank of America survey found its clients are the most bearish since the 2008 financial crisis, with trade and recession concerns driving much of the pessimism. Average cash balances soared, according to the bank, marking the biggest jump in cash since the debt ceiling crisis in 2011.

People are getting defensive at UBS Group AG, according to its head of wealth management, Jason Chandler. “Clients are being a little bit more conservative and they’re holding more cash,” Chandler told Bloomberg TV. “U.S.-based clients are holding roughly 25% of their holdings in cash, and it’s less about a market pullback where they’re going to invest -- it’s just being comfortable to go to sleep at night.”

Of the $28.7 billion yanked from global equity mutual and exchange-traded funds in the week ended July 2, more than $25 billion fled U.S. products, data compiled by Investment Company Institute show. Those outflows from American active and passive funds were the third-biggest since 2013.

Bulls note it’s hard to be pessimistic looking at groups like tech, where Amazon.com’s value just hit $1 trillion, while the Fang group comprising it, Facebook, Alphabet and Netflix gained for 23 out of 26 sessions, something it’s never done before. And look at the strong June jobs report, the dwindling jobless claims, and inflation data coming in firmer than expected.

And yet, those are the same bulls betting on a quarter-point reduction in interest rates at the end of this month. Following Powell’s testimony to Congress this week, traders have priced in almost three quarters of a point of easing by the end of the year.

For Peter Cecchini, the global chief market strategist at Cantor Fitzgerald, it’s a little confusing.

“A look at history should be creating considerably more dissonance for market participants than it is right now,” he wrote in a note this week. “Late cycle cuts, no matter how masterful any Fed maestro might be, tend to be followed by recession within several months. Risk assets tend not to perform well during such periods.”

To contact the reporters on this story: Vildana Hajric in New York at vhajric1@bloomberg.net;Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.