A Weak Pound Can Still Create Opportunities

A Weak Pound Can Still Create Opportunities

(Bloomberg) -- What’s bad for the pound is good for the FTSE 100 -- that’s the mantra of investors who favor U.K. exporters over domestic equities this year. The currency is likely to remain troubled by deteriorating macroeconomic data, the impending change of prime minister and the looming Brexit deadline. But is the case for British large caps as compelling as it appears?

On average, FTSE 100 companies derive more than 70% of their revenue abroad, more than most European peers, while about 45% of their dividends are labeled in dollars and converted to sterling. And the pound fell to a two-year low against the dollar this week, as economic sentiment soured.

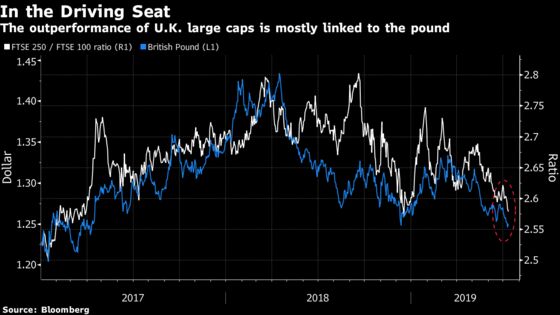

The relative ratio between the FTSE 250 and FTSE 100 is now back to mid-June lows and should continue to drop, according to Mint Partners Cross-Asset Sales trader Gurmit Kapoor. The next chart shows the ratio has recently broken below its long-term uptrend and is probably heading toward June 2016 lows, Kapoor says.

Poor retail sales and contracting PMIs in June are signaling a slowdown of the U.K. economy for first time since 2012, which is unlikely to support the currency in the short term.

Politics is playing the bigger part in the trend, though. The two candidates to be prime minister are keen to take the U.K. out of the EU by Oct. 31, with a no-deal departure under serious consideration. Conflict with Parliament might also be on the cards and uncertainty is likely to persist.

- READ: Brexit Drama Is The Big Issue for U.K. Stocks in Second Half

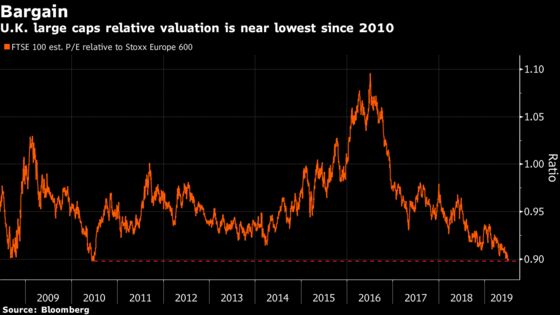

But nevertheless, the view on the nation’s stocks has improved recently. Citi and Barclays strategists have upgraded U.K. equities over the past few weeks, saying the uncertainty should provide a cap to the pound for now. The Brexit risk premium provides a “land of opportunities,” wrote Citi strategist Jonathan Stubbs, setting a target for the FTSE 100 of 8,000 by mid-2020. Looking at the relative valuation of the gauge against the Stoxx Europe 600, it’s now at lows last seen in 2010 and 2008.

In the meantime, FTSE 100 contracts are gaining 0.3%, while the pound is rising 0.2% against the dollar, and Euro Stoxx 50 futures are trading up 0.4% ahead of the open.

- Watch U.K. homebuilders following a report which showed new buyers increased in June for the first time since November 2016. Watch Taylor Wimpey, Persimmon, Bovis Homes among others.

- Watch oil stocks as about a third of the Gulf of Mexico’s output was cut before a potential hurricane and U.S. crude inventories shrank more than expected. Brent crude and WTI futures edged higher, extending gains after contracts in New York finished above $60 a barrel for the first time since May.

- Watch for more central bank comments after Fed Chairman Jerome Powell provided further hints at an impending rate cut on Wednesday. ECB publishes an account of its June 5-6 policy meeting, with most economists expecting more stimulus to be announced by September at the latest. Bank of England Governor Mark Carney is also speaking.

- Watch the trade front as investors in Asia remain cautious over the ongoing Japan-South Korea spat, with no easy exit in sight, while the U.S. is investigating France’s taxation plans on tech giants.

COMMENT:

- “Full-year guidance from companies reporting in 2Q will be key, given our earnings model suggests that consensus for 2019 is still over-optimistic,” Bloomberg Intelligence strategists Laurent Douillet and Tim Craighead write in a note. “Following the most pre-announcements since 4Q 18, sales and EPS estimates merit further cuts, we believe, prolonging the tug of war with the equity-market’s looser monetary-policy-driven re-rating. ”

COMPANY NEWS AND M&A:

- Reckitt Benckiser to Pay Up to $1.4b to Resolve Federal Probes

- Deutsche Bank Faces U.S. Justice Department Probe Over 1MDB (1)

- AB InBev Asia Unit Guides Hong Kong IPO Pricing Toward Bottom

- Norwegian Air Second-Quarter Ebit Misses Estimates

- Norwegian Air CEO and Founder Kjos Steps Down Amid Turnaround

- Barry Callebaut 9M Sales CHF5.48b; Confirms Mid-Term Guidance

- Ryanair CEO May Pare Growth Plans If Max 737 Grounding Drags On

- Swiss Re Suspends ReAssure IPO on ‘Weaker’ Market Conditions

- DNB Second-Quarter Net Income 1.5% Below Estimates

- Bayer’s Toll of Roundup Misery Depends on Who Runs the Numbers

- Credit Suisse StarKhan’s Thwarted Ambition Led to Rift With CEO

- HSBC Key Target Prone to Manipulation by Managers, Auditors Said

- Krones Cuts Full-Year Pretax Profit Margin Forecast

- Russia Files RUB60b Tax Claims vs Tobacco Companies: Vedomosti

- Nordic Semiconductor Second-Quarter Revenue 1.1% Below Estimates

- Vivendi: Mediaset Minority Withdrawal Price Undervalues Co.

- Atlantia: Italy May Soften Position on Autostrade Concession: Repubblica

- Suedzucker Profit Drops, Reaching Fruit Unit Target ‘Difficult’

- Bossard Sees 2019 Ebit Margin at Lower End of 10%-13% Range

- Fielmann 2Q Sales, Profit Up as Company Eyes Top Spot in Eyewear

- Mediolanum Ready to Consider Acquisitions, CEO Tells Il Sole

- Energean Oil & Gas Offering by Holders Prices at GBP9.50/Share

NOTES FROM THE SELL SIDE:

- Piper Jaffray cut British American Tobacco to neutral from overweight, saying the tobacco firm is likely to deliver decent top-line and margin momentum but softer U.S. expectations and competition in reduced-risk products means there is limited upside for the shares. PT is cut to 3,100p.

- Getinge’s recovery looks real and, while shares have rallied this year, the move is justified, Berenberg says, upgrading the stock to buy from hold and raising price target to SEK180.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 397.9 (May 2018 high); 403.7 (2018 high)

- Support at 385.7 (76.4% Fibo); 380.9 (50-DMA)

- RSI: 55.6

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,520 (76.4% Fibo); 3,596 (May 2018 high)

- Support at 3,412 (50-DMA); 3,403 (61.8% Fibo);

- RSI: 60.3

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Cobham upgraded to overweight at Barclays; PT 1.35 Pounds

- Gestamp upgraded to buy at Kepler Cheuvreux; PT 5.60 Euros

- Getinge upgraded to buy at Berenberg

- Holmen upgraded to buy at AlphaValue

- Meggitt upgraded to buy at Goldman; PT 6.62 Pounds

- SCA upgraded to buy at AlphaValue

DOWNGRADES:

- Aixtron downgraded to neutral at Oddo BHF; PT 8 Euros

- BAT downgraded to neutral at Piper Jaffray; PT 31 Pounds

- Experian downgraded to neutral at Goldman; PT 26 Pounds

- Glencore downgraded to market perform at BMO

- Mowi downgraded to hold at Fearnley; PT 201 Kroner

- Oerlikon downgraded to sector perform at RBC; PT 12.50 Francs

INITIATIONS:

- Belships rated new hold at ABG; PT 7 Kroner

- Fluidra rated new overweight at JPMorgan; PT 14.50 Euros

MARKETS:

- MSCI Asia Pacific up 0.2%, Nikkei 225 up 0.4%

- S&P 500 up 0.5%, Dow up 0.3%, Nasdaq up 0.7%

- Euro up 0.19% at $1.1272

- Dollar Index down 0.22% at 96.89

- Yen up 0.44% at 107.98

- Brent up 0.1% at $67.1/bbl, WTI up 0.2% to $60.5/bbl

- LME 3m Copper down 0.1% at $5936/MT

- Gold spot up 0.2% at $1421.7/oz

- US 10Yr yield down 2bps at 2.04%

ECONOMIC DATA (All times CET):

- 8:45am: (FR) June CPI EU Harmonized MoM, est. 0.3%, prior 0.3%

- 8:45am: (FR) June CPI MoM, est. 0.2%, prior 0.2%

- 8:45am: (FR) June CPI YoY, est. 1.2%, prior 1.2%

- 8:45am: (FR) June CPI Ex-Tobacco Index, est. 104.1, prior 103.9

- 8:45am: (FR) June CPI EU Harmonized YoY, est. 1.4%, prior 1.4%

- 11am: (IT) ECB’s Visco presents Bank of Italy’s annual AML report

* For a wrap on developments in European equity capital markets, click here.

--With assistance from William Canny.

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.