A Fund Manager Lesson From Japan: Buy Growth When There Is None

A Fund Manager Lesson From Japan: Buy Growth When There Is None

(Bloomberg) -- The message to investors from Aisa Ogoshi is clear: buy growth stocks when there is no growth.

To the fund manager at JPMorgan Asset Management, what happened in Japan over the past 20 years backs up her call to stick with faster-growing companies. When the country’s economy was struggling, it was investors who bet on growth that made money through the cycle, not those who went bargain hunting, according to Ogoshi, whose Pacific Securities Fund has beaten 97% of peers over the last five years, according to data compiled by Bloomberg.

“In a low growth environment, people want to stick to quality where they could trust the management,” she said in an interview in Hong Kong. “And if there is any type of growth, all the money will chase that.”

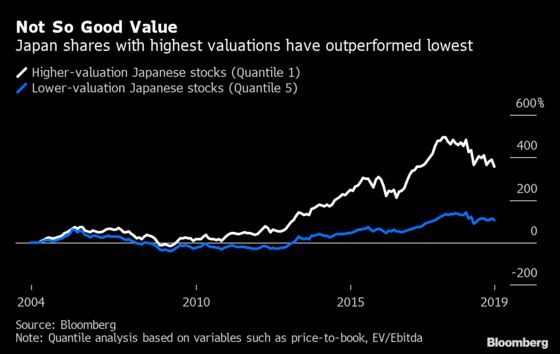

Over the past 15 years, a basket of stocks with the highest valuations, which includes many growth stocks, significantly outperformed shares with the lowest valuations, according to a Bloomberg factor analysis on Japan’s benchmark Topix Index. The former saw a return of over 350%, with the latter rising by about 105%.

Growth stocks “tend to have high multiples, but over the cycle, we have witnessed some of them are able to deliver growth and keep growing their market share,” said Ogoshi, naming examples such as sensor manufacturer Keyence Corp which has risen more than 600% over the past ten years.

Still, it’s inevitable that an economic slowdown would also affect companies in growth universe, and valuations also have reached a level that investors should be more selective, Ogoshi said. Her fund recently trimmed a position in pharmaceutical company CSL Ltd. and some Chinese health care names, as their valuation leaves them “no room for mistakes or bad news”, she said.

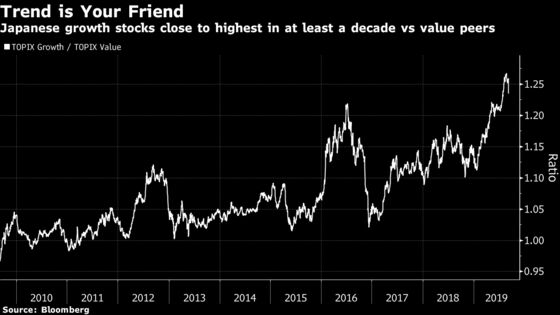

While growth stocks have been trouncing their value peers in recent years globally -- in Japan the factor is close to at least a ten-year relative high -- this month has seen the trend showing signs of losing steam. Though at an early stage, the reversal has raised questions over whether there could be a comeback for the least-loved investment factor.

“A trigger for a reversal of this trend would be a rise in interest rates, however, a lot of people think that the markets have factored in monetary easing globally and there’s no sign of inflation anywhere,” said Yoshinori Shigemi, a global market strategist for JPMorgan Asset Management Japan Ltd. in Tokyo. “Given that, it’s difficult to see this trend will end.”

For now, Ogoshi is sticking with what has worked best for her.

“There are brief periods that there is a value rally, so growth stocks would underperform,” said Ogoshi. “But over the past 20 years we have seen being overweight these growth quality names in a low growth environment has worked in our favor.”

--With assistance from Keiko Ujikane, Naoto Hosoda and Toshiro Hasegawa.

To contact the reporter on this story: Moxy Ying in Hong Kong at yying13@bloomberg.net

To contact the editors responsible for this story: Lianting Tu at ltu4@bloomberg.net, Cormac Mullen

©2019 Bloomberg L.P.