A Dollar Funding Squeeze Is Spreading Across Global Markets

A Dollar Funding Squeeze Is Spreading Across Global Markets

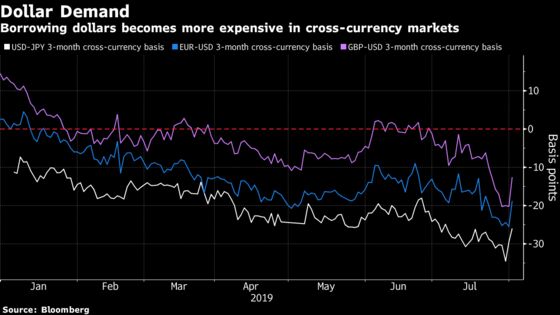

(Bloomberg) -- Borrowing dollars has gotten even more expensive in recent weeks and the squeeze is starting to show up in global money markets.

The premiums that investors have to pay to swap euros, pounds or yen into dollars for three months are close to their highest levels this year, as measured by cross-currency basis swaps. While there was a slight pullback at the end of July, the squeeze could have further to go as it’s being driven by a wide array of factors.

Demand for dollars is increasing as investors prepare for an expected ramp up of Treasury bill issuance following a compromise among U.S. legislators over the debt ceiling. It’s also being driven by increasing bets on policy easing in Europe and the U.K. that’s pressuring the euro and pound, and by Japanese investors looking to swap yen for dollars to buy overseas assets.

Some Wall Street analysts estimate that the U.S. government may sell $200 billion or more of Treasury bills during August and September. Jefferies economist Thomas Simons said that with limited capacity to take on such a large amount of new supply in such a narrow time frame, short-term market rates could face “significant upward pressure heading into the end of the year.”

The U.S. Treasury expects to issue $433 billion in net marketable debt from July through September, about $274 billion more than it had estimated in April, according to figures released this week. The increase in borrowing is larger than analysts had forecast, and much of it is likely to come in the form of T-bills.

Of course, there’s a chance that the increase in T-bill supply fails to have a significant impact in broader funding markets. That’s because the supply and demand dynamics in the unsecured funding sector “seem fairly benign” compared to 2018’s debt-ceiling episode, NatWest strategist Blake Gwinn wrote in a note, referring to the fact that prime money-market fund assets have been outpacing growth in the commercial paper space.

Dollar cross-currency basis tightened on Thursday as month-end demand flows finished and after the Federal Reserve cut interest rates as economists forecast.

Policy Divergence

While dollar demand is rising, speculation the European Central Bank will ease policy some time this year is making it cheaper to borrow euros. At the same time, increasing uncertainty around Brexit is pushing down the pound, prompting local investors to start hedging foreign-currency assets.

In Japan, one-year dollar-yen cross-currency basis is near the widest in more than a year amid speculation the Government Pension Investment Fund will increase currency hedging after its latest annual report showed it had bought bonds with such protection for the first time.

The cost for Japanese investors to hedge holdings of U.S. Treasuries is currently above the yield on 30-year debt, driving them into riskier assets such as credit bonds. Japanese funds bought about 1 trillion yen ($9.2 billion) of U.S. debt including credit products in the three months through May, according to Ministry of Finance data.

“Japanese investors who want to avoid taking currency risks may have to hunt for yields in corporate bonds,” said Masayuki Kichikawa, chief macro strategist at Sumitomo Mitsui DS Asset Management Co. in Tokyo. “They have to continue to seek yields from U.S corporate bonds as they can’t earn returns by buying Treasuries as hedge costs remain very high. ”

--With assistance from Alexandra Harris, Cormac Mullen and Chikafumi Hodo.

To contact the reporter on this story: Stephen Spratt in Hong Kong at sspratt3@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Benjamin Purvis

©2019 Bloomberg L.P.