Bruising Year for Stocks Is Ending in Almost Unheard of Calm

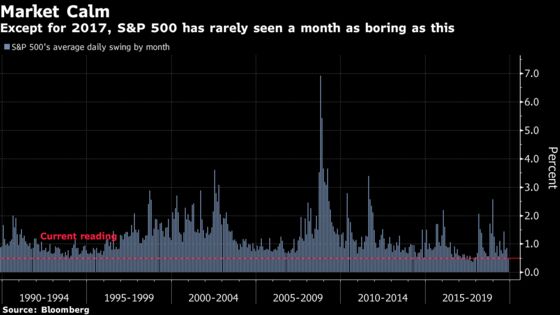

Barring 2017, S&P daily swings are the smallest since 1993.

(Bloomberg) -- An investor probably would’ve panicked if you told her at the start of 2019 that the trade war wouldn’t go away. Or that earnings would fall flat and that a bid to kick out the president would erupt.

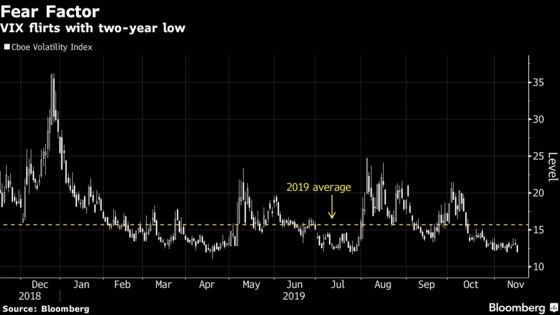

Fast forward 11 months and nobody seems to care. Volatility in the equity market is flirting with a two-year low, with November rivaling the quietest months in three decades. Stocks are booming a month before Christmas, and not even next year’s presidential race is troubling investors.

“You’d think nothing’s happened. It’s incredible,” Paul Brigandi, managing director at Direxion, said by phone. “Volatility’s been depressed. Maybe too depressed, given the uncertainties.”

That peace prevails in the face of upheaval has a way of infuriating certain traders, who say investors are deluding themselves with the help of a compliant Federal Reserve. Donald Trump’s twitter might have gone quiet, but give it time -- the calm won’t last.

On the other hand, tranquility has been a signature characteristic of the bull market for almost 11 years, with every bet on its long-term disruption proving a loser. While bouts of panic have come faster in the last two years, none has driven the VIX above its long-term average for more than a few months. Viewed from that perspective, traders may just be settling back into patterns that have prevailed since the crisis.

It’s so dull that with Friday’s gain, the S&P 500 is guaranteed to go at least 29 sessions without back-to-back declines, the longest stretch since 2005. Peak-to-trough swings have averaged 0.5% a day this month, something that prior to two years ago hadn’t happened since 1993, according to Bloomberg data.

Slowly, equities have gone back to the upward grind that marked 2017, the most tranquil year for the S&P 500 since 1965. Ten-day realized volatility in U.S. stocks has fallen below 3 for the first time since October of that year.

“The market’s nothingness has continued, which begs the question, is it a sign of a tiring market, or one that simply can’t get knocked down?” said Frank Cappelleri, senior equity trader and market technician at Instinet in New York. “The gains have been small, while the pullbacks have been even smaller. Like it or not, low volatility is an uptrend’s friend.”

Such low volatility must mean traders are betting it will storm back, right? The opposite. Going by positioning by hedge funds and other speculators, the smart money is betting on continued tranquility. Such traders in futures on the VIX were net short a record 206,157 contracts as of Tuesday, data from the Commodity Futures Trading Commission show.

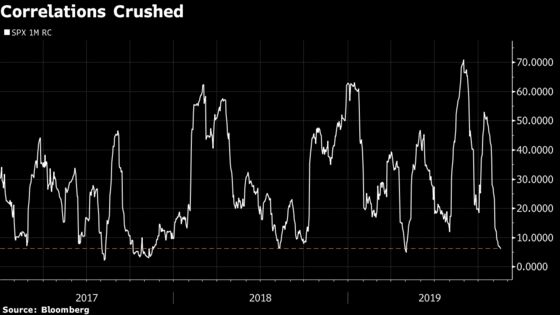

A very 2017 dynamic has been recently at play, with a recovery in bond yields bolstering the appeal of financial firms and allowing them to cushion the blow at times when software shares have gotten knocked. Realized correlations, a key ingredient in volatility since it takes a lot of shares moving together for an index to really swing, have loosened among S&P 500 constituents amid dizzying earnings-season rotations.

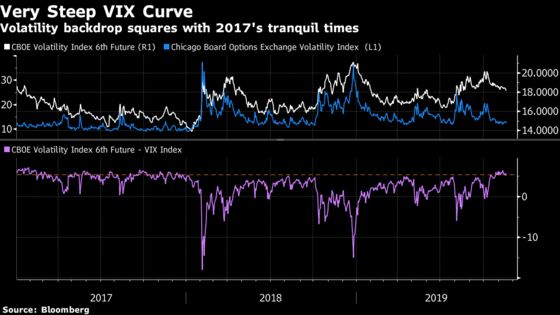

The Cboe Volatility Index -- a gauge of the 30-day implied volatility of U.S. stocks that is often called the “fear gauge” -- closed this week just above 12 as the S&P 500 inched to a fresh record.True, futures on the index that expire in May are more than 5 points higher -- but the steepness of the slope is almost entirely attributable to how quickly the VIX has fallen. Traders minted money off a near-identical disparity in 2017 by selling volatility and no market meltdown materialized.

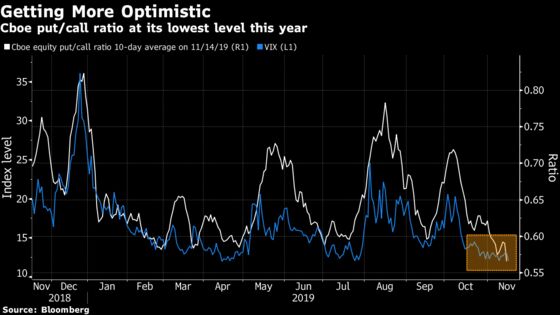

For now, investors are willing to buy the dip, making every pullback shallow and fleeting. There have only been two down days this month, the put-to-call ratio for stocks has dropped to its lowest level this year, there hasn’t been a single day of a larger-than-1% drop since Oct. 8.

“‘Never short a boring market’ is an adage that I think resonates. This market does seem incredibly boring, but you do want to have a good bulk of your portfolio in equities,” Matthew Miskin, a market strategist at John Hancock Advisors LLC in Boston, said in a Bloomberg Television interview. “You haven’t seen any euphoria yet. That’s still to come. You’ve got to participate in that. And equities are the best channel to get that done.”

Of course, just because things are quiet now doesn’t mean they must stay that way. Last year, gyrations in stocks were comparably small in October, just before the commencement of a risk rout that nearly sent equity indexes into a bear market. Other volatility shocks, like February 2018, were presaged by stocks and volatility rising in tandem.

Rising market turbulence is loosely associated with late-stage rallies in some academic literature. Researchers from Harvard University published a study in 2017 listing it as a signal to exit the market in past bubbles, along ballooning share issuance and a concentration in gains among younger companies. Based on that model, even after 10 years and 2,400 points in the S&P 500 the current bull market didn’t even qualify for investigation under their definition of a bubble.

For now, subdued reactions to Donald Trump’s tweets show “the market’s become immune,” said Peter Mallouk, president of Creative Planning, a wealth-management firm with about $45 billion in assets. “When he tweeted about China or anything else, the market would react much more drastically and I think now we just price in that’s just how he does business and we try to measure what’s really behind the tweet or messaging instead of reacting right away.”

--With assistance from Claire Ballentine.

To contact the reporters on this story: Vildana Hajric in New York at vhajric1@bloomberg.net;Luke Kawa in New York at lkawa@bloomberg.net;Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.