A Bond Selloff Is Coming to Emerging Markets of Korea and India

Inflation in these two nations is heavily influenced by rising energy prices given how much they import.

(Bloomberg) -- Bond markets in South Korea and India are the most vulnerable to a sell-off in the region’s emerging markets, even if they’re typically at opposite ends of the investment spectrum.

Inflation in these two nations -- one a tech exporter and the other a services and agriculture-driven economy -- is heavily influenced by rising energy prices given how much they import. Their bonds also have a higher sensitivity to U.S. inflation breakevens than others, according to data compiled by Bloomberg News.

Rising price pressures have led to a rout in the debt markets of Australia and New Zealand this month, and traders are increasingly betting that entrenched inflation will spur central banks globally to turn more hawkish. The Bank of Korea has already hiked 25 basis points, while India this month said it will stop a government bond purchase program.

Risks to the bonds are coming from two fronts, “namely the actual domestic inflation risk that seeps through via import channels, and how emerging-Asia bond markets navigate rising Treasury yields,” according to Vishnu Varathan, head of economics and strategy at Mizuho Bank Ltd. in Singapore.

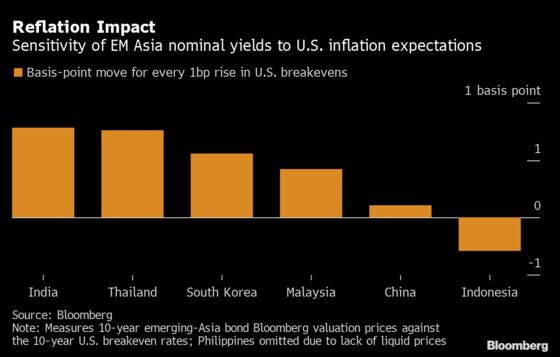

According to a Bloomberg analysis, yields on India’s 10-year bonds gained by 0.78 basis points for every one basis-point rise in the similar-tenor U.S. breakeven rate, based on five episodes starting 2019. A similar gauge for South Korea stood at 0.56. While bonds in Thailand also have a high sensitivity, inflation indicators have stayed within the central bank’s target range.

India imports about 85% of its oil needs, while Korea buys nearly all of its requirements, making them more susceptible to energy prices. The two vulnerable bond markets have little in common otherwise. Yields on 10-year bonds in India are higher than 6% while those for South Korea are at 2.5%.

Rising inflation will spur further hawkish bets in India, with five-year onshore overnight indexed swap rates poised for the biggest monthly gains since February. Reserve Bank of India halting bond purchases is seen as a precursor to raising policy rates.

South Korea’s October inflation figures due next week will be closely watched, after September’s print beat estimates, sending bonds tumbling. This will be the final reading before the Bank of Korea’s policy decision on Nov. 25, with price growth having already exceeded the central bank’s 2% target for six straight months. Swaps are currently pricing in over 100 basis-points of hikes over the next 12 months.

The recent sell off in Korean bonds has spurred authorities into action. The Bank of Korea announced Thursday that it would cut the size of the monetary stabilization bond issuances and increase the amount of bond buy-backs in November. The nation’s finance ministry followed up with an announcement that it will slash shorter-dated government bond issuances in the coming month.

The following table shows the sensitivity of emerging market bond yields to U.S. breakeven rates.

Sensitivity to U.S. break-even rates | Basis point move for each 1bp rise in U.S. breakevens | Z-score |

|---|---|---|

| India | 0.78 | 1.23 |

| Thailand | 0.76 | 0.76 |

| South Korea | 0.56 | 1.01 |

| Malaysia | 0.42 | 2.53 |

| China | 0.11 | 0.58 |

| Indonesia | -0.29 | (0.66) |

©2021 Bloomberg L.P.