A Market Guide to a Brexit Deal, If and When It Finally Happens

A Market Guide to a Brexit Deal, If and When It Finally Happens

(Bloomberg) -- Follow @Brexit on Twitter, join our Facebook group and sign up to our Brexit Bulletin.

U.K. negotiators have secured a deal with the European Union to exit the bloc, and on Wednesday Prime Minister Theresa May will try to win over her Cabinet and later, Parliament. For investors, a done deal would remove one of the biggest overhangs in European markets since the 2016 vote.

Of course, we’re not exactly there yet. Some U.K. ministers have preferred quitting to backing May’s blueprint in the past, and the math for getting it through Parliament still looks challenging. But traders are turning a little more optimistic, with the pound gaining as much as 1.5 percent on Tuesday and domestic mid-caps jumping.

It’s too early to breathe a sigh of relief, but this is what an orderly Brexit could mean for U.K. markets:

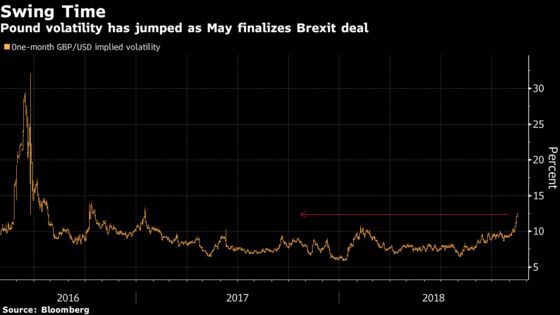

Currency

It’s prime time for the pound. The pound-dollar rate is paring some of Tuesday’s gains, and a jump in implied volatility shows the success of May’s deal is nowhere near certain.

“If the deal is seen as favorable, I think sterling could quickly move to $1.40 and if negative it will re-test the recent lows around $1.20,” said Roger Jones, head of equities at London & Capital. “If the Conservatives splinter on the back of a ‘failed’ Brexit and the possibility of a Corbyn Labour government increases, then sterling will come under further pressure.”

Three-month risk-reversal rates in pound-dollar options, a bellwether for market sentiment, have recovered but remain negative, a sign traders are still bearish. Even a fudged deal might not be too uplifting, since it could kick the can down the road when it comes to the actual details.

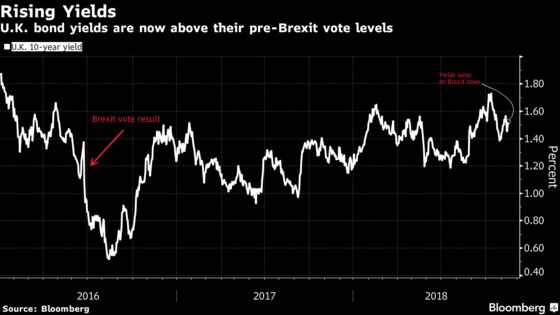

Bonds

Gilts rallied following the Brexit referendum as investors sought the safety of sovereign debt. They have sold off since, after global yields rose and domestic economic growth remained solid, allowing the central bank to raise interest rates. Yields jumped on Tuesday, as a Brexit deal would increase the chance of more tightening.

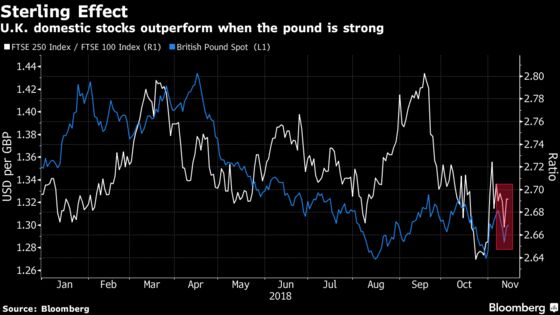

Equities

Since the vote, smaller companies -- which are more sensitive to the local economy -- have trailed larger ones, whose overseas earnings tend to benefit from sterling weakness. That’s why the FTSE 250 is extending its outperformance over the FTSE 100 and Stoxx Europe 600 on Wednesday.

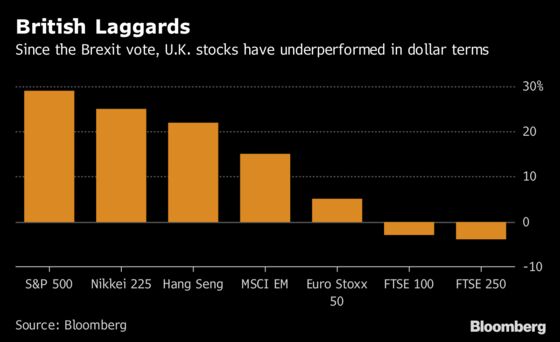

Brexit hasn’t exactly ruined U.K. equity returns when calculated in the local currency, but in dollar terms, it’s made British stocks underperformers. On such a basis, the U.K. is the only major developed market to have handed investors zero returns since that fateful day of the Brexit referendum in June 2016.

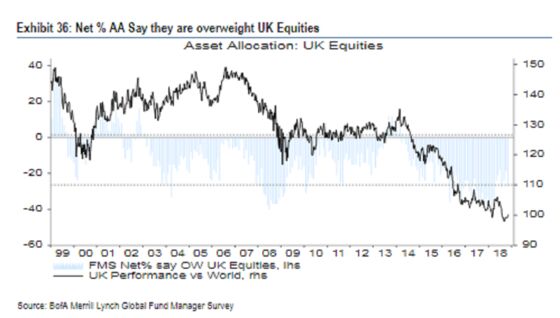

That’s one reason Bank of America Merrill Lynch’s surveys show a rising net percentage of global fund managers underweight on U.K. stocks since Brexit. A deal could help fuel more inflows into British as well as European shares.

“A soft and orderly Brexit could contribute to making both U.K. and European equities more ‘investable’ to global investors,” Barclays strategists led by Emmanuel Cau wrote in a Nov. 6 note.

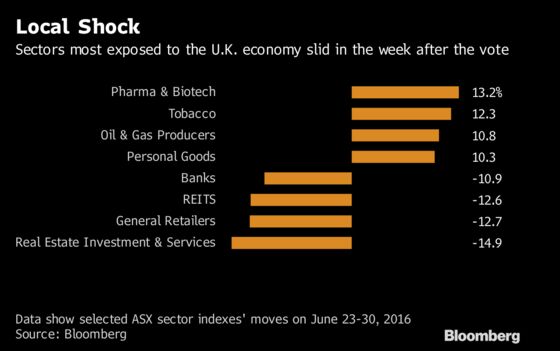

A look at what sectors did during the week after the vote sheds some light on how they might respond to a deal. The worst stock performers were more exposed to the local economy -- real estate, general retailers, banks -- whereas the winners were exporters like energy or tobacco stocks.

Outside the U.K., automakers may benefit from a deal as the the country is Europe’s second-biggest premium car market, Societe Generale strategists wrote in an Oct. 30 note. Overseas banks with a strong presence in Britain, such as Spain’s Banco Santander SA, may also gain.

But, ultimately, many investors would rather not make political forecasts until the dust settles.

“Few global investors feel they have an edge in predicting the next few rounds of British politics,” Mark Haefele, global chief investment officer at UBS Wealth Management, wrote in an email. They “prefer to stay neutral on U.K. equities while looking for opportunities more amenable to financial analysis.”

To contact the reporters on this story: Justina Lee in London at jlee1489@bloomberg.net;Charlotte Ryan in London at cryan147@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon, Tom Lavell

©2018 Bloomberg L.P.