A Game Theory Hypothesis on the Stock Market's G-20 ‘Conundrum’

A Game Theory Hypothesis on the Stock Market's G-20 ‘Conundrum’

(Bloomberg) -- Jerome Powell’s out of the way, now it’s Donald Trump’s turn. A week after the Federal Reserve chairman’s dovish turn sparked a rally in just about everything, markets are on edge as the president heads to Japan for trade talks with his Chinese counterpart.

Investors have been eyeing the coming Group of 20 summit for weeks as the next best chance to resolve the dispute ever since Trump escalated tensions with Xi Jinping by raising tariffs. Any sign of detente, the thinking went, would rejuvenate animal spirits and usher in a summertime rally.

But Powell -- while giving the market exactly what it wanted -- gummed up the analysis. A Fed standing ready to cut if signs of economic weakness persist gives the president one less reason to settle with the Chinese, threatening a bull run in stocks. And if he does a deal, Powell’s hawkish side could well reassert itself, putting gains in gold and Treasuries at risk.

“More accommodation by the Fed, which the market likes, enables Trump to pursue a more aggressive policy, which the market does not like,” said Ryan Giannotto, director of research at GraniteShares Inc. “That’s the crux of the issue. It really is a real conundrum for markets.”

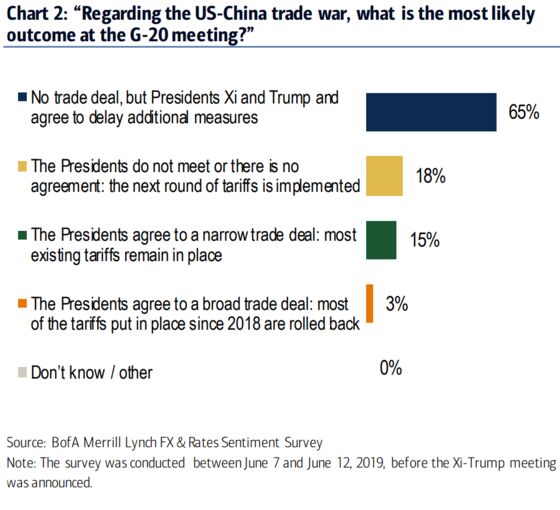

Relax, is the message from Bank of America. The most likely outcome is that Trump and Xi agree to more talks without escalation, the bank wrote in a note to clients, framing the summit as a “major event” with “minor expectations.”

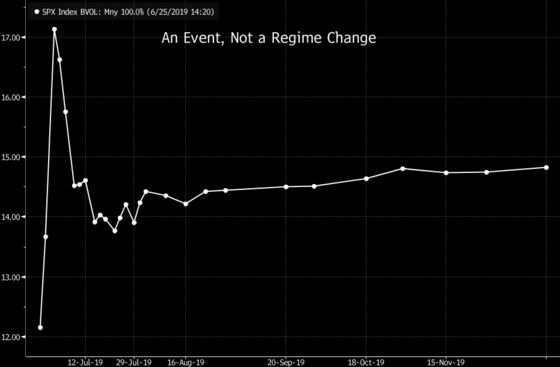

Calm also seems to be prevailing in the options market, where the summit is just a blip on its radar: Forward volatility points to fireworks in the S&P 500 on July 1, the first trading day after the weekend meeting, but after that traders see a return to tranquility.

Looking at the forward curve on the Cboe Volatility Index prompted Pravit Chintawongvanich, Wells Fargo’s equity derivatives strategist, to recommend positioning for a “vol crush” after the event by buying puts on an exchange-traded fund that benefits from turbulence in stocks, known by its ticker VXX.

Markets euphoric over the Fed’s dovish turn may place too much emphasis on any sign of progress in trade talks, warns Priya Misra, global head of rates strategy at TD Securities.

“There have been points in time throughout the U.S.-China trade dispute that market optimism has perhaps outpaced pragmatic skepticism, eventually leading to sharp asset-price adjustments once reality sets in,’’ she wrote in a recent note.

Similar to Bank of America, TD expects the two leaders to make progress, but sees a “near-zero probability” of an actual deal. Misra said such an outcome would be welcomed warmly by emerging-market assets and growth currencies in the G-10 like the New Zealand kiwi, while also fostering a modest increase in the 10-year yield, according to TD.

UBS Investment Group sounded a more cautionary tone, noting that the Fed’s willingness to cushion the economy from the impact of a protracted trade war dims any hope for a quick grand bargain -- either this weekend or in the near future.

The consequences of an impasse could be enormous -- with a 20% rout in global equities possible in the worst case, unless a deal is struck in the coming weeks, the bank has warned.

Trump administration officials this week have been lowering expectations for a deal, while at the same time emphasizing that they expect progress to be made. The S&P 500 fell for a fourth day Wednesday to cap its longest slide seven weeks.

Some on Wall Street are ready to turn super-bullish should the prospects for trade brighten materially, even if Powell has twice directly linked his willingness to cut to the spat’s drag on the economy.

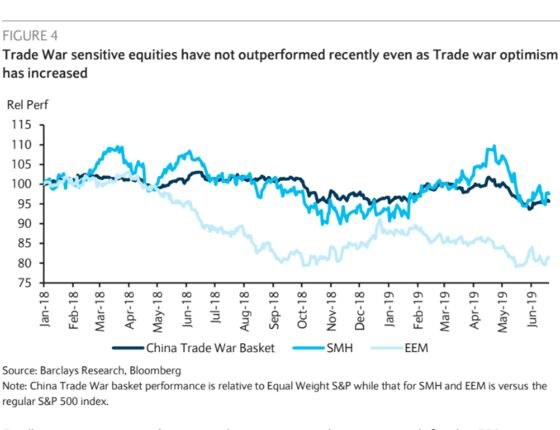

Barclays strategists led by Maneesh Deshpande are musing about a potential melt-up in equities, noting that stocks exposed to the trade war, like chipmakers and heavy-machinery producers, haven’t outperformed as the S&P 500 rallied to an all-time high last week. Instead, it’s been defensive shares and bond proxies.

Bank of America’s head of high-grade credit strategy, Hans Mikkelsen, says he doesn’t need to wait for the aftermath of the meeting for his unbridled enthusiasm to shine through. He just wants to get past the event and deal with the outcome, so any news will be good news for corporate debt, he reckons.

It’s Time to Increase Your Allocation to Corporate Bonds: BofA

“Between now and the conclusion of the G-20 meeting we should know whether the situation is converging toward a deal and meaningfully higher interest rates, trade war escalation and a sizable move lower in rates, or something in-between,” Mikkelsen wrote. “The leg tighter in credit spreads and flatter curves will accelerate after G-20 when we get more clarity on trade and uncertainties about long term rates lift -- regardless of which scenario plays out.’’

To contact the reporters on this story: Vildana Hajric in New York at vhajric1@bloomberg.net;Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Rita Nazareth

©2019 Bloomberg L.P.