A Bond Rally So Fierce That Trend-Following Quants Maxed Out

A Bond Rally So Fierce That Trend-Following Quants Are Maxed Out

(Bloomberg) -- The quants who ride waves of buying and selling love a decisive trend, but even they sound exhausted by this extended bond rally.

After chasing the bull run that’s pushed U.S. yields to record lows and ignited buy signals for systematic players, the cohort known as Commodity Trading Advisors have now likely maxed out on long bets.

Thank the sheer speed of the market advance.

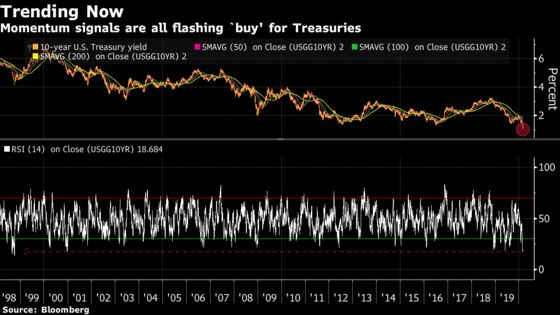

Ten-year Treasuries are near the most overbought since at least 1998 by one indicator, having jumped over other moving-average in decades of history. A Bloomberg index of government bonds is set for its sharpest three-day rally since 2016. JPMorgan Chase & Co. estimates momentum signs for U.S. and German debt were already “extreme” going into last week’s run-up in prices.

And that’s even before the Federal Reserve delivered an emergency rate cut on Tuesday.

It all suggests the fast money has limited firepower to power bonds anew. That makes the securities vulnerable to profit-taking from rules-based traders who buy and sell futures based on mean-reversion signals, according to JPMorgan.

“I don’t think we’re going to raise it a lot more,” Kathryn Kaminski, chief research strategist at AlphaSimplex Group LLC, said on Monday, referring to the fixed-income exposure in its managed-futures strategy. “We have some risk limits in terms of how much risk we take in bonds.”

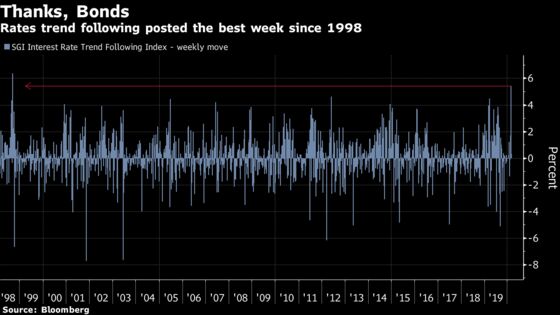

Ten-year Treasury yields dropped near a historic low after the Fed announced a rate cut to forestall the economic impact of the virus. Debt prices from Europe to Japan meanwhile have moved toward last year’s highs. All that has powered a trend-following strategy in interest rates onto its best run since 1998, according to a Societe Generale SA index.

Over at Transtrend BV in Rotterdam, the $4 billion firm only boosted bond exposures “marginally” last week despite the one-way trend, according to strategy specialist Daniel Schotanus. The reason? It already started to ramp up positions from late January.

Similarly, Berouz Fatemi’s tail-risk fund at Tages Capital, which uses a short-term momentum model, has been “full long for the past three weeks everywhere” and isn’t adding fresh allocations.

All told CTAs, which oversee an estimated $300 billion before leverage, lack the firepower to pump prices up further, according to JPMorgan. That suggests real-money investors may have taken over of late, the bank’s strategists led by Nikolaos Panigirtzoglou wrote in a recent note.

“Unequivocally, we’re bullish everywhere in fixed income,” said Roberto Croce, who oversees managed futures strategies at Mellon Investments from Boston. “I don’t see our positions getting longer from here.”

To contact the reporter on this story: Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Sam Potter at spotter33@bloomberg.net, Sid Verma, Yakob Peterseil

©2020 Bloomberg L.P.